JDN 2457545

If you work in economics in any capacity (much like “How is the economy doing?” you don’t even really need to be in macroeconomics), you will encounter many people who believe in the gold standard. Many of these people will be otherwise quite intelligent and educated; they often understand economics better than most people (not that this is saying a whole lot). Yet somehow they continue to hold—and fiercely defend—this incredibly bizarre and anachronistic view of macroeconomics.

They even bring it up at the oddest times; I recently encountered someone who wrote a long and rambling post arguing for drug legalization (which I largely agree with, by the way) and concluded it with #EndTheFed, not seeming to grasp the total and utter irrelevance of this juxtaposition. It seems like it was just a conditioned response, or maybe the sort of irrelevant but consistent coda originally perfected by Cato and his “Carthago delenda est.” “Foederale Reservatum delendum est. Hey, maybe that’s why they’re called the Cato Institute.

So just how bizarre is the gold standard? Well, let’s look at what sort of arguments they use to defend it. I’ll use Charles Kadlic, prominent Libertarian blogger on Forbes, as an example, with his “Top Ten Reasons That You Should Support the ‘Gold Commission’”:

- A gold standard is key to achieving a period of sustained, 4% real economic growth.

- A gold standard reduces the risk of recessions and financial crises.

- A gold standard would restore rising living standards to the middle-class.

- A gold standard would restore long-term price stability.

- A gold standard would stop the rise in energy prices.

- A gold standard would be a powerful force for restoring fiscal balance to federal state and local governments.

- A gold standard would help save Medicare and Social Security.

- A gold standard would empower Main Street over Wall Street.

- A gold standard would increase the liberty of the American people.

- Creation of a gold commission will provide the forum to chart a prudent path toward a 21st century gold standard.

Number 10 can be safely ignored, as clearly Kadlic just ran out of reasons and to make a round number tacked on the implicit assumption of the entire article, namely that this ‘gold commission’ would actually realistically lead us toward a gold standard. (Without it, the other 9 reasons are just non sequitur.)

So let’s look at the other 9, shall we? Literally none of them are true. Several are outright backward.

You know a policy is bad when even one of its most prominent advocates can’t even think of a single real benefit it would have. A lot of quite bad policies do have perfectly real benefits, they’re just totally outweighed by their costs: For example, cutting the top income tax rate to 20% probably would actually contribute something to economic growth. Not a lot, and it would cut a swath through the federal budget and dramatically increase inequality—but it’s not all downside. Yet Kadlic couldn’t actually even think of one benefit of the gold standard that actually holds up. (I actually can do his work for him: I do know of one benefit of the gold standard, but as I’ll get to momentarily it’s quite small and can easily be achieved in better ways.)

First of all, it’s quite clear that the gold standard did not increase economic growth. If you cherry-pick your years properly, you can make it seem like Nixon leaving the gold standard hurt growth, but if you look at the real long-run trends in economic growth it’s clear that we had really erratic growth up until about the 1910s (the surge of government spending in WW1 and the establishment of the Federal Reserve), at which point went through a temporary surge recovering from the Great Depression and then during WW2, and finally, if you smooth out the business cycle, our growth rates have slowly trended downward as growth in productivity has gradually slowed down.

Here’s GDP growth from 1800 to 1900, when we were on the classical gold standard:

Here’s GDP growth from 1929 to today, using data from the Bureau of Economic Analysis:

Also, both of these are total GDP growth (because that is what Kadlic said), which means that part of what you’re seeing here is population growth rather than growth in income per person. Here’s GDP per person in the 1800s:

If you didn’t already know, I bet you can’t guess where on those graphs we left the gold standard, which you’d clearly be able to do if the gold standard had this dramatic “double your GDP growth” kind of effect. I can’t immediately rule out some small benefit to the gold standard just from this data, but don’t worry; more thorough economic studies have done that. Indeed, it is the mainstream consensus among economists today that the gold standard is what caused the Great Depression.

Indeed, there’s a whole subfield of historical economics research that basically amounts to “What were they thinking?” trying to explain why countries stayed on the gold standard for so long when it clearly wasn’t working. Here’s a paper trying to argue it was a costly signal of your “rectitude” in global bond markets, but I find much more compelling the argument that it was psychological: Their belief in the gold standard was simply too strong, so confirmation bias kept holding them back from what needed to be done. They were like my aforementioned #EndTheFed acquaintance.

Then we get to Kadlic’s second point: Does the gold standard reduce the risk of financial crises? Let’s also address point 4, which is closely related: Does the gold standard improve price stability? Tell that to 1929.

In fact, financial crises were more common on the classical gold standard; the period of pure fiat monetary policy was so stable that it was called the Great Moderation, until the crash in 2008 screwed it all up—and that crash occurred essentially outside the standard monetary system, in the “shadow banking system” of unregulated and virtually unlimited derivatives. Had we actually forced banks to stay within the light of the standard banking system, the Great Moderation might have continued indefinitely.

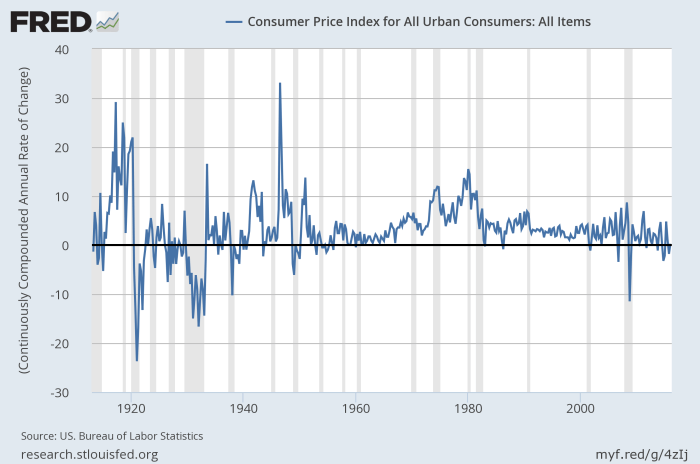

As for “price stability”, that’s sort of true if you look at the long run, because prices were as likely to go down as they were to go up. But that isn’t what we mean by “price stability”. A system with good price stability will have a low but positive and steady level of inflation, and will therefore exhibit some long-run increases in price levels; it won’t have prices jump up and down erratically and end up on average the same.

For jump up and down is what prices did on the gold standard, as you can see from FRED:

This is something we could have predicted in advance; the price of any given product jumps up and down over time, and gold is just one product among many. Tying prices to gold makes no more sense than tying them to any other commodity.

As for stopping the rise in energy prices, energy prices aren’t rising. Even if they were (and they could at some point), the only way the gold standard would stop that is by triggering deflation (and therefore recession) in the rest of the economy.

Regarding number 6, I don’t see how the fiscal balance of federal and state governments is improved by periodic bouts of deflation that make their debt unpayable.

As for number 7, saving Medicare and Social Security, their payments out are tied to inflation and their payments in are tied to nominal GDP, so overall inflation has very little effect on their long-term stability. In any case, the problem with Medicare is spiraling medical costs (which Obamacare has done a lot to fix), and the problem with Social Security is just the stupid arbitrary cap on the income subject to payroll tax; the gold standard would do very little to solve either of those problems, though I guess it would make the nominal income cap less binding by triggering deflation, which is just about the worst way to avoid a price ceiling I’ve ever heard.

Regarding 8 and 9, I don’t even understand why Kadlic thinks that going to a gold standard would empower individuals over banks (does it seem like individuals were empowered over banks in the “Robber Baron Era”?), or what in the world it has to do with giving people more liberty (all that… freedom… you lose… when the Fed… stabilizes… prices?), so I don’t even know where to begin on those assertions. You know what empowers people over banks? The Consumer Financial Protection Bureau. You know what would enhance liberty? Ending mass incarceration. Libertarians fight tooth and nail against the former; sometimes they get behind the latter, but sometimes they don’t; Gary Johnson for some bizarre reason believes in privatization of prisons, which are directly linked to the surge in US incarceration.

The only benefit I’ve been able to come up with for the gold standard is as a commitment mechanism, something the Federal Reserve could do to guarantee its future behavior and thereby reduce the fear that it will suddenly change course on its past promises. This would make forward guidance a lot more effective at changing long-term interest rates, because people would have reason to believe that the Fed means what it says when it projects its decisions 30 years out.

But there are much simpler and better commitment mechanisms the Fed could use. They could commit to a Taylor Rule or nominal GDP targeting, both of which mainstream economists have been clamoring for for decades. There are some definite downsides to both proposals, but also some important upsides; and in any case they’re both obviously better than the gold standard and serve the same forward guidance function.

Indeed, it’s really quite baffling that so many people believe in the gold standard. It cries out for some sort of psychological explanation, as to just what cognitive heuristic is failing when otherwise-intelligent and highly-educated people get monetary policy so deeply, deeply wrong. A lot of them don’t even to seem grasp when or how we left the gold standard; it really happened when FDR suspended gold convertibility in 1933. After that on the Bretton Woods system only national governments could exchange money for gold, and the Nixon shock that people normally think of as “ending the gold standard” was just the final nail in the coffin, and clearly necessary since inflation was rapidly eating through our gold reserves.

A lot of it seems to come down to a deep distrust of government, especially federal government (I still do not grok why the likes of Ron Paul think state governments are so much more trustworthy than the federal government); the Federal Reserve is a government agency (sort of) and is therefore not to be trusted—and look, it has federal right there in the name.

But why do people hate government so much? Why do they think politicians are much less honest than they actually are? Part of it could have to do with the terrifying expansion of surveillance and weakening of civil liberties in the face of any perceived outside threat (Sedition Act, PATRIOT ACT, basically the same thing), but often the same people defending those programs are the ones who otherwise constantly complain about Big Government. Why do polls consistently show that people don’t trust the government, but want it to do more?

I think a lot of this comes down to the vague meaning of the word “government” and the associations we make with particular questions about it. When I ask “Do you trust the government?” you think of the NSA and the Vietnam War and Watergate, and you answer “No.” But when I ask “Do you want the government to do more?” you think of the failure at Katrina, the refusal to expand Medicaid, the pitiful attempts at reducing carbon emissions, and you answer “Yes.” When I ask if you like the military, your conditioned reaction is to say the patriotic thing, “Yes.” But if I ask whether you like the wars we’ve been fighting lately, you think about the hundreds of thousands of people killed and the wanton destruction to achieve no apparent actual objective, and you say “No.” Most people don’t come to these polls with thought-out opinions they want to express; the questions evoke emotional responses in them and they answer accordingly. You can also evoke different responses by asking “Should we cut government spending?” (People say “Yes.”) versus asking “Should we cut military spending, Social Security, or Medicare?” (People say “No.”) The former evokes a sense of abstract government taking your tax money; the latter evokes the realization that this money is used for public services you value.

So, the gold standard has acquired positive emotional vibes, and the Fed has acquired negative emotional vibes.

The former is fairly easy to explain: “good as gold” is an ancient saying, and “the gold standard” is even a saying we use in general to describe the right way of doing something (“the gold standard in prostate cancer treatment”). Humans have always had a weird relationship with gold; something about its timeless and noncorroding shine mesmerizes us. That’s why you occasionally get proposals for a silver standard, but no one ever seems to advocate an oil standard, an iron standard, or a lumber standard, which would make about as much sense.

The latter is a bit more difficult to explain: What did the Fed ever do to you? But I think it might have something to do with the complexity of sound monetary policy, and the resulting air of technocratic mystery surrounding it. Moreover, the Fed actively cultivates this image, by using “open-market operations” and “quantitative easing” to “target interest rates”, instead of just saying, “We’re printing money.” There may be some good reasons to do it this way, but a lot of it really does seem to be intended to obscure the truth from the uninitiated and perpetuate the myth that they are almost superhuman. “It’s all very complicated, you see; you wouldn’t understand.” People are hoarding their money, so there’s not enough money in circulation, so prices are falling, so you’re printing more money and trying to get it into circulation. That’s really not that complicated. Indeed, if it were, we wouldn’t be able to write a simple equation like a Taylor Rule or nominal GDP targeting in order to automate it!

The reason so many people become gold bugs after taking a couple of undergraduate courses in economics, then, is that this teaches them enough that they feel they have seen through the veil; the curtain has been pulled open and the all-powerful Wizard revealed to be an ordinary man at a control panel. (Spoilers? The movie came out in 1939. Actually, it was kind of about the gold standard.) “What? You’ve just been printing money all this time? But that is surely madness!” They don’t actually understand why printing money is actually a perfectly sensible thing to do on many occasions, and it feels to them a lot like what would happen if they just went around printing money (counterfeiting) or what a sufficiently corrupt government could do if they printed unlimited amounts (which is why they keep bringing up Zimbabwe). They now grasp what is happening, but not why. A little learning is a dangerous thing.

Now as for why Paul Volcker wants to go back to Bretton Woods? That, I cannot say. He’s definitely got more than a little learning. At least he doesn’t want to go back to the classical gold standard.

[…] For examples of each, I’m using a hypothetical argument about the gold standard, based on the actual arguments I refute in my previous post on the subject. […]

LikeLike