Jul 25 JDN 2459421

I’ve been under a great deal of stress lately. Somehow I ended up needing to finish my dissertation, get married, and move overseas to start a new job all during the same few months—during a global pandemic.

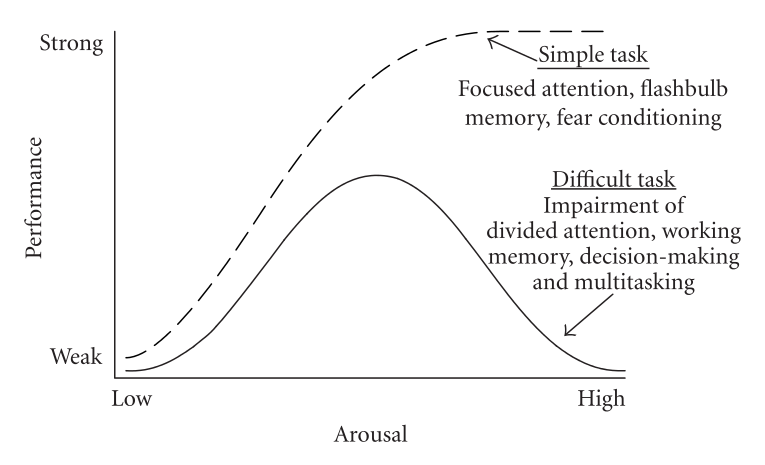

A little bit of stress is useful, but too much can be very harmful. On complicated tasks (basically anything that involves planning or careful thought), increased stress will increase performance up to a point, and then decrease it after that point. This phenomenon is known as the Yerkes-Dodson law.

The Yerkes-Dodson curve very closely resembles the Laffer curve, which shows that since extremely low tax rates raise little revenue (obviously), and extremely high tax rates also raise very little revenue (because they cause so much damage to the economy), the tax rate that maximizes government revenue is actually somewhere in the middle. There is a revenue-maximizing tax rate (usually estimated to be about 70%).

Instead of a revenue-maximizing tax rate, the Yerkes-Dodson law says that there is a performance-maximizing stress level. You don’t want to have zero stress, because that means you don’t care and won’t put in any effort. But if your stress level gets too high, you lose your ability to focus and your performance suffers.

Since stress (like taxes) comes with a cost, you may not even want to be at the maximum point. Performance isn’t everything; you might be happier choosing a lower level of performance in order to reduce your own stress.

But once thing is certain: You do not want to be to the right of that maximum. Then you are paying the cost of not only increased stress, but also reduced performance.

And yet I think many of us spent a great deal of our time on the wrong side of the Yerkes-Dodson curve. I certainly feel like I’ve been there for quite awhile now—most of grad school, really, and definitely this past month when suddenly I found out I’d gotten an offer to work in Edinburgh.

My current circumstances are rather exceptional, but I think the general pattern of being on the wrong side of the Yerkes-Dodson curve is not.

Over 80% of Americans report work-related stress, and the US economy loses about half a trillion dollars a year in costs related to stress.

The World Health Organization lists “work-related stress” as one of its top concerns. Over 70% of people in a cross-section of countries report physical symptoms related to stress, a rate which has significantly increased since before the pandemic.

The pandemic is clearly a contributing factor here, but even without it, there seems to be an awful lot of stress in the world. Even back in 2018, over half of Americans were reporting high levels of stress. Why?

For once, I think it’s actually fair to blame capitalism.

One thing capitalism is exceptionally good at is providing strong incentives for work. This is often a good thing: It means we get a lot of work done, so employment is high, productivity is high, GDP is high. But it comes with some important downsides, and an excessive level of stress is one of them.

But this can’t be the whole story, because if markets were incentivizing us to produce as much as possible, that ought to put us near the maximum of the Yerkes-Dodson curve—but it shouldn’t put us beyond it. Maximizing productivity might not be what makes us happiest—but many of us are currently so stressed that we aren’t even maximizing productivity.

I think the problem is that competition itself is stressful. In a capitalist economy, we aren’t simply incentivized to do things well—we are incentivized to do them better than everyone else. Often quite small differences in performance can lead to large differences in outcome, much like how a few seconds can make the difference between an Olympic gold medal and an Olympic “also ran”.

An optimally productive economy would be one that incentivizes you to perform at whatever level maximizes your own long-term capability. It wouldn’t be based on competition, because competition depends too much on what other people are capable of. If you are not especially talented, competition will cause you great stress as you try to compete with people more talented than you. If you happen to be exceptionally talented, competition won’t provide enough incentive!

Here’s a very simple model for you. Your total performance p is a function of two components, your innate ability aand your effort e. In fact let’s just say it’s a sum of the two: p = a + e

People are randomly assigned their level of capability from some probability distribution, and then they choose their effort. For the very simplest case, let’s just say there are two people, and it turns out that person 1 has less innate ability than person 2, so a1 < a2.

There is also a certain amount of inherent luck in any competition. As it says in Ecclesiastes (by far the best book of the Old Testament), “The race is not to the swift or the battle to the strong, nor does food come to the wise or wealth to the brilliant or favor to the learned; but time and chance happen to them all.” So as usual I’ll model this as a contest function, where your probability of winning depends on your total performance, but it’s not a sure thing.

Let’s assume that the value of winning and cost of effort are the same across different people. (It would be simple to remove this assumption, but it wouldn’t change much in the results.) The value of winning I’ll call y, and I will normalize the cost of effort to 1.

Then this is each person’s expected payoff ui:

ui = (ai + ei)/(a1+e1+a2 + e2) V – ei

You choose effort, not ability, so maximize in terms of ei:

(a2 + e2) V = (a1 +e1+a2 + e2)2 = (a1 + e1) V

a1 + e1 = a2 + e2

p1 = p2

In equilibrium, both people will produce exactly the same level of performance—but one of them will be contributing more effort to compensate for their lesser innate ability.

I’ve definitely had this experience in both directions: Effortlessly acing math tests that I knew other people barely passed despite hours of studying, and running until I could barely breathe to keep up with other people who barely seemed winded. Clearly I had too little incentive in math class and too much in gym class—and competition was obviously the culprit.

If you vary the cost of effort between people, or make it not linear, you can make the two not exactly equal; but the overall pattern will remain that the person who has more ability will put in less effort because they can win anyway.

Yet presumably the amount of effort we want to incentivize isn’t less for those who are more talented. If anything, it may be more: Since an hour of work produces more when done by the more talented person, if the cost to them is the same, then the net benefit of that hour of work is higher than the same hour of work by someone less talented.

In a large population, there are almost certainly many people whose talents are similar to your own—but there are also almost certainly many below you and many above you as well. Unless you are properly matched with those of similar talent, competition will systematically lead to some people being pressured to work too hard and others not pressured enough.

But if we’re all stressed, where are the people not pressured enough? We see them on TV. They are celebrities and athletes and billionaires—people who got lucky enough, either genetically (actors who were born pretty, athletes who were born with more efficient muscles) or environmentally (inherited wealth and prestige), to not have to work as hard as the rest of us in order to succeed. Indeed, we are constantly bombarded with images of these fantastically lucky people, and by the availability heuristic our brains come to assume that they are far more plentiful than they actually are.

This dramatically exacerbates the harms of competition, because we come to feel that we are competing specifically with the people who were handed the world on a silver platter. Born without the innate advantages of beauty or endurance or inheritance, there’s basically no chance we could ever measure up; and thus we feel utterly inadequate unless we are constantly working as hard as we possibly can, trying to catch up in a race in which we always fall further and further behind.

How can we break out of this terrible cycle? Well, we could try to replace capitalism with something like the automated luxury communism of Star Trek; but this seems like a very difficult and long-term solution. Indeed it might well take us a few hundred years as Roddenberry predicted.

In the shorter term, we may not be able to fix the economic problem, but there is much we can do to fix the psychological problem.

By reflecting on the full breadth of human experience, not only here and now, but throughout history and around the world, you can come to realize that you—yes, you, if you’re reading this—are in fact among the relatively fortunate. If you have a roof over your head, food on your table, clean water from your tap, and ibuprofen in your medicine cabinet, you are far more fortunate than the average person in Senegal today; your television, car, computer, and smartphone are things that would be the envy even of kings just a few centuries ago. (Though ironically enough that person in Senegal likely has a smartphone, or at least a cell phone!)

Likewise, you can reflect upon the fact that while you are likely not among the world’s most very most talented individuals in any particular field, there is probably something you are much better at than most people. (A Fermi estimate suggests I’m probably in the top 250 behavioral economists in the world. That’s probably not enough for a Nobel, but it does seem to be enough to get a job at the University of Edinburgh.) There are certainly many people who are less good at many things than you are, and if you must think of yourself as competing, consider that you’re also competing with them.

Yet perhaps the best psychological solution is to learn not to think of yourself as competing at all. So much as you can afford to do so, try to live your life as if you were already living in a world that rewards you for making the best of your own capabilities. Try to live your life doing what you really think is the best use of your time—not your corporate overlords. Yes, of course, we must do what we need to in order to survive, and not just survive, but indeed remain physically and mentally healthy—but this is far less than most First World people realize. Though many may try to threaten you with homelessness or even starvation in order to exploit you and make you work harder, the truth is that very few people in First World countries actually end up that way (it couldbe brought to zero, if our public policy were better), and you’re not likely to be among them. “Starving artists” are typically a good deal happier than the general population—because they’re not actually starving, they’ve just removed themselves from the soul-crushing treadmill of trying to impress the neighbors with manicured lawns and fancy SUVs.