Many commentators had been worried that the discredited center-right parties in these countries had left a power vacuum that would be filled by far-right parties like France’s National Rally, but this isn’t what happened. Voters showed up to the polls, and they voted out the center-right all right; but what they put in its place was the center-left, not the far-right.

The New York Times is constitutionally incapable of celebrating anything, so they immediately turned to worries that “turnout was low” and this indicates “an unhappy Britain”. Honestly this seems to be a general failing of journalists: They can’t ever say anything is good. Their entire view of the world is based around “if it bleeds, it leads”. I’m assuming this has something to do with incentives created by the market of news consumers, but it also seems to be an entrenched social norm among journalists themselves. The world must be getting worse, in every way, or if it’s obviously not, we don’t talk about those things—because good things just aren’t news. (Look no further than the fact we now have the lowest global homicide rates in the history of the human race. What, you didn’t realize we had that right now? Could that perhaps be because literally no news source even mentioned it, ever?)

Now, to be fair, turnout was low, and far-right parties did win some representation, and any kind of sudden political shift indicates some kind of public dissatisfaction… but for goodness’ sake, can we take the win for once?

These elections are proof that the free world’s slide into far-right authoritarianism doesn’t have to be inevitable. We can fight it, we are fighting it—and sometimes, we actually win.

So let’s not give up hope in the United States, either. Yes, polls of the Biden/Trump election don’t look great right now; Trump seems to have a slight lead, and it’s way too close for comfort. But we don’t need to roll over and die. The left can win, when we band together well enough; and if France and Britain can pull it off, I don’t see why we can’t too.

Biden is old. Sure. So is Trump. And if it turns out that Biden is really unhealthy, guess what? That means he’ll die or resign and weget a woman of color as President instead. I don’t see eye-to-eye with Kamala Harris on everything, but I don’t see her taking office as a horrible outcome. It’s certainly a hundred times better than what happens if we let Trump win.

Are there better candidates out there? Theoretically, sure. But unless one of them manages to win nomination by one of the two leading parties, that doesn’t matter. Because in a first-past-the-post voting system, you either vote for one of the top two, or you waste your vote. I’m sorry. It sucks. I want a new voting system too. I know exactly which one we could use that would be a hundred times better. But we’re not going to get it by refusing to vote altogether.

We might get a better voting system by voting strategically for candidates who are open to the idea—which at this juncture clearly means Democrats, not Republicans. (At this point in history, Republicans don’t seem entirely convinced that we should decide things democratically in the first place.)There are also other forms of activism we can use, independent of voting. But not voting isn’t a form of activism, and we should stop acting like it is. Not voting is the lazy, selfish, default option. It’s what you’d do if you were a neoclassical rational agent who cares not in the least for his fellow human beings. You should never be proud of not voting. You’re not sending a message; you’re shirking your civic responsibility.

Voting isn’t writing a love letter. It isn’t signing a form endorsing everything a candidate has ever done or ever will do. If you think of it that way, you’re going to never want to vote—and thus you’re going to give up the most important power you have as a citizen of a democracy.

Voting is a decision. It’s choosing one alternative over another. Like any decision in the real world, there will almost never be a perfect option. There will only be better or worse options. Sometimes, even, you’ll feel that there are only bad options, and you are choosing the least-bad option. But you still have to choose the least-bad option, because literally everything else is worse—including doing nothing.

So get out there and try to help Biden win. Not because you love Biden, but because it’s your civic duty. And if enough people do it, we can still win this.

Is this the result of systemic failings of the academic system? Before deciding that, one thing we should consider is that very smart people do seem to have a higher risk of depression.

This suggests that, yes, there really is something wrong with academia. It may not be entirely the fault of the system—perhaps even a well-designed academic system would result in more depression than the general population because we are genetically predisposed. But it really does seem like there is a substantial environmental contribution that academic institutions bear some responsibility for.

Don’t other jobs evaluate performance? Sure. But not constantly the way that academia does. This is especially obvious as a student, where everything you do is graded; but it largely continues once you are faculty as well.

For most jobs, you are concerned about doing well enough to keep your job or maybe get a raise. But academia has this continuous forward pressure: if you are a grad student or junior faculty, you can’t possibly keep your job; you must either move upward to the next stage or drop out. And academia has become so hyper-competitive that if you want to continue moving upward—and someday getting that tenure—you must publish in top-ranked journals, which have utterly opaque criteria and ever-declining acceptance rates. And since there are so few jobs available compared to the number of applicants, good enough is never good enough; you must be exceptional, or you will fail. Two thirds of PhD graduates seek a career in academia—but only 30% are actually in one three years later. (And honestly, three years is pretty short; there are plenty of cracks left to fall through between that and a genuinely stable tenured faculty position.)

Moreover, our skills are so hyper-specialized that it’s very hard to imagine finding work anywhere else. This grants academic institutions tremendous monopsony power over us, letting them get away with lower pay and worse working conditions. Even with an economics PhD—relatively transferable, all things considered—I find myself wondering who would actually want to hire me outside this ivory tower, and my feeble attempts at actually seeking out such employment have thus far met with no success.

I also find academia painfully isolating. I’m not an especially extraverted person; I tend to score somewhere near the middle range of extraversion (sometimes called an “ambivert”). But I still find myself craving more meaningful contact with my colleagues. We all seem to work in complete isolation from one another, even when sharing the same office (which is awkward for other reasons). There are very few consistent gatherings or good common spaces. And whenever faculty do try to arrange some sort of purely social event, it always seems to involve drinking at a pub and nobody is interested in providing any serious emotional or professional support.

Some of this may be particular to this university, or to the UK; or perhaps it has more to do with being at a certain stage of my career. In any case I didn’t feel nearly so isolated in graduate school; I had other students in my cohort and adjacent cohorts who were going through the same things. But I’ve been here two years now and so far have been unable to establish any similarly supportive relationships with colleagues.

There may be some opportunities I’m not taking advantage of: I’ve skipped a lot of research seminars, and I stopped going to those pub gatherings. But it wasn’t that I didn’t try them at all; it was that I tried them a few times and quickly found that they were not filling that need. At seminars, people only talked about the particular research project being presented. At the pub, people talked about almost nothing of serious significance—and certainly nothing requiring emotional vulnerability. The closest I think I got to this kind of support from colleagues was a series of lunch meetings designed to improve instruction in “tutorials” (what here in the UK we call discussion sections); there, at least, we could commiserate about feeling overworked and dealing with administrative bureaucracy.

There seem to be deep, structural problems with how academia is run. This whole process of universities outsourcing their hiring decisions to the capricious whims of high-ranked journals basically decides the entire course of our careers. And once you get to the point I have, now so disheartened with the process of publishing research that I can’t even engage with it, it’s not at all clear how it’s even possible to recover. I see no way forward, no one to turn to. No one seems to care how well I teach, if I’m not publishing research.

And I’m clearly not the only one who feels this way.

When I first decided to move to Edinburgh, I certainly did not expect it to be such a historic time. The pandemic was already in full swing, but I thought that would be all. But this year I was living in the UK when its leadership changed in two historic ways:

First, there was the death of Queen Elizabeth II, and the coronation of King Charles III.

Second, there was the resignation of Boris Johnson, the appointment of Elizabeth Truss, and then, so rapidly I feel like I have whiplash, the resignation of Elizabeth Truss.

In other words, I have seen the end of the longest-reigning monarch and the rise and fall of the shortest-reigning prime minister in the history of the United Kingdom. The three hundred-year history of the United Kingdom.

The prior probability of such a 300-year-historic event happening during my own 3-year term in the UK is approximately 1%. Yet, here we are. A new king, one of a handful of genuine First World monarchs to be coronated in the 21st century. The others are the Netherlands, Belgium, Spain, Monaco, Andorra, and Luxembourg; none of these have even a third the population of the UK, and if we include every Commonwealth Realm (believe it or not, “realm” is in fact still the official term), Charles III is now king of a supranational union with a population of over 150 million people—half the size of the United States. (Yes, he’s your king too, Canada!) Note that Charles III is not king of the entire Commonwealth of Nations, which includes now-independent nations such as India, Pakistan, and South Africa; that successor to the British Empire contains 54 nations and has a population of over 2 billion.

I still can’t quite wrap my mind around this idea of having a king. It feels even more ancient and anachronistic than the 400-year-old university I work at. Of course I knew that we had a queen before, and that she was old and would presumably die at some point and probably be replaced; but that wasn’t really salient information to me until she actually did die and then there was a ten-mile-long queue to see her body and now next spring they will be swearing in this new guy as the monarch of the fourteen realms. It now feels like I’m living in one of those gritty satirical fractured fairy tales. Maybe it’s an urban fantasy setting; it feels a lot like Shrek, to be honest.

Yet other than feeling surreal, none of this has affected my life all that much. I haven’t even really felt the effects of inflation: Groceries and restaurant meals seem a bit more expensive than they were when we arrived, but it’s well within what our budget can absorb; we don’t have a car here, so we don’t care about petrol prices; and we haven’t even been paying more than usual in natural gas because of the subsidy programs. Actually it’s probably been good for our household finances that the pound is so weak and the dollar is so strong. I have been much more directly affected by the university union strikes: being temporary contract junior faculty (read: expendable), I am ineligible to strike and hence had to cross a picket line at one point.

Perhaps this is what history has always felt like for most people: The kings and queens come and go, but life doesn’t really change. But I honestly felt more directly affected by Trump living in the US than I did by Truss living in the UK.

This may be in part because Elizabeth Truss was a very unusual politician; she combined crazy far-right economic policy with generally fairly progressive liberal social policy. A right-wing libertarian, one might say. (As Krugman notes, such people are astonishingly rare in the electorate.) Her socially-liberal stance meant that she wasn’t trying to implement horrific hateful policies against racial minorities or LGBT people the way that Trump was, and for once her horrible economic policies were recognized immediately as such and quickly rescinded. Unlike Trump, Truss did not get the chance to appoint any supreme court justices who could go on to repeal abortion rights.

Then again, Truss couldn’t have appointed any judges if she’d wanted to. The UK Supreme Court is really complicated, and I honestly don’t understand how it works; but from what I do understand, the Prime Minister appoints the Lord Chancellor, the Lord Chancellor forms a commission to appoint the President of the Supreme Court, and the President of the Supreme Court forms a commission to appoint new Supreme Court judges. But I think the monarch is considered the ultimate authority and can veto any appointment along the way. (Or something. Sometimes I get the impression that no one truly understands the UK system, and they just sort of go with doing things as they’ve always been done.) This convoluted arrangement seems to grant the court considerably more political independence than its American counterpart; also, unlike the US Supreme Court, the UK Supreme Court is not allowed to explicitly overturn primary legislation. (Fun fact: The Lord Chancellor is also the Keeper of the Great Seal of the Realm, because Great Britain hasn’t quite figured out that the 13th century ended yet.)

It’s sad and ironic that it was precisely by not being bigoted and racist that Truss ensured she would not have sufficient public support for her absurd economic policies. There’s a large segment of the population of both the US and UK—aptly, if ill-advisedly, referred to by Clinton as “deplorables”—who will accept any terrible policy as long as it hurts the right people. But Truss failed to appeal to that crucial demographic, and so could find no one to support her. Hence, her approval rating fell to a dismal 10%, and she was outlasted by a head of lettuce.

At the time of writing, the new prime minister has not yet been announced, but the smart money is on Rishi Sunak. (I mean that quite literally; he’s leading in prediction markets.) He’s also socially liberal but fiscally conservative, but unlike Truss he seems to have at least some vague understanding of how economics works. Sunak is also popular in a way Truss never was (though that popularity has been declining recently). So I think we can expect to get new policies which are in the same general direction as what Truss wanted—lower taxes on the rich, more privatization, less spent on social services—but at least Sunak is likely to do so in a way that makes the math(s?) actually add up.

Natural gas prices are rising worldwide, but not nearly as much: Henry Hub natural gas prices (a standard metric for natural gas prices in the US) have risen from under $2 per million BTU in 2020 to nearly $9 today. This substantial divide in prices can only be sustained because transporting natural gas is expensive and requires substantial infrastructure. (1 megawatt-hour is about 3.4 million BTU, and the euro is trading at parity with the dollar (!), so effectively US prices rose from €7 per MWh to €31 per MWh—as opposed to €200.)

As a result, a lot of people in Europe are suddenly finding their utility bills unaffordable. (I’m fortunate that my flat is relatively well-insulated and my income is reasonably high, so I’m not among them; the higher prices will be annoying, but not beyond my means.) What should we do about this?

There are some economists who would say we should do nothing at all: Laissez-faire. Markets are efficient, right? So just let people freeze! Fortunately, Europe is not governed by such people nearly as much as the US is.

But while most economists would agree that we should do something, it’s much harder to get them to agree on exactly what.

Rising prices of natural gas are sort of a good thing, from an environmental perspective; they’ll provide an incentive to reduce carbon emissions. So it’s tempting to say that we should just let the prices rise and then compensate by raising taxes and paying transfers to poor families. But that probably isn’t politically viable; all three parts—letting prices rise, raising taxes, and increasing transfers—are all going to make enemies, and we really must have all three for such a plan to work.

The current approach seems to be based on price controls: Don’t let the prices rise so much. The UK has such a policy in place: Natural gas prices for consumers are capped by regulations. The cap has been increased in response to the crisis (itself an unpopular, but clearly necessary, move), but even so 31 gas companies have already gone under across the UK since the start of 2021. It really seems to be the case that for many gas companies, especially the smaller ones with less economy of scale, it’s simply not possible to continue providing natural gas to homes with input prices so high and output prices capped so low.

Or, we could let prices rise that high for producers, but subsidize consumers so that they don’t feel it; several European countries are already doing this. That at least won’t result in gas companies failing, but it will cost a lot of government funds. Greece in particular is spending over 3% of their GDP on it! (For comparison, the US military budget is about 4% of GDP.) I think this might actually be the best option, though all that spending will mean more government debt or higher taxes.

We could also ration energy use, as we’ve often done during wartime. (Is this wartime? Kind of? Not really? It certainly is starting to feel like Cold War II.) Indeed, the President of the European Commission basically said that this should happen. That, at least, would reap some of the environmental benefits of reduced natural gas consumption. Rationing also feels fair to most people in a way that simply letting market prices rise does not; there is a sense of shared sacrifice. What worries me, however, is that the rations won’t be well-designed enough to account for energy usage that isn’t in a family’s immediate control. If you’re renting a flat that is poorly insulated, you can’t immediately fix that. You can try to pressure the landlord into buying better insulation, but in the meantime you’re the one paying the energy bills—or getting cold when the natural gas ration isn’t enough.

Actually I strongly suspect that most household usage of natural gas is of this kind; people don’t generally heat their homes more than necessary just because gas is cheap. Maybe they can set the thermostat a degree or two lower when gas is expensive, or maybe they use the gas oven less often and the microwave more; but the vast majority of their gas consumption is a function of the climate they live in and the insulation of their home, not their day-to-day choices. So if we’re trying to incentivize more efficient energy usage, that’s a question of long-term investment in construction and retrofitting, not something that sudden price spikes will really help with.

In the long run, what we really need to do is wean ourselves off of natural gas. Currently natural gas provides 33% of energy and nearly 40% of heating in Europe. (US figures are comparable.) Switching to electric heat pumps and powering them with solar and wind power isn’t something we can do overnight—but it is something we surely must do.

I think ultimately what is going to happen is all of the above: Different countries will adopt different policy mixes, all of them will involve difficult compromises, none of them will be particularly well-designed, and we’ll all sort of muddle through as best we can.

Manchin wants to call it the Inflation Reduction Act, but it probably won’t actually reduce inflation very much. But some economists—even quite center-right ones—think it may actually reduce inflation quite a bit, and we basically all agree that it at least won’t increase inflation very much. Since the effects on inflation are likely to be small, we really don’t have to worry about them: whatever it does to inflation, the important thing is that this bill reduces carbon emissions.

Honestly, it’ll be kind of disgusting if this actually does work—because it’s so easy. This bill will have almost no downside. Its macroeconomic effects will be minor, maybe even positive. There was no reason it needed to be this hard-fought. Even if it didn’t have tax increases to offset it—which it absolutely does—the total cost of this bill over the next ten years would be less than six months of military spending, so cutting military spending by 5% would cover it. We have cured our unbearable headaches by finally realizing we could stop hitting ourselves in the head. (And the Republicans want us to keep hitting ourselves and will do whatever they can to make that happen.)

So, yes, it’s very sad that it took us this long. And even 60% of our current emissions is still too much emissions for a stable climate. But let’s take a moment to celebrate, because this is a genuine victory—and we haven’t had a lot of those in awhile.

While a return to double-digits remains possible, at this point it likely won’t happen, and if it does, it will occur only briefly.

This is no doubt a major reason why the dollar and the pound are widely used as reserve currencies (especially the dollar), and is likely due to the fact that they are managed by the world’s most competent central banks. Brexit would almost have made sense if the UK had been pressured to join the Euro; but they weren’t, because everyone knew the pound was better managed.

The Euro also doesn’t have much inflation, but if anything they err on the side of too low, mainly because Germany appears to believe that inflation is literally Hitler. In fact, the rise of the Nazis didn’t have much to do with the Weimar hyperinflation. The Great Depression was by far a greater factor—unemployment is much, much worse than inflation. (By the way, it’s weird that you can put that graph back to the 1980s. It, uh, wasn’t the Euro then. Euros didn’t start circulating until 1999. Is that an aggregate of the franc and the deutsche mark and whatever else? The Euro itself has never had double-digit inflation—ever.)

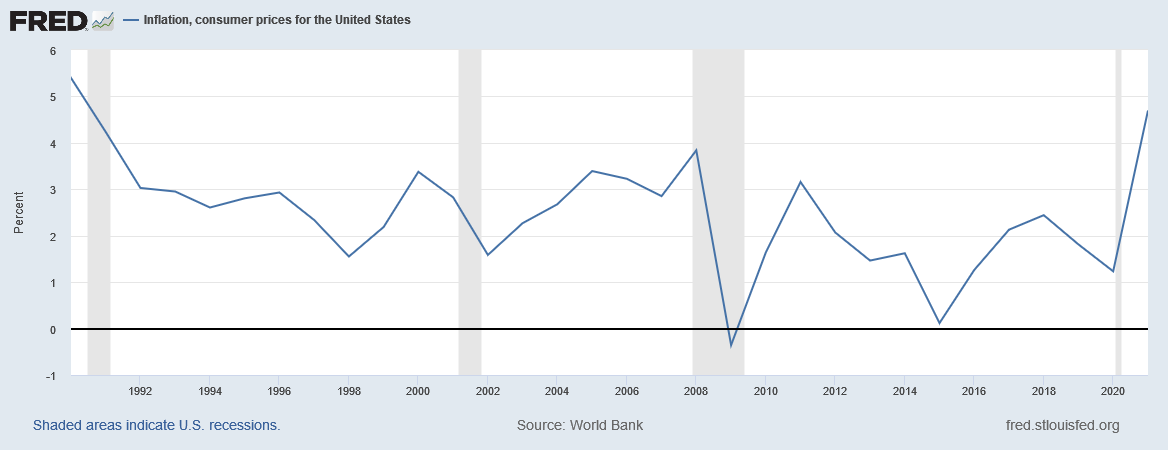

But it’s always a little surreal for me to see how panicked people in the US and UK get when our inflation rises a couple of percentage points. There seems to be an entire subgenre of economics news that basically consists of rich people saying the sky is falling because inflation has risen—or will, or may rise—by two points. (Hey, anybody got any ideas how we can get them to panic like this over rises in sea level or aggregate temperature?)

Hyperinflation is a real problem—it isn’t what put Hitler into power, but it has led to real crises in Germany, Zimbabwe, and elsewhere. Once you start getting over 100% per year, and especially when it starts rapidly accelerating, that’s a genuine crisis. Moreover, even though they clearly don’t constitute hyperinflation, I can see why people might legitimately worry about price increases of 20% or 30% per year. (Let alone 60% like Argentina is dealing with right now.) But why is going from 2% to 6% any cause for alarm? Yet alarmed we seem to be.

I can even understand why rich people would be upset about inflation (though the magnitudeof their concern does still seem disproportionate). Inflation erodes the value of financial assets, because most bonds, options, etc. are denominated in nominal, not inflation-adjusted terms. (Though there are such things as inflation-indexed bonds.) So high inflation can in fact make rich people slightly less rich.

But why in the world are so many poor people upset about inflation?

Inflation doesn’t just erode the value of financial assets; it also erodes the value of financial debts. And most poor people have more debts than they have assets—indeed, it’s not uncommon for poor people to have substantial debt and no financial assets to speak of (what little wealth they have being non-financial, e.g. a car or a home). Thus, their net wealth position improves as prices rise.

The interest rate response can compensate for this to some extent, but most people’s debts are fixed-rate. Moreover, if it’s the higher interest rates you’re worried about, you should want the Federal Reserve and the Bank of England not to fight inflation too hard, because the way they fight it is chiefly by raising interest rates.

I admit, I question the survey design here: I would answer ‘yes’ to both questions if we’re talking about a theoretical 10,000% hyperinflation, but ‘no’ if we’re talking about a realistic 10% inflation. So I would like to see, but could not find, a survey asking people what level of inflation is sufficient cause for concern. But since most of these people seemed concerned about actual, realistic inflation (85% reported anger at seeing actual, higher prices), it still suggests a lot of strong feelings that even mild inflation is bad.

So it does seem to be the case that a lot of poor and middle-class people really strongly dislike inflation even in the actual, mild levels in which it occurs in the US and UK.

The main fear seems to be that inflation will erode people’s purchasing power—that as the price of gasoline and groceries rise, people won’t be able to eat as well or drive as much. And that, indeed, would be a real loss of utility worth worrying about.

But in fact this makes very little sense: Most forms of income—particularly labor income, which is the only real income for some 80%-90% of the population—actually increases with inflation, more or less one-to-one. Yes, there’s some delay—you won’t get your annual cost-of-living raise immediately, but several months down the road. But this could have at most a small effect on your real consumption.

To see this, suppose that inflation has risen from 2% to 6%. (Really, you need not suppose; it has.) Now consider your cost-of-living raise, which nearly everyone gets. It will presumably rise the same way: So if it was 3% before, it will now be 7%. Now consider how much your purchasing power is affected over the course of the year.

For concreteness, let’s say your initial income was $3,000 per month at the start of the year (a fairly typical amount for a middle-class American, indeed almost exactly the median personal income). Let’s compare the case of no inflation with a 1% raise, 2% inflation with a 3% raise, and 5% inflation with a 6% raise.

If there was no inflation, your real income would remain simply $3,000 per month, until the end of the year when it would become $3,030 per month. That’s the baseline to compare against.

If inflation is 2%, your real income would gradually fall, by about 0.16% per month, before being bumped up 3% at the end of the year. So in January you’d have $3,000, in February $2,995, in March $2,990. Come December, your real income has fallen to $2,941. But then next January it will immediately be bumped up 3% to $3,029, almost the same as it would have been with no inflation at all. The total lost income over the entire year is about $380, or about 1% of your total income.

If inflation instead rises to 6%, your real income will fall by 0.49% per month, reaching a minimum of $2,830 in December before being bumped back up to $3,028 next January. Your total loss for the whole year will be about $1110, or about 3% of your total income.

Indeed, it’s a pretty good heuristic to say that for an inflation rate of x% with annual cost-of-living raises, your loss of real income relative to having no inflation at all is about (x/2)%. (This breaks down for really high levels of inflation, at which point it becomes a wild over-estimate, since even 200% inflation doesn’t make your real income go to zero.)

This isn’t nothing, of course. You’d feel it. Going from 2% to 6% inflation at an income of $3000 per month is like losing $700 over the course of a year, which could be a month of groceries for a family of four. (Not that anyone can really raise a family of four on a single middle-class income these days. When did The Simpsons begin to seem aspirational?)

But this isn’t the whole story. Suppose that this same family of four had a mortgage payment of $1000 per month; that is also decreasing in real value by the same proportion. And let’s assume it’s a fixed-rate mortgage, as most are, so we don’t have to factor in any changes in interest rates.

With no inflation, their mortgage payment remains $1000. It’s 33.3% of their income this year, and it will be 33.0% of their income next year after they get that 1% raise.

With 2% inflation, their mortgage payment will also fall by 0.16% per month; $998 in February, $996 in March, and so on, down to $980 in December. This amounts to an increase in real income of about $130—taking away a third of the loss that was introduced by the inflation.

With 6% inflation, their mortgage payment will also fall by 0.49% per month; $995 in February, $990 in March, and so on, until it’s only $943 in December. This amounts to an increase in real income of over $370—again taking away a third of the loss.

Indeed, it’s no coincidence that it’s one third; the proportion of lost real income you’ll get back by cheaper mortgage payments is precisely the proportion of your income that was spent on mortgage payments at the start—so if, like too many Americans, they are paying more than a third of their income on mortgage, their real loss of income from inflation will be even lower.

And what if they are renting instead? They’re probably on an annual lease, so that payment won’t increase in nominal terms either—and hence will decrease in real terms, in just the same way as a mortgage payment. Likewise car payments, credit card payments, any debt that has a fixed interest rate. If they’re still paying back student loans, their financial situation is almost certainly improved by inflation.

This means that the real loss from an increase of inflation from 2% to 6% is something like 1.5% of total income, or about $500 for a typical American adult. That’s clearly not nearly as bad as a similar increase in unemployment, which would translate one-to-one into lost income on average; moreover, this loss would be concentrated among people who lost their jobs, so it’s actually worse than that once you account for risk aversion. It’s clearly better to lose 1% of your income than to have a 1% chance of losing nearly all your income—and inflation is the former while unemployment is the latter.

Indeed, the only reason you lost purchasing power at all was that your cost-of-living increases didn’t occur often enough. If instead you had a labor contract that instituted cost-of-living raises every month, or even every paycheck, instead of every year, you would get all the benefits of a cheaper mortgage and virtually none of the costs of a weaker paycheck. Convince your employer to make this adjustment, and you will actually benefit from higher inflation.

So if poor and middle-class people are upset about eroding purchasing power, they should be mad at their employers for not implementing more frequent cost-of-living adjustments; the inflation itself really isn’t the problem.

As I write this, we have just passed the 20th anniversary of 9/11. Yet only in the past month were US troops finally withdrawn from Afghanistan—and that withdrawal was immediately followed by a total collapse of the Afghan government and a reinstatement of the Taliban. The United States had been at war for nearly 20 years, spending trillions of dollars and causing thousands of deaths—and seems to have accomplished precisely nothing.

Some left-wing circles have been saying that the Taliban offered surrender all the way back in 2001; this is not accurate. Alternet even refers to it as an “unconditional surrender” which is utter nonsense. No one in their right mind—not even the most die-hard imperialist—wouldever refuse an unconditional surrender, and the US most certainly did nothing of the sort.)

The Taliban did offer a peace deal in 2001, which would have involved giving the US control of Kandahar and turning Osama bin Laden over to a neutral country (not to the US or any US ally). It would also have granted amnesty to a number of high-level Taliban leaders, which was a major sticking point for the US. In hindsight, should they have taken the deal? Obviously. But I don’t think that was nearly so clear at the time—nor would it have been particularly palatable to most of the American public to leave Osama bin Laden under house arrest in some neutral country (which they never specified by the way; somewhere without US extradition, presumably?) and grant amnesty to the top leaders of the Taliban.

Thus, even after the 20-year nightmare of the war that refused to end, we are still back to the nightmare we were in before—Afghanistan ruled by fanatics who will oppress millions.

Yet somehow this isn’t even the worst unending nightmare, for after a year and a half we are still in the throes of a global pandemic which has now caused over 4.6 million deaths. We are still wearing masks wherever we go—at least, those of us who are complying with the rules. We have gotten vaccinated already, but likely will need booster shots—at least, those of us who believe in vaccines.

The most disturbing part of it all is how many people still aren’t willing to follow the most basic demands of public health agencies.

In case you thought this was just an American phenomenon: Just a few days ago I looked out the window of my apartment to see a protest in front of the Scottish Parliament complaining about vaccine and mask mandates, with signs declaring it all a hoax. (Yes, my current temporary apartment overlooks the Scottish Parliament.)

Some of those signs displayed a perplexing innumeracy. One sign claimed that the vaccines must be stopped because they had killed 1,400 people in the UK. This is not actually true; while there have been 1,400 people in the UK who died after receiving a vaccine, 48 million people in the UK have gotten the vaccine, and many of them were old and/or sick, so, purely by statistics, we’d expect some of them to die shortly afterward. Less than 100 of these deaths are in any way attributable to the vaccine. But suppose for a moment that we took the figure at face value, and assumed, quite implausibly, that everyone who died shortly after getting the vaccine was in fact killed by the vaccine. This 1,400 figure needs to be compared against the 156,000 UK deaths attributable to COVID itself. Since 7 million people in the UK have tested positive for the virus, this is a fatality rate of over 2%. Even if we suppose that literally everyone in the UK who hasn’t been vaccinated in fact had the virus, that would still only be 20 million (the UK population of 68 million – the 48 million vaccinated) people, so the death rate for COVID itself would still be at least 0.8%—a staggeringly high fatality rate for a pandemic airborne virus. Meanwhile, even on this ridiculous overestimate of the deaths caused by the vaccine, the fatality rate for vaccination would be at most 0.003%. Thus, even by the anti-vaxers’ own claims, the vaccine is nearly 300 times safer than catching the virus. If we use the official estimates of a 1.9% COVID fatality rate and 100 deaths caused by the vaccines, the vaccines are in fact over 9000 times safer.

Indeed, the predominant tone I get from trying to keep up on the current news in epidemiology is fatalism: It’s too late, we’ve already failed to contain the virus, we won’t reach herd immunity, we won’t ever eradicate it. At this point they now all seem to think that COVID is going to become the new influenza, always with us, a major cause of death that somehow recedes into the background and seems normal to us—but COVID, unlike influenza, may stick around all year long. The one glimmer of hope is that influenza itself was severely hampered by the anti-pandemic procedures, and influenza cases and deaths are indeed down in both the US and UK (though not zero, nor as drastically reduced as many have reported).

The contrast between terrorism and pandemics is a sobering one, as pandemics kill far more people, yet somehow don’t provoke anywhere near as committed a response.

9/11 was a massive outlier in terrorism, at 3,000 deaths on a single day; otherwise the average annual death rate by terrorism is about 20,000 worldwide, mostly committed by Islamist groups. Yet the threat is not actually to Americans in particular; annual deaths due to terrorism in the US are less than 100—and most of these by right-wing domestic terrorists, not international Islamists.

Were we prepared to respond so aggressively to pandemics? Certainly not to influenza; we somehow treat all those deaths are normal or inevitable. In response to COVID we did spend a great deal of money, even more than the wars in fact—a total of nearly $6 trillion. This was a very pleasant surprise to me (it’s the first time in my lifetime I’ve witnessed a serious, not watered-down Keynesian fiscal stimulus in the United States). And we imposed lockdowns—but these were all-too quickly removed, despite the pleading of public health officials. It seems to be that our governments tried to impose an aggressive response, but then too many of the citizens pushed back against it, unwilling to give up their “freedom” (read: convenience) in the name of public safety.

For the wars, all most of us had to do was pay some taxes and sit back and watch; but for the pandemic we were actually expected to stay home,wear masks, and get shots? Forget it.

Politics was clearly a very big factor here: In the US, the COVID death rate map and the 2020 election map look almost equivalent: By and large, people who voted for Biden have been wearing masks and getting vaccinated, while people who voted for Trump have not.

But pandemic response is precisely the sort of thing you can’t do halfway. If one area is containing a virus and another isn’t, the virus will still remain uncontained. (As some have remarked, it’s rather like having a “peeing section” of a swimming pool. Much worse, actually, as urine contains relatively few bacteria—but not zero—and is quickly diluted by the huge quantities of water in a swimming pool.)

Indeed, that seems to be what has happened, and why we can’t seem to return to normal life despite months of isolation. Since enough people are refusing to make any effort to contain the virus, the virus remains uncontained, and the only way to protect ourselves from it is to continue keeping restrictions in place indefinitely.

Had we simply kept the original lockdowns in place awhile longer and then made sure everyone got the vaccine—preferably by paying them for doing it, rather than punishing them for not—we might have been able to actually contain the virus and then bring things back to normal.

But as it is, this is what I think is going to happen: At some point, we’re just going to give up. We’ll see that the virus isn’t getting any more contained than it ever was, and we’ll be so tired of living in isolation that we’ll finally just give up on doing it anymore and take our chances. Some of us will continue to get our annual vaccines, but some won’t. Some of us will continue to wear masks, but most won’t. The virus will become a part of our lives, just as influenza did, and we’ll convince ourselves that millions of deaths is no big deal.

Most of us don’t cross borders all that often, and when we do it’s generally only for brief visits; so we don’t often experience just how absurdly difficult it is to move to another country. I have received a crash course in the subject for the past couple of months, in trying to arrange my move to Edinburgh.

Certain portions of the move would be inherently difficult: Moving a literal ton of stuff across an entire ocean is no mean feat, and really the impressive thing is that our civilization has reached the point where we can do it so quickly and reliably. (I do mean a literal ton: We estimated we have about 350 cubic feet and 2300 pounds of items, or 10 cubic meters and 1040 kilograms.)

But most of the real headaches have been the results of institutional policies.

First of all, there’s the fact that the university gave me so little notice. This is not entirely their fault; my understanding is that the position opened up during the spring, and they scrambled to fill it as fast as they could for the fall. Still, this has made everything that much more difficult.

More importantly, there is the matter of moving across borders.

In order to get visas to live in the UK, my fiance and I had to complete an application documenting basically our whole lives (I had to track down three parking tickets and a speeding ticket from as far back as 2011), maintain bank balances of a sufficient amount for at least 30 days (evidently poor people need not apply), and pay exorbitant fees (over $5000 in all for the two of us, which, gratefully, the university is supposed to reimburse me for). We had to upload not only our passports, but also financial documents as well as housing records to prove our relationship (in lieu of a marriage license, since we had to delay the wedding to this year due to the pandemic). But this was not enough; we had to pay even more fees to get expedited processing, and then travel to a US government office in the LA area to get our fingerprints done, and then mail our passports to another office in New York for further processing. We started this process the first week of August; we still haven’t heard back on our final approval.

Then there is the matter of moving our cat, Tootsie. UK regulations for importing a cat require an ISO-compliant microchip and certain vaccinations; this is perfectly reasonable. But they also require that you bring the cat with you when you move (within at most 5 days of your arrival), or else the cat will be legally considered livestock and subject to a tariff of over $1000.

This would be inconvenient enough, but then there is the fact that current regulations do not allow cats to be transported into the UK in the cabin of an aircraft. If they are to be flown in, they must be brought in the cargo hold. Since we did not want to subject our cat to several hours alone in a cargo hold on a transatlantic flight, we will instead be flying to Amsterdam, because the Netherlands has more lenient regulations. But then of course we still need to get her to Edinburgh; our current plan involves taking a ferry from Amsterdam to Newcastle and then a train from there to Edinburgh. In all the whole process will take at least a day longer (and cost a few hundred dollars more) than it would have without the utterly pointless rule forbidding cats from flying into the UK in the cabin.

All of this for, and I really cannot emphasize this enough, a routine move between two NATO allied First World countries.

The alliance between the US and the UK is one of the most tightly-knit in the world, and dates back generations. Our trade networks are thoroughly interconnected, and we even share most of our media and culture back and forth. There’s honestly no particular reason we couldn’t simply be the same country. (Indeed the one thing we did fight with them about in the last 250 years was over precisely that.)

There is probably less difference culturally and economically between New York and London than there is between New York and rural Texas or between London and rural Scotland. Yet a move within each country requires basically none of this extra hassle and paperwork—you basically just physically move yourself, register your car, maybe a few other minor things. You certainly don’t need to get a passport, apply for a visa, or pay exorbitant fees.

What purpose does all of this extra regulation serve? Are we safer, or richer, or healthier, because we make it so difficult to move across borders?

I can understand the need to hve some sort of security at border crossings: We want to make sure people aren’t smuggling contraband or planning acts of terrorism. (There is, by the way, a series of questions on the UK visa application asking things like this:”Have you ever committed terrorism?” “Have you ever been implicated in genocide?” One wonders if anyone has ever answered “yes”.) It even makes sense to have some kind of registration process and background check for people who plan to move permanently. But what we actually do goes far, far beyond these sensible requirements; the goal seems to be to ensure that only the finest upstanding citizens may be allowed to move to a country, while anyone who is born on the opposite side of that line need not meet any standard whatsoever in order to remain.

In my view, the most sensible standard would be this: You should only exclude someone from entering your country for actions that you’d be willing to imprison them for if they were already there. Clearly, smuggling and terrorism qualify. Indeed, any felony would do. But would you lock someone in prison for not having enough money in their bank account? Or for failing to disclose a parking ticket from ten years ago? Or for filling out paperwork incorrectly? Yet visas are denied for this sort of reason all the time.

I think most economists would agree with me: The free movement of people across borders is one of the most vital principles of free trade—and the one that the world has least lived up to so far.

Yet it seems we are in the minority. Most people seem to think it’s perfectly sensible to have completely different rules for moving from Detroit to Toledo than from Detroit to Windsor.

The reason for this is apparent enough: Once again, the tribal paradigm looms large. Human beings divide themselves into groups, and form their identities around those groups. Those inside the group are good, while those outside are bad. Actions which benefit our own group are right, while actions which benefit other groups are wrong. The group you belong to is an inherent part of who you are, and can never be changed.

We have defined these groups in many different ways throughout human history, and our scale of group identification has gradually expanded over time. First, it was families and tribes. For centuries, it was feudal kingdoms. Now, it is nation-states. Perhaps, someday, it will enlarge to encompass all of humanity.

But until that day comes, people are going to make it as hard as possible to cross from one group to another.

It seems like an egregious understatement to say that the last couple of years have been unusual. The COVID-19 pandemic was historic, comparable in threat—though not in outcome—to the 1918 influenza pandemic.

At this point it looks like we may not be able to fully eradicate COVID. And there are still many places around the world where variants of the virus continue to spread. I personally am a bit worried about the recent surge in the UK; it might add some obstacles (as if I needed any more) to my move to Edinburgh. Yet even in hard-hit places like India and Brazil things are starting to get better. Overall, it seems like the worst is over.

This pandemic disrupted our society in so many ways, great and small, and we are still figuring out what the long-term consequences will be.

But as an economist, one of the things I found most unusual is that this recession fit Real Business Cycle theory.

Real Business Cycle theory (henceforth RBC) posits that recessions are caused by negative technology shocks which result in a sudden drop in labor supply, reducing employment and output. This is generally combined with sophisticated mathematical modeling (DSGE or GTFO), and it typically leads to the conclusion that the recession is optimal and we should do nothing to correct it (which was after all the original motivation of the entire theory—they didn’t like the interventionist policy conclusions of Keynesian models). Alternatively it could suggest that, if we can, we should try to intervene to produce a positive technology shock (but nobody’s really sure how to do that).

For a typical recession, this is utter nonsense. It is obvious to anyone who cares to look that major recessions like the Great Depression and the Great Recession were caused by a lack of labor demand, not supply. There is no apparent technology shock to cause either recession. Instead, they seem to be preciptiated by a financial crisis, which then causes a crisis of liquidity which leads to a downward spiral of layoffs reducing spending and causing more layoffs. Millions of people lose their jobs and become desperate to find new ones, with hundreds of people applying to each opening. RBC predicts a shortage of labor where there is instead a glut. RBC predicts that wages should go up in recessions—but they almost always go down.

But for the COVID-19 recession, RBC actually had some truth to it. We had something very much like a negative technology shock—namely the pandemic. COVID-19 greatly increased the cost of working and the cost of shopping. This led to a reduction in labor demand as usual, but also a reduction in labor supply for once. And while we did go through a phase in which hundreds of people applied to each new opening, we then followed it up with a labor shortage and rising wages. A fall in labor supply should create inflation, and we now have the highest inflation we’ve had in decades—but there’s good reason to think it’s just a transitory spike that will soon settle back to normal.

The recovery from this recession was also much more rapid: Once vaccines started rolling out, the economy began to recover almost immediately. We recovered most of the employment losses in just the first six months, and we’re on track to recover completely in half the time it took after the Great Recession.

This makes it the exception that proves the rule: Now that you’ve seen a recession that actually resembles RBC, you can see just how radically different it was from a typical recession.

Moreover, even in this weird recession the usual policy conclusions from RBC are off-base. It would have been disastrous to withhold the economic relief payments—which I’m happy to say even most Republicans realized. The one thing that RBC got right as far as policy is that a positive technology shock was our salvation—vaccines.

Indeed, while the cause of this recession was very strange and not what Keynesian models were designed to handle, our government largely followed Keynesian policy advice—and it worked. We ran massive government deficits—over $3 trillion in 2020—and the result was rapid recovery in consumer spending and then employment. I honestly wouldn’t have thought our government had the political will to run a deficit like that, even when the economic models told them they should; but I’m very glad to be wrong. We ran the huge deficit just as the models said we should—and it worked. I wonder how the 2010s might have gone differently had we done the same after 2008.

The European Union is one of those awkward international institutions, like the UN, NATO, and the World Bank, that doesn’t really have a lot of actual power, but is meant to symbolize international unity and ultimately work toward forming a more cohesive international government. This is probably how people felt about national government maybe 500 years ago, when feudalism was the main system of government and nation-states hadn’t really established themselves yet. Oh, sure, there’s a King of England and all that; but what does he really do? The real decisions are all made by the dukes and the earls and whatnot. Likewise today, the EU and NATO don’t really do all that much; the real decisions are made by the UK and the US.

The biggest things that the EU does are all economic; it creates a unified trade zone called the single market that is meant to allow free movement of people and goods between countries in Europe with little if any barrier. The ultimate goal was actually to make it as unified as internal trade within the United States, but it never quite made it that far. More realistically, it’s like NAFTA, but more so, and with ten times as many countries (yet, oddly enough, almost exactly the same number of people). Starting in 1999, the EU also created the Euro, a unified national currency, which to this day remains one of the world’s strongest, most stable currencies—right up there with the dollar and the pound.

Wait, the pound? Yes, the pound. While the UK entered the EU, they did not enter the Eurozone, and therefore retained their own national currency rather than joining the Euro. One of the first pieces of fallout from Brexit was a sudden drop in the pound’s value as investors around the world got skittish about the UK’s ability to support its current level of trade.

There are in fact several layers of “EU-ness”, if you will, several levels of commitment to the project of the European Union. The strongest commitment is from the Inner Six, the six founding countries (Belgium, France, the Netherlands, Luxembourg, Italy, and Germany), followed by the aforementioned Eurozone, followed by the Schengen Area (which bans passport controls among citizens of member countries), followed by the EU member states as a whole, followed by candidate states (such as Turkey), which haven’t joined yet but are trying to. The UK was never all that fully committed to the EU to begin with; they aren’t even in the Schengen Area, much less the Eurozone. So by this vote, the UK is essentially saying that they’d dipped their toes in the water, and it was too cold, so they’re going home.

Countries in the Eurozone were subject to a lot more control, via the European Central Bank controlling their money supply. The strong Euro is great for countries like Germany and France… and one of the central problems facing countries like Portugal and Greece. Strong currencies aren’t always a good thing—they cause trade deficits. And Greece has so little influence over European monetary policy that it’s essentially as if they were pegged to someone else’s currency. But the UK really can’t use this argument, because they’ve stayed on the pound all along.

The real question is what’s going to happen to the UK’s participation in the single market. I can outline four possible scenarios, from best to worst:

The single market is renegotiated, making Brexit more bark than bite: At this point, a more likely way for the UK to stop the bleeding would be to leave the EU formally, but renegotiate all the associated treaties and trade agreements so that most of the EU rules about free trade, labor standards, environmental regulations, and so on actually remain in force. This would result in a brief recession in the UK as policies take time to be re-established and markets are overwhelmed by uncertainty, but its long-term economic trajectory would remain the same. The result would be similar to the current situation in Norway, and hey, #ScandinaviaIsBetter. Probability: 40%

Balkanization of the UK: As I mentioned earlier, Scotland and Northern Ireland overwhelmingly voted against Brexit, and want no part of it. As a result, they have actually been making noises about leaving the UK if the UK decides to leave the EU. The First Minister of Scotland has proposed an “independence referendum” on Scotland leaving the UK in order to stay in the EU, and a grassroots movement in Northern Ireland is pushing for unification of all of Ireland in order to stay in the EU with the Republic of Ireland. This sort of national shake-up is basically unprecedented; parts of one state breaking off in order to stay in a larger international union? The closest example I can think of is West Germany and East Germany splitting to join NATO and the Eastern Bloc respectively, and I think we all know how well that went for East Germany. But really this is much more radical than that. NATO was a military alliance, not an economic union; nuclear weapons understandably make people do drastic things. Moreover, Germany hadn’t unified in the first place until Bismark in 1871, and thus was less than a century old when it split again. Scotland joined England to form the United Kingdom in 1707, three centuries ago, at a time when the United States didn’t even exist—indeed, George Washington hadn’t even been born. Scotland leaving the UK to stay with the EU would be like Texas leaving the US to stay in NAFTA—nay, more like Massachusetts doing that, because Scotland was a founding member of the UK and Texas didn’t become a state until 1845. While Scotland might actually be better off this way than if they go along with Brexit (and England of course even worse), this Balkanization would cast a dark shadow over all projects of international unification for decades to come, at a level far beyond what any mere Brexit could do. It would essentially mean declaring that all national unity is up for grabs, there is no such thing as a permanently unified state. I never thought I would see such a policy even being considered, much less passed; but I can’t be sure it won’t happen. My best hope is that Scotland can use this threat to keep the UK in the EU, or at least in the single market—but what if UKIP calls their bluff? Probability: 5%

Options 2 and 3 are the most likely, and actually there are intermediate cases between them; they could only implement immigration restrictions but not tariffs, for example, and that would lessen the economic fallout but still displace hundreds of thousands of people. They could only remove a few of the most stringent EU regulations, but still keep most of the good ones; that wouldn’t be so bad. Or they could be idiots and remove the good regulations (like environmental sustainability and freedom of movement) while keeping the more questionable ones (like the ban on capital controls).

Only time will tell, and the most important thing to keep in mind here is that trade is nonzero-sum. If and when England loses that $200 billion per year in trade, where will it go? Nowhere. It will disappear. That wealth—about enough to end world hunger—will simply never be created, because xenophobia reintroduced inefficiencies into the global market. Yes, it might not all disappear—Europe’s scramble for import sources and export markets could lead to say $50 billion per year in increased US trade, for example, because we’re the obvious substitute—but the net effect on the whole world will almost certainly be negative. The world will become poorer, and Britain will feel it the most.

Still, like most economists there is another emotion I’m feeling besides “What have they done!? This is terrible!”; there’s another part of my brain saying, “Wow, this is an amazing natural experiment in free trade!” Maybe the result will be bad enough to make people finally wake up about free trade, but not bad enough to cause catastrophic damage. If nothing else, it’ll give economists something to work on for years.