I’m calling it now: We officially live in the dystopian cyberpunk future. We’re not headed that way; it’s not on the horizon. It is here, now. The United States is a cyberpunk dystopia, exactly as we were warned it would become. Maybe there is still hope for the rest of the world.

I haven’t been writing blog posts as often for the last few weeks, mainly because the future feels so bleak that I can no longer tell the difference between the reality of this cyberpunk dystopia and my own crushing depression. I don’t want to add any more bleakness to the world than it already has, and I don’t even know if anything I write (or anything I do) even really matters anymore. The Fourth of July this year doesn’t feel like a birthday; it feels like a funeral.

But I couldn’t let this one go, so here we are: This man now owns 1 TRILLION DOLLARS in assets.

I want you to understand just how insane an amount of money that is. I want you to understand that no just society could ever remotely allow something like this to happen as long as there is a single child unfed or unhoused. I want you to understand that the time to reverse course on our society’s inequality was five orders of magnitude ago.

How much is 1 trillion dollars?

If you made a comfortable salary of $110,000 per year (more than most American families make), and you saved it all, spending nothing (or, equivalently, spent only the interest on your savings), it would take you nine million years to save up $1 trillion. Humans have not existed for that long. Even australopithecines hadn’t evolved yet. Nine million years ago, our ancestors were chimpanzees.

If you made $1 per second—that’s $86,500, more than most individual Americans make in a year, every single day—and likewise only spent the interest, you’d take 31,000 years to save up $1 trillion—longer than human civilization has existed. You could have started saving when the Great Pyramid was a twinkle in its architect’s eye, and you’d only have saved up 15% of the total.

If he wanted to, Elon Musk could personally end world hunger. And don’t tell me he couldn’t really do that because his wealth is tied up in stocks: UNICEF happily accepts donations in stock.

(As I understand it, SEC rules prevent Musk from selling or giving away his shares for a year after the IPO, so he couldn’t technically give away a trillion dollars today. But he could do it a year from now—and how likely do you think it is that he will?)

Did he earn this wealth?

HE COULDN’T POSSIBLY HAVE.

That is my point. No human being, no matter how great their contribution to the world, could ever possibly have earned this much wealth—and Elon Musk isn’t even on my top-100 list of greatest contributions by human beings; mostly they’d be scientists and humanitarians, but even quite a few science fiction authors and comedians should be ranked well above Elon Musk. In fact, his net contribution to humanity is pretty clearly negative. He is not the worst human to have ever lived (there’s a lot of competition for that spot, unfortunately; Stalin, maybe? Or some ancient mass murderer most people haven’t heard of?), but he is on that list, actually—or did you forget about those millions of children he sentenced to death?

He does not work a million times harder than you. He is not a million times smarter than you. He has not contributed to the world a million times more than you have. But I’m willing to bet he has a million times as much wealth as you do—because if he doesn’t, you’d have to be a millionaire, and I doubt most of my readers are millionaires.

This is the world we live in now. The dystopia is here.

They call themselves effective accelerationists, co-opting the acronym EA from Effective Altruism despite being about as diametrically opposed as it is possible to be.

They rally behind the Techno-Optimist Manifesto, which I admit makes a lot of good points and has a very seductive quality to it; but when you get to the end and reach the conclusions they draw from many reasonable-sounding premises, the result is absolute horror.

What do they want?

Totally unrestricted artificial intelligence produced as fast as possible.

Let’s be clear about this: They not only want to develop artificial intelligence (many people want that). They not only want to replace humanity with artificial intelligence (serious philosophers have suggested that this might be a long-term evolution for our civilization). They want to do it right now, without restrictions.

Their reasoning seems to go something like this:

Artificial intelligence has tremendous potential.

Improved computing has already been a tremendous boon to humanity, Applications of artificial intelligence to many fields such as scientific research and biotechnology could continue to be so.

Free-market capitalism is the most efficient economic system yet devised.

Therefore,

We should allow (or even incentivize) corporations to make artificial intelligence as powerful as possible as quickly as possible.

If we were to apply their same reasoning to other technologies, it would be obvious what’s wrong here. Consider the following argument:

Nuclear energy is tremendously powerful and very environmentally-friendly.

Cleaner, more powerful energy has been a boon to humanity, and would continue to be so if improved further.

Free-market capitalism is the most efficient economic system yet devised.

Therefore,

We should grant unrestricted access to nuclear material to anyone who is rich enough to afford it.

From three entirely reasonable premises (that honestly should be uncontroversial, even though they aren’t), we have made some kind of leap of logic to derive a conclusion that is utterly insane, and could literally result in the destruction of our entire civilization.

I agree that artificial intelligence has tremendous potential. That is why it must be kept on a tight leash.

In the near term, it is already poised to severely disrupt our economy and education system. But sufficiently-powerful AI genuinely could result in harms that could kill billions of people or even destroy human civilization. (I don’t think this will happen; but if the effective accelerationists have their way, that outcome becomes a lot more likely.)

Part of their argument seems to be that delaying new medical treatments and solutions to global problems will cost lives. This is true. But it’s far fewer lives than we would be putting at risk by pulling out all the stops and letting corporations do whatever they feel like doing.

I, too, want to see a glorious future where humanity transcends our current limits through biotechnology or cybernetics or truly-sentient artificial general intelligence. But the benefits of doing that a few years—or even decades, or even centuries—sooner are simply not worth the risk of destroying our entire civilization.

When dealing with a technology this powerful and a change this radical, the most important thing is to do it correctly—not to do it quickly. We need to make sure that the artificial intelligence we create is wise and benevolent so that its great power benefits humanity—and with this much at stake, it’s worth taking a long time to get it right if we have to.

A world run by copies of Lieutenant Commander Data would be a paradise. A world run by copies of Grok would be a hellscape. It’s worth spending some time to make sure we get the former and not the latter.

Why do I make less money than, say, Mr. Beast (who now has a game show, apparently)?

The proximal answer to this question is obvious: He has a lot more people viewing his content, so he can sell ads that make him enormous amounts of money.

But that still leaves a deeper, more ultimate question unanswered:

Why are so many people interested in that?

Mr. Beast’s first truly viral YouTube videos was literally just him counting, one by one, from 1 to 100,000. He edited the footage to speed it up slightly so that the 40-hour ordeal would fit within a 24-hour video.

This is something that literally anyone could do that literally no one benefits from.

I also can’t imagine it was particularly entertaining to watch! Like, maybe he made it a little more entertaining than you might at first imagine (I don’t know; I have no desire to watch the actual video), but I still can’t imagine it would rate among even the top 100 most interesting things to do with 24 hours—or even the top 100 most interesting things that I could do right now from the comfort of my own home.

Right now you might be thinking I’m bitter about this, but if I am bitter, it is at our economic system as a whole; I harbor no ill will toward Mr. Beast in particular, who is actually something of a philanthropist. What I really am is utterly confused.

I don’t understand why anyone—let alone millions of people—would choose to watch that video. (Though it’s a bit easier to understand if you recognize that most viewers surely did not watch the entire thing.) I don’t understand how a man can make a highly successful career doing stupid stunts on video.

And I’m also quite certain that if I, right now, tried to do some similarly stupid stunt and post it on YouTube, it would get maybe a few dozen hits and nothing more would come of it.

Maybe Mr. Beast has something I don’t: A charm, a charisma, a salesmanship. Maybe he is spectacularly persistent in a way that I really can’t be (one certainly must be that to count to 100,000!). He likely is utterly unfazed by rejection, while I am severely oversensitive to it. So I’m not making the claim that there is nothing about Mr. Beast’s individual characteristics or talents that contributed to his success.

But I think it’s pretty clear at this point that the most important reason for Mr. Beast’s success is in fact no reason at all; his video is just the one that happened to go viral at that particular moment, and he managed to leverage that publicity into making yet more viral videos until he could become a multi-millionaire for doing stupid stunts in front of a webcam.

He is what I propose we call a stochastic superstar.

His success is not driven by talent, or intellect, or expertise; it is driven by luck. A million others have tried to imitate his exact methods and failed, not because they were any worse at it—but because he did it first.

This phenomenon is not entirely new; it certainly can be traced back at least as far as any form of mass media; radio and TV stars were often famous for no other reason that they were famous.

But I think it’s pretty clear that the Internet, and social media in particular, have made it much easier to become a stochastic superstar. Arcane, mysterious algorithms promote some content over other content in ways that hardly anyone—or perhaps literally no one, if LLMs are now involved—fully understands, and thousands of people doing basically the same thing get zero compensation for it, while one becomes rich and famous for no apparent reason.

This is not a healthy way to run an economy.

Yes, it certainly results in creating a lot of content, some of which is genuinely valuable. (Mr. Beast would not be high on my list of that either.) The Internet is an unfathomably grand and diverse place, and if you know where to look you can learn about almost anything in the world; or, you know, you can be fed complete misinformation and come away with fundamental misconceptions. Or you can just watch cat videos, which I’ll admit add some joy to the world, but probably not nearly enough to justify the amount of effort and time spent creating and viewing them.

It’s bad enough that glorifying superstars glorifies risk; but at least superstar athletes are objectively in peak physical condition and are the best players at the games they play. (I still don’t really get why people invest so much in these games, but whatever.) But it isn’t even clear that viral YouTubers are producing the best video content; they are just somehow producing the most successful video content in a way that seems basically orthogonal to actual quality or value for society.

I think this should lead us to a very important question:

Are there other systems we could use to compensate people for content?

What if ad revenue was divided evenly between all contributors to a platform, rather than just those with the highest view rates? Or what if there was some benefit to getting higher views, but there was some sort of mechanism to reduce the income inequality generated this way, like paying higher rates for views when you have fewer total views (e.g. $0.01 per view for the first 1000, $0.009 for the next 10,000, $0.008 for the next 100,000, etc.)? (Are there perverse incentives here, too? Surely. But are they worse than what we have right now?)

What if we didn’t run ads at all, but instead people paid microtransactions to subscribe to content? Patreon already sort of does this (and my Patreon is also an utter failure), but I think the transactions still aren’t micro enough. I want people to pay $0.05 to read an article—because that’s all the ad revenue they would give by reading that article anyway. Nobody should have to pay $5 to read what advertisers only pay $0.05 for. I want you to be able to see the title of a blog post and a brief snippet, and think, “Sure, I’ll pay a nickel to read that.” I don’t want you to have to decide whether you’re willing to commit to subscribing for an entire month for $5.

I would like to believe, at least, that people would be more willing to pay $0.05 to read good journalism and serious intellectual content, rather than a random guy counting to 100,000 for no reason. But even if that’s not true, at least we wouldn’t be so constantly inundated by ads!

Or what if social media platforms were maintained as public infrastructure, not yielding profits to any corporation, and instead of running ads, their hosting costs (which really are not all that high; I pay for my own hosting on this blog, for instance) were covered by tax revenue? Or what if you simply paid a subscription to use the social media site, and it was no longer used to harvest your data and target ads to you?

With an alternative system like one of the above, stochastic superstars would still be able to get famous randomly, and there are benefits (and drawbacks) that come directly from being famous; but maybe at least there would be fewer multi-millionaire YouTuber superstars and more ordinary people who are better able to make ends meet by contributing content.

But who am I kidding? This system works great for the billionaires who run it (who makes the real money off YouTube? Not Mr. Beast—Sundar Pichai.), and our government has shown very little interest in doing anything that would reduce their wealth and power. So, we can expect this, and everything else, to continue to get worse in exactly the way that cyberpunk fiction explicitly warned us it would, and our government continuing to do absolutely nothing about it!

There is a factoid in the original reporting that has people especially shocked: The website that hosted this terrifying content had 62 million visitors in just one month!

A lot of people seem to be taking this to mean that there are 62 million rapists on that website—a number so huge that, since it’s just one site and there could be many more out there, would seem to imply that a large fraction of men—or even the majority of men—are in fact rapists.

But this is completely false.

That is not what that figure means, and it is an utterly preposterous claim to begin with.

I consider it deeply irresponsible journalism to report that 62 million figure without clarification.

The site that had 62 million visitors last month is a mainstream porn site. It seems to have very poor moderation policies, and as a result users were getting away with posting this “rape academy” content on it. But the number of users who actually participated in that content was not 62 million—it was not anywhere near 62 million. It was in fact only a few thousand. This is the difference between the population of a small town and the population of France.

The story here is not “there are a huge number of rapists out there and any man you know could be implicated”. The story here is mainstream porn sites are not properly moderating their content.

Of course it’s horrible that there are any rapists in the world. But that has always been true, probably will always be true, and ultimately all we can do is try to find ways to reduce those numbers while knowing that they will never actually reach zero.

Yet the public reaction to this story seems to have completely misunderstood this.

I am particularly disturbed by Greta Christina’s response (and she is someone that I greatly respect, and whose blog I follow quite carefully):

And every time I passed a man, I thought, “Are you one of them? There were 62 million visits to the rape academy site, in one month alone. Were you one of them? Are you, not just a rapist, but a calculating, plan-ahead rapist who conspires with other men on how to commit rape?”

[…]

Comment policy: Do not try to console or reassure me. Right now that feels like gaslighting. And if I hear one whiff of “Not all men,” I will block you so hard and so fast you’ll hear the explosion on the other side of the world.

She has swallowed this false narrative that it’s 62 million rapists, and categorically refuses to be corrected on that. In fact, she says that any attempt to do so feels like gaslighting.

In fact, since there were only 1,000 participants in the “rape academy”, the probability that any man Greta Christina has ever encountered was one of them is negligible. The probability that she encountered a man who had visited that porn site is considerably higher—but that’s a very different thing entirely.

Say what you will about porn sites; there is a lot of legitimate criticism to be had there. I consider myself a sex-positive feminist, and yet I still have a lot of concerns about how the porn industry is run. But millions of men consuming perfectly legal sexual content is a completely different thing from millions of men committing premeditated rape.

Moreover, Christina is far from alone in this. I have seen a huge amount of discourse on this where someone tries to correct the obviously preposterous figure, and then a bunch of people attack them for it, saying things like:

“If you are arguing statistics, you are part of the problem.”

Seriously? Trying to get accurate figures on the prevalence of rape makes you complicit in rape? Is that what you really meant to say? Shouldn’t getting accurate figures in fact be part of the solution?

The criminology statistics on this are very clear:

The vast majority of men are not rapists.

The reason that a large fraction of women are victims of rape (the best estimates are about 20%, though you’ll often hear higher figures from less credible sources) is that rapists generally rape multiple times before they are caught. That’s a big problem! It says something very bad about how our criminal justice system operates. But it absolutely, categorically, does not mean that 20% of men are rapists.

And yes, basically all women feel vulnerable to rape and try to protect themselves from it. So in that sense, all women are affected. But it doesn’t take all men to make all women feel threatened.

In fact, the best estimates we have suggest that about 8% of men have ever committed rape. That’s honestly higher than I would have expected (my guess would have been 5%). But it still implies that over 90% of men are not rapists.

(Since the world population is over 8 billion, half of people are male, and most people are adults, the 8% figure does mean that there are in fact about 300 million rapists in the world—but there’s absolutely no way that one-fifth of all rapists in the world are on a single website coordinating their activities!)

I don’t think this is really that hard to understand; it’s the same pattern as other crimes.

What proportion of people have been victims of theft? Probably the majority, depending on the seriousness of the theft.

And basically everyone feels a need to protect themselves against theft, locking their homes and cars, keeping a close eye on their valuables, avoiding dark alleys at night, and so on.

But what proportion of people are thieves? Maybe most people have shoplifted at some point, but in terms of real, serious theft, like stealing a car or breaking into a home? Only a tiny fraction. The reason that so many people have been victimized and everyone needs to be careful is that thieves do it many times before they are stopped.

In fact, it’s fair to say that this is more true of theft than it is of rape— much less than 8% of people are car thieves or burglars, and most rapes are committed by men known to the victim, which is surely not true of serious theft. But still, over 90% of men are not rapists.

This doesn’t necessarily mean that all other men are off the hook.

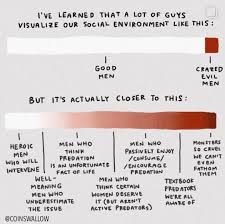

I actually really like this chart (which unfortunately I was unable to find in higher resolution, because Threads wouldn’t cooperate and I couldn’t find it anywhere else):

I have some quibbles with the categorization, to be sure: Why does “men who think predation is an unfortunate fact of life” make you worse than “well-meaning men who underestimate the issue”? Surely in some sense it is true that predation is an unfortunate fact of life: We’re never going to get that number to zero, no matter what we do. We can hopefully make it smaller, but a world with zero rapes implies some kind of global totalitarian police state (and frankly an especially benevolent and competent one at that). But maybe the intent here is that these men think there is nothing we can do to reduce rape at all, which does sound bad.

Also, what exactly does “enjoy/consume/encourage predation” mean? “enjoy/consume” seems like it could apply to rape fantasy content, which isn’t illegal—and is actually extremely popular among both men and women. I guess if we mean men who consume and enjoy actual rape content (like the “rape academy”); that sounds really bad, but it also can’t be all that many men.

But in general, I think this is a much more accurate view than either the one which says that most men aren’t rapists and therefore don’t need to do anything differently, or the view that most men are rapists and need to be taught or convinced to stop being rapists. Most men aren’t rapists, but there’s still more that they could be doing to help.

If I had to put figures on these, my guesses would be about this:

Heroic men who would intervene: 10-20%

Well-meaning men who underestimate the issue: 25-35%

Men who think there is nothing we can do about rape: 10-20%

Men who think certain women deserve it: 15-25%

Men who passively consume rape content: 5-10%

Textbook predators we’re all aware of: 5-10%

Monsters so cruel we can’t even fathom them: 1-2%

This still means that the chart is skewed; the worst categories should be much smaller than the best ones.

I might even add a better category, men who have intervened, which would surely be much smaller than the category of men who would intervene—because, contrary to the apparent belief of most feminists, most men really don’t get a lot of opportunities to intervene to stop rape. Rape happens in private, and generally rapists don’t advertise that they are planning on it or even that they have done it. Out of all the men I know in my life, only a handful of them would I reasonably suspect of committing rape at some point in their lives, and I have neither confessions nor compelling evidence to support the accusation for any of them. All I can say is they seem like thesort of man who would be willing to commit rape. (One of them I’m firmly convinced is a full-blown psychopath.) So while I absolutely would intervene to stop them if I had the opportunity to do so, I simply haven’t ever had that opportunity.

Actually I think men are even less aware of which men are dangerous than women, because women seem to have whisper networks that share this kind of information, but they rarely think to include any men in those networks. Maybe they don’t trust us enough? But I don’t understand how I’m expected to intervene when nobody has even told me who I should be intervening against.

It’s also quite likely—in fact, I dare say, nearly certain—that my own social networks are not representative of male social networks. Maybe more conventionally masculine cishet men who hang out in clubs and bars have more opportunities to intervene against rapists. It’s probably the case that most men have more experience of other men bragging about their sexual exploits in ways that may suggest predation (I have almost never experienced this, in fact).

So here’s my updated chart (which I also added more colors to, to make it clearer):

This still means that there is a lot we could do to make things better—especially about the “men who think some women deserve it” and “well-meaning men who underestimate the issue” categories, which are (in my estimation) the largest. But it’s a far cry from “any man you meet could be one of them” or “just teach men not to rape”.

And it’s never a good sign when trying to correct egregious misunderstandings is characterized as “gaslighting”.

This is a huge victory for democracy, not just in Hungary, but across Europe and indeed around the world. It brings hope in a time when we needed it most. It proves to the world that authoritarians can be toppled, and democracy can be restored—sometimes even without bloodshed.

There is a light at the end of this tunnel. We must keep pressing forward.

Second, I want to use it as a model.

I think the biggest thing that this event teaches us is that democracy and nonviolence can succeed. This is something we should already have recognized from the empirical evidence, but rarely do we see such a clear, unambiguous example of a triumphant victory by nonviolent, democratic means alone.

And once he took power, Magyar already began the process of reform. It will no doubt be a long and difficult process, and may take years to complete. Orban and his party are defeated, but not destroyed, and they will continue to mount resistance. But Magyar did not wait. He did not try to reconcile or compromise. He immediately set out to make things better.

This is what the Democrats must do when they win the midterm elections this year. They must not be timid and careful, not taking any bold moves to avoid upsetting “moderates”. (Anyone who still thinks Trump belongs anywhere near public office at this point is not and never was a moderate. At best, they might be a low-information voter who literally doesn’t know what’s going on.) They must act swiftly and decisively to repair the damage Trump has done and fix our system so that no similar maniac can do such damage again in the future. This is exactly what Biden failed to do when he took office in 2020. (Yes, I know that Congress and the Supreme Court fought him on a lot of things. But there was definitely still more that he could have done and didn’t, and people are suffering now because of it.)

Ideally, in fact, they would impeach and remove Trump before 2028. (And if it’s not too much trouble, try him at the Hague for all the children he starved?) But if they don’t manage to do that, at the very least, they must ensure that they continue to have such a strong campaign for Congress and the President in 2028 that they take both of those branches of government—and then, they need to pack the Supreme Court in order to secure the third. This damage will not be undone until Republicans are completely removed from the seats of national power, and stay removed for at least a decade.

Of course, in order for that to happen, the Democrats are going to need to win a lot of elections. And that isn’t just on them—it’s also on us. They need to run better candidates, we need to vote for those candidates, and we need to hold those candidates accountable for taking the bold measures necessary to repair America after this disaster. They need to stop taking their own electoral victories for granted: Yes, Clinton and Biden absolutely deserved to win all three elections. But they only actually won one of them, and that is what matters. The Democratic Party should be looking long and hard at what went wrong in 2016 and 2024, and learning from those mistakes.

I’m not even saying the Democrats are perfect; they are not. (Neither is Magyar.) But we need a powerful party to defeat the Republicans and restore American democracy, and only the Democrats are currently in a position to fulfill that role. After the Republicans are totally destroyed and only a distant, unsettling memory like the Nazis, then you can start voting for the Greens or the Libertarians.

And since “Magyar” basically just means “Hungarian”, maybe we should run a Presidential candidate named something like John T. American, just in case.

And yes, it matters that he has authority over nukes. If you’re in a fistfight and the other guy says, “I’ll kill you!” that’s very different than if he draws a handgun and says the same thing. The President of the United States should essentially be treated as always brandishing a deadly weapon, and it is his responsibility to have the decorum to not make statements that can be read as imminent threats.

This means that trying to be topical about current events is just too painful and disorienting for me to write anything that feels useful to say. (I mostly feel like screaming.)

So, perhaps ironically, I’m going to write a post that’s completely un-topical, that could honestly have been written any time between roughly 300 AD and the present, and—much to my chagrin—will probably still be relevant in 3000 AD if humanity survives that long.

It concerns the doctrine of scriptural inerrancy.

Simply put, inerrancy is the belief that divine scriptures (especially the Bible or Qur’an) are without error: That is, that literally every proposition contained therein is absolutely and completely true.

We can set aside the question of copyediting. I don’t care about typos or grammar mistakes. Translation errors are somewhat more serious—as they can affect real doctrines—but I’m willing to set those aside as well. We can say that we are talking about the original texts in their original languages, and idealized so that they do not contain any errors of grammar or typography.

This is already asking a lot, but I am prepared to concede it.

Even so, inerrancy is an absurdly strong claim that no rational person should ever take seriously.

The claim is that this entire text—hundreds of pages by dozens of authors over hundreds of years—is entirely true, without a single false assertion anywhere within it.

I want to be absolutely clear about this: I do not believe that about any text I have ever encountered.

I do not believe that The Origin of Species is inerrant. I do not believe that calculus textbooks are inerrant. I do not believe that Einstein’s 1905 paper on special relativity is inerrant.

I can’t point you to any specific errors in these books right now (especially since we haven’t even specified a calculus textbook), but if someone did point me to an error, I would not be the least bit surprised. Even if I combed through the entire text multiple times and didn’t spot any errors, I would still be doubtful that I hadn’t missed one somewhere.

Honestly, I find it improbable that any nonfiction work by human beings of significant length and complexity is completely without errors. (Okay, a 5-page book on counting for kindergartners might actually be inerrant. Maybe.)

Let me try putting it this way. What is the probability that any given proposition stated by a given source is correct? For a very reliable source, it could be 99%, or 99.9%, or even 99.99%. Perhaps you literally trust some sources so much that they must assert 10,000propositions before they get one wrong. (I’m not sure there’s anyone I trust this much—I certainly do not trust myself this much—but I’ll allow it for the sake of argument.)

Even if each and every proposition is 99.99% reliable, the probability that all of 30,000 distinct propositions is correct is less than 5%. Even if you trust the Bible that much, you should still be 95% certain that it got something wrong somewhere.

In fact, it’s much worse than that, as we know for a fact that there are explicit contradictions between different parts of the Bible. The Skeptic’s Annotated Bible counts over 500 explicit contradictions, some relatively trivial (did Enoch die?) but others absolutely core to Christian theology (do Heaven and Hell exist?). If even one of those holds up—and as far as I can tell, most of them hold up, maybe even all of them (though I wouldn’t be surprised if some don’t; are you getting it yet?)—then the Bible is not inerrant. Indeed, just counting contradictions, if 500 of 30,000 propositions are contradictions, then the accuracy of each proposition can’t be more than 99%.

Some of these kinds of contradictions are exactly the sort of thing you would expect to slip into a historical account that was delivered by oral tradition over multiple generations. (They do not, for instance, give me reason to doubt that there was in fact a historical figure named Yeshua of Nazareth who gathered a group of apostles and was crucified to death by the Roman state. The vast majority of historians agree that this man did, in fact, exist.)

But they are exactly what you are not allowed to have in a book that is inerrant!

A book that is literally without error, without flaw, should not contain even one single contradiction, no matter how trivial—and come on, whether or not Heaven and Hell exist is not trivial!

Inerrancy is not simply saying “the Bible is basically true” or “the Bible is a reliable source” or even “Christian theology is true.”

I believe that The Origin of Species is basically true, and a reliable source, and that Darwinian evolutionary theory is true. But I absolutely do not believe that The Origin of Species is inerrant.

I believe that most calculus textbooks are basically true, and are reliable sources, and that the Fundamental Theorem of Calculus is true. But I absolutely do not believe that any calculus textbook is inerrant.

Inerrancy isn’t even simply saying that “the Bible was written by God”! It’s very clear that the Bible is not simply dictated verbatim from On High; there was some kind of human process involved in its creation, and even if you believe that the Council of Nicaea was right about all their choices of the canon, you should still recognize that there is plenty of room for errors to have crept in during this long, convoluted, and controversial human process.

(For the Qur’an, we actually have mostly the original text by the original author—but even then, you should still be doubtful that any document with thousands of claims could be absolutely, 100% true.)

So, please, Christians, Muslims, and everyone else, I am literally begging you:

Please, give up on inerrancy. Admit that your book could be mistaken.

I’m not asking you to give up on your religion. You can keep your theology. You can still mostly believe in the book. But please, recognize how incredibly unreasonable you are being by asserting that it is impossible that anything in the book could ever be wrong.

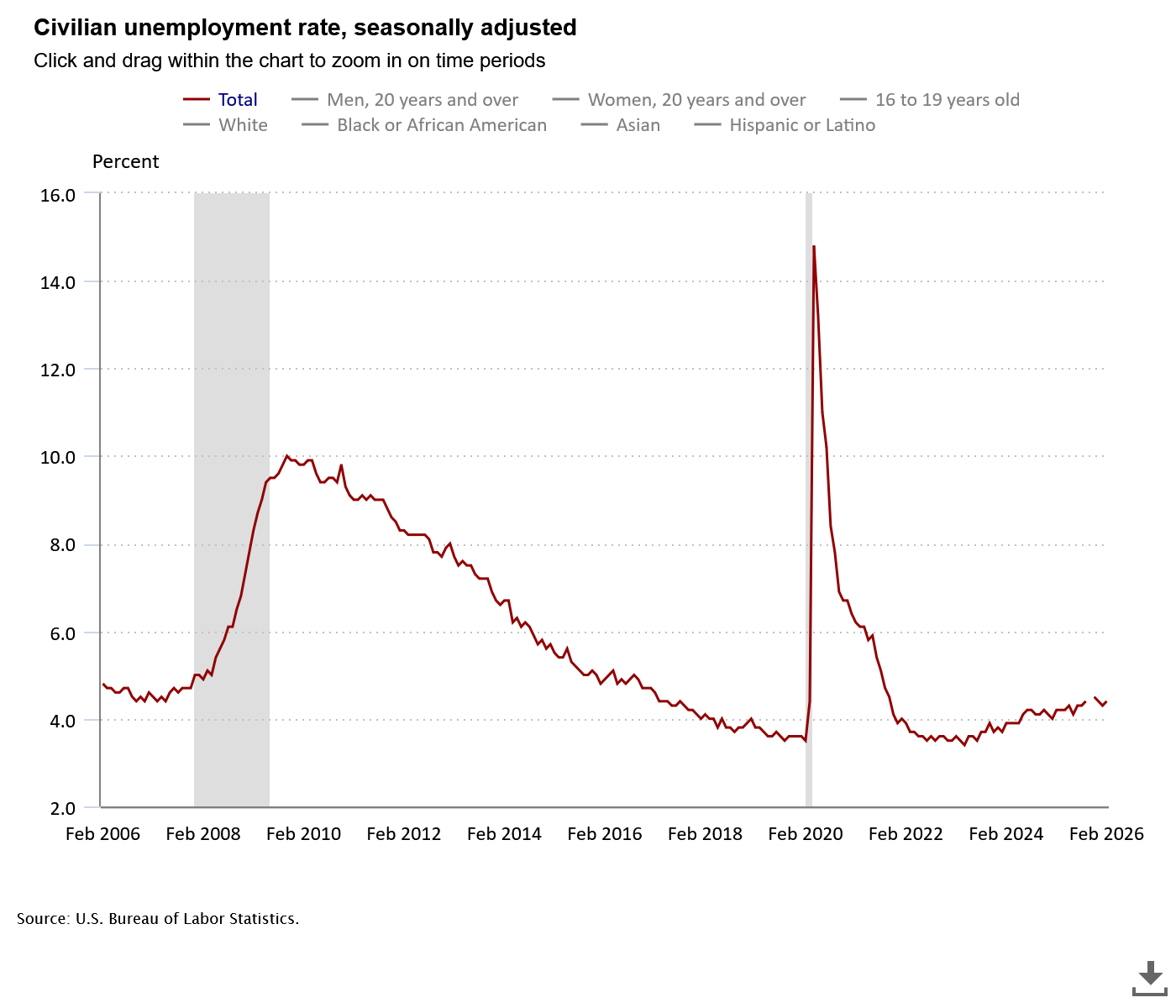

When the preliminary data for our job markets over the past few months were released, they looked all right. But after more careful analysis and better data has allowed us to revise the figures and do more accurate seasonal adjustments, the results are really quite shocking:

That is certainly something we’ve done before; it is indeed what tends to happen during recessions. But no recession has been declared, GDP seems to be growing normally, and unemployment still stands at a perfectly-reasonable 4.4%.

What’s going on here?

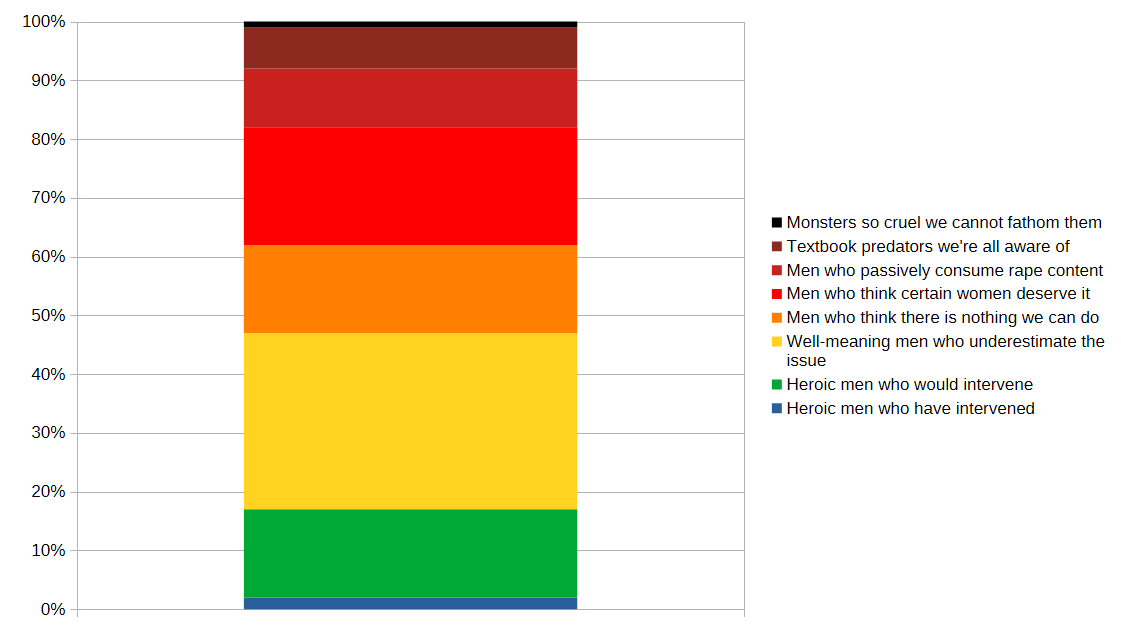

If you look at the employment level—the absolute number of people employed—it looks shockingly flat since 2023.

From 2009 to 2019, US employment grew from 138 million to 159 million, growing at 1.4% per year. Obviously it collapsed during the 2020 recession, but then it recovered to 158 million by the end of 2022. It now stands at 163 million, only 0.7% growth per year since 2022. Since January 2025 it has actually fallen from a peak of 164 million.

Because our population is growing (albeit not as much as it once was, because immigration has collapsed after Trump’s crackdowns), this actually looks even worse when you consider the employment rate, the ratio between the number of people employed and the total population:

US employment peaked at 61.1% just before the 2020 recession, and has still not recovered to that level. It reached 60% in 2022, stayed around there through 2024, and then since then has actually declined, now to 59.3%. In fact, it was even higher in 2007 before the other big recession of my adult life (you know, it’s starting to feel like the economy hates Millennials in particular), reaching 63.3% before crashing and never recovering.

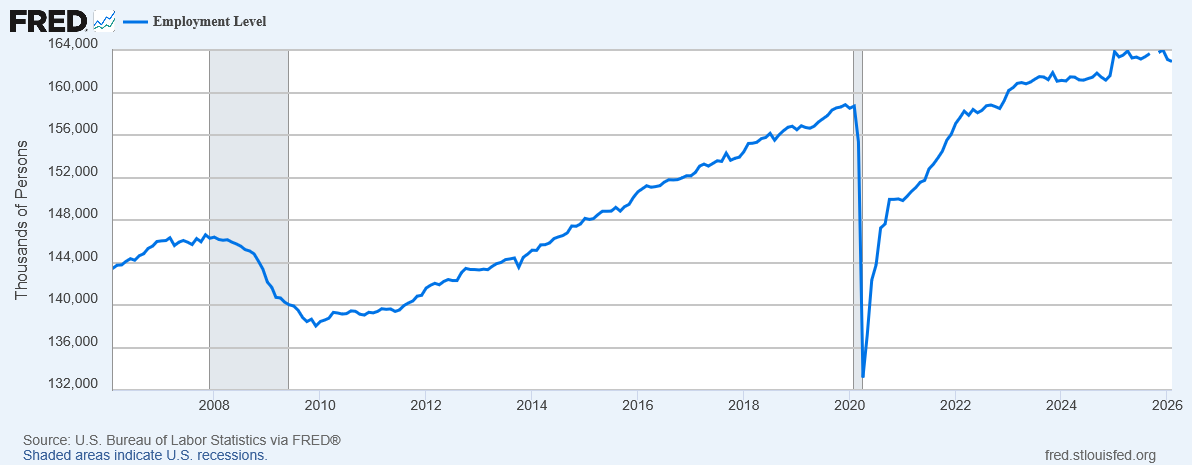

Sure, it had a huge drop in the 2020 recession, but it grew very fast in the recovery, and since then has fluctuated a bit, but generally averaged about 2.5% per year—which is pretty good for a highly-developed country. We had negative growth in the first quarter of 2025 and slow growth in the fourth quarter, but the second and third quarter both had strong growth to make up for it. Overall real GDP growth for 2025 as a whole was a perfectly respectable 2.1%.

Even our unemployment rate looks fine—though with employment falling, it suggests more people are leaving the labor force instead of looking for jobs at all.

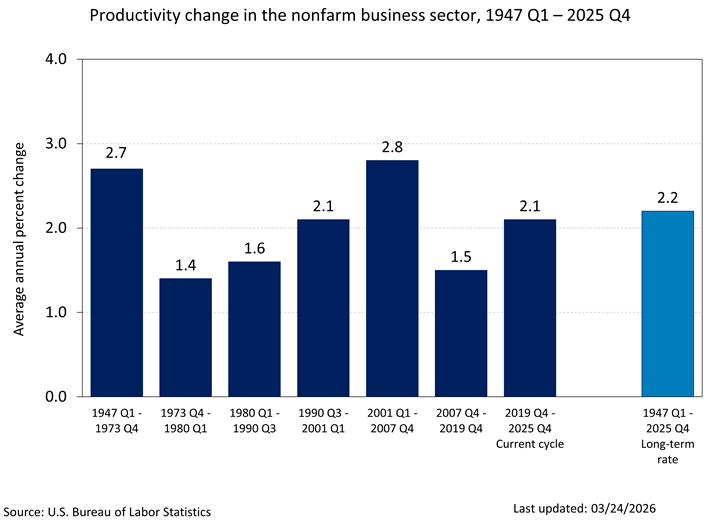

This actually looks like what you’d expect to happen under technological unemployment: Productivity-enhancing technology allows GDP to increase even as employment falls.

Overall, our productivity growth looks… pretty normal, by historical standards:

Instead, what actually seems to be happening is what we might call techno-hype unemployment: Employers think that a massive productivity surge is around the corner, and they’ve already stopped hiring in anticipation of that.

Unemployment isn’t rising very much, not because people are finding jobs, but because people who already have jobs are generally keeping them, while people who don’t have jobs are basically giving up.

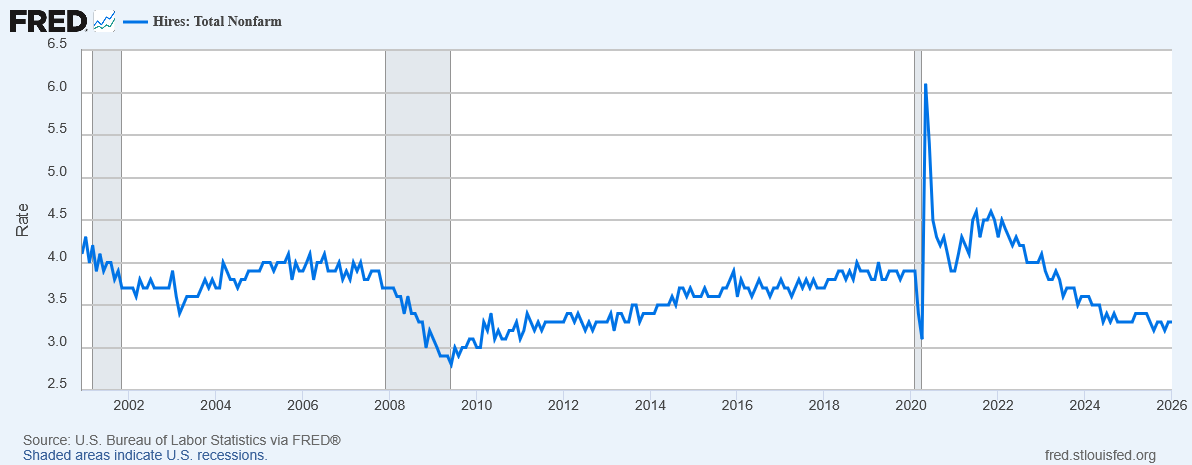

The hiring rate is now the lowest it has been since the 2020 recession—and not much higher than it was at the trough of the 2020 recession!

As far as I can tell, on our current path, one of two things will happen:

The current paradigm of AI will work, and genuinely increase productivity.

The current paradigm of AI will fail, and expected productivity gains will not materialize.

It turns out that neither possibility looks good for workers.

If AI succeeds, then businesses seem like they’re gonna just… stop hiring, especially entry-level positions that can be more readily replaced. People who already have senior positions may do just fine, or even make more money; but anyone fresh out of college, or even anyone whose career got derailed and is trying to start again, looks like they’ll just be… out of luck.

It’s every capitalist’s dream: To buy a machine that lets you never have to hire anyone ever again. And maybe, at last, they’ve found that Holy Grail.

On the other hand, if AI fails, the bubble will burst, the huge amount of investment that was previously driving the economy will suddenly dry up, and we will have a financial crisis and a recession. Businesses that were so sure they could replace their workers with AI will want to start hiring again, but won’t be able to, because no one can afford to buy anything and so nobody is making any revenue to pay employees with.

In many ways, the second one appears to be the preferable outcome, because at least it’s temporary. We would, sooner or later, recover from that recession and bring things back to normal. If AI ever actually works even half as well as most of the tech industry claims it will any minute, the most likely outcome seems to be launching us fully into a cyberpunk dystopia where a handful of trillionaires own everything and the rest of us struggle for scraps because our skills can now be replaced by machines.

This didn’t have to happen.

Even if AI is really going to be a transformational technology, we could have prepared for it better. We could have implemented policies that would ensure that people would continue to be provided for even as their labor was more and more replaced by machines. But that would have made the billionaires slightly less rich, and it sounded like “socialism” to ideologues, and the right-wing media convinced millions of people that even moving slightly in that direction would destroy all they held dear.

It’s not even too late! We could still turn it around, if those same people who stopped us from doing the right thing before weren’t still in charge of everything and richer than ever and just as effective as they ever were at deluding the masses.

I don’t know how to be optimistic about the future anymore. It feels like I’m watching the collapse of our entire civilization live in real time.

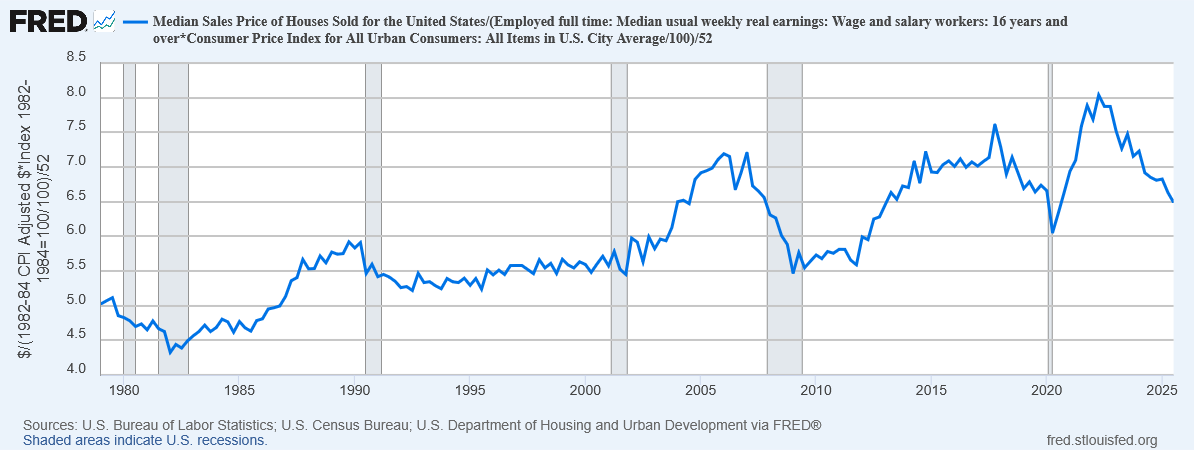

The graph below, constructed from FRED data, provides a simple measure of housing affordability: How many years of median earnings does it take to afford the median home?

From a low of 4.4 in 1982, this rose to about 5.5 and was relatively stable in the 1990s. Then in the 2000s, it began to rise, peaked at 7.2 just before the housing crisis, and then rapidly dropped to back to 5.5 again.

Then in the 2010s it began to rise again, peaked even higher at 7.6 in 2017, and then dropped down to 6.0 in 2020 before beginning to rise anew. In 2023 it reached a yet higher peak of 8.0, and then has been slowly declining ever since—but is still about 6.5, well above its 1990s level.

I honestly expected worse than this, but I think part of what’s happening is that new homes have gotten a bit smaller in the past few years: median square footage of homes sold has fallen from a peak of 1997 in 2019 to 1788 today. (Unfortunately, FRED doesn’t have this data series going back any earlier than 2016.)

If we adjust for that, the price a typical 2019 home today would be about 7.2 years of median earnings, which is about what it was at the peak of the housing crisis in 2007.

Note of course this isn’t actually how many years you need to save up to buy a house. You clearly can’t save your entire earnings, but you also don’t need to come up with the full price, only the down payment. And what you can afford also depends upon interest rates and such. But still, it’s a pretty clear sign that housing is radically more expensive now than it was in the 1980s or even 1990s.

In my view, this is the affordability crisis.

Gas prices really aren’t that important. Car prices are relatively stable. Food prices are volatile but don’t have a bad long-term trend. We do still have serious problems with affordability in education and healthcare, but we have obvious solutions available (that several other countries are already doing successfully); we’re just not doing them because Republicans don’t like them. But housing? We have no clear solutions on the table, certainly not anything that would be politically viable. Fundamentally, we need to build more housing in places people want to live—a lot more housing—and force the price of housing down.

And with our society structured the way it is, when you price people out of housing, you price them out of adulthood. Millennials are not having kids at anywhere near the rate of previous generations, because raising kids requires living space. Especially with immigration collapsing after Trump, this housing affordability crisis is going to turn into a population crisis.

I guess what I’m hoping for at the moment is just consciousness-raising, making people see that this is actually a problem. For some reason, everyone agrees that rising prices of goods are a bad thing, except when it comes to housing.

Inflation in food? An urgent crisis that must be immediately resolved.

Inflation in gas prices? So terrible it’s worth invading other countries over.

Inflation in housing? No, somehow that’s good actually, because it makes homeowners feel richer (even though they actually owe more in property taxes). We treat housing like an asset instead of a good, which is something we should absolutely never, ever do with a good that people need to live.

Many religions teach that love is a gift from God, perhaps the greatest of all such gifts; indeed, some even say “God is love” (though I confess I have never been entirely sure what that sentence is intended to mean). But if there is no God, what is love? Does it still have meaning?

I believe that it does.

Yes, there is a cynical account of love often associated with atheism, which is that it is “just a chemical reaction” or “just an evolved behavior”. (An easy way to look out for this sort of cynical account is to look for the word “just”.)

Well, if love is a chemical reaction, so is consciousness—indeed the two seem very deeply related. I suppose a being can be conscious without being capable of love (do psychopaths qualify?), but I certainly do not think a being can be capable of love without being conscious.

Indeed, I contend that once you really internalize the Basic Fact of Cognitive Science, “just a chemical reaction” strikes you as an utterly trivial claim: What isn’t a chemical reaction? That’s just a funny way of saying something exists.

What about being an evolved behavior? Yes, this is a much more insightful account of what love is, what it means—what it’s for, even. It evolved to make us find mates, protect offspring, and cooperate in groups.

And I can hear the response coming: “Is that all?” “Is it just that?” (There’s that “just” again.)

So let me try phrasing it another way:

Love is what makes us human.

If there is one thing that human beings are better at than anything in the known universe, one thing that most absolutely characterizes who and what we are, it is love.

Intelligence? Rationality? Reasoning? Oh, sure, for the first half-million years of our existence, we were definitely on top; but now, I think computers have got us beat on those. (I guess it’s hard to say for sure if Claude is truly intelligent, but I can tell you this: Wolfram Alpha is a lot better at calculus than I’ll ever be, and I will never win a game of Go against AlphaZero.)

Strength? Ridiculous! By megafauna standards—even ape standards—we’re pathetic. Speed? Not terrible, but of course the cheetahs and peregrine falcons have us beat. Endurance? We’re near the top, but so are several other species—including horses, which we’ve made good use of. Durability? Also surprisingly good—we’re tougher than we look—but we still hold no candles to a pachyderm. (You need special guns to kill an elephant, because most standard bullets barely pierce their skin. And standard bullets were, more or less by construction, designed to kill humans.) We do throw exceptionally well, so if you’d like, you can say that the essence of humanity is javelin-throwing—or perhaps baseball.

But no, I think it is love that sets us apart.

Not that other animals are incapable of love; far from it. Almost all mammals and birds express love to their offspring and often their partners; I would not even be sure that reptiles, fish, or amphibians are incapable of love, though their behavior is less consistently affectionate and I am thus less certain about it. (Especially when fish eat their own offspring!) In fact, I might even be prepared to say that bees feel love for their sisters and their mother (the queen). And if insects can feel it, then our world is absolutely teeming with love.

But what sets humans apart, even from other mammals, is the scale at which we are able to love. We are able to love a city, a nation, a culture. We are even able to love ideas.

I do not think this is just a metaphor: (There’s that “just” again!) I would as surely die for democracy as I would to save the life of my spouse. That love is real. It is meaningful. It is important.

Humans feel love for other humans they have never met who live thousands of miles away from them. They will even willingly accept harm to themselves to benefit those others (e.g. by donating to international charities); one can argue that most people do not do this enough, but people do actually do it, and it is difficult to explain why they would were it not for genuine feelings of caring toward people they have never met and most likely never will.

And without this, all of what we know as “human civilization” quite simply could not exist. Without our love for our countrymen, for our culture, for our shared ethical and political principles, we could not sustain these grand nation-states that span the world.

Yes, even despite our often fierce disagreements, there must be a core of solidarity between at least enough people to sustain a nation. Even authoritarian governments cannot sustain themselves when the entire population stops loving them—in fact, they seem to fail at the hands of a sufficiently well-organized four percent. (Honestly, perhaps the worst part about fascist states is that many of their people do love them, all too deeply!)

More than that, without love, we could never have created institutions like science, art, and journalism that slowly but surely accumulate knowledge that is shared with the whole of humanity. The march of progress has been slower and more fitful than I think anyone would like; but it is real, nonetheless, and in the long run humanity’s trajectory still seems to be toward a brighter future—and it is love that makes it so.

It is sometimes said that you should stop caring what other people think—but caring what other people think is what makes us human. Sure, there are bad forms of social pressure; but a person who literally does not care how their actions make other people think and feel is what we call a psychopath. Part of what it means to love someone is to care a great deal what they think. And part of what makes a good person is to have the capacity to love as much as possible.

Love binds us together not only as families, but as nations, and—hopefully, one day—it could bind humanity or even all sentient life as one united whole. Morality is a deep and complicated subject, but if you must start somewhere very simple in understanding it, you could do much worse than to start with love.

It is often said that God is what binds cultures, nations, and humanity together. With this in mind, perhaps I am prepared to assent to “God is love” after all, but let me clarify what I would mean by it:

Love does for us what people thought they needed God for.

Just listing people I had previously heard of, even aside from Donald and Melania Trump:

Woody Allen, Steve Bannon, Ehud Barak, Richard Branson, William Burns, Noam Chomsky, Deepak Chopra, Bill Clinton, David Copperfield, Bill Gates, Stephen Hawking, Michael Jackson, Thorbjørn Jagland, Lawrence Krauss, Elon Musk, Mehmet Oz, Brett Ratner, Ariane de Rothschild, Kevin Spacey, Lawrence H. Summers, Peter Thiel, Robert Trivers, and Michael Wolff.

There are of course more people who are famous for various things that I simply wasn’t familiar with, such as Anil Ambani, Peter Attia, Todd Boehly, Andrew Farkas, Brad S. Karp, and Brian Vickers. And more names may yet come out as the saga continues.

Now, some of these connections are more damning than others: At the milder end, we have Bill Gates, who doesn’t appear to have actually received (let alone responded to) the emails addressed to him, and Thorbjørn Jagland, who was planning to visit the island but apparently never actually did so. At the worse end, we have Richard Branson, who introduced Epstein to his “harem” (Branson’s word), Noam Chomsky, who had extensive exchanges and received $270,000 from a mysterious account (he claims Epstein had nothing to do with it), Lawrence Krauss and Robert Trivers, who both continued to publicly defend Epstein even after Epstein was convicted of sex crimes against children in 2008, Peter Thiel, who received $40 million from Epstein, and of course Donald Trump himself, who is mentioned in the Epstein files some 38,000 times. (That we know of.)

Even the damning ones are largely not conclusive; the documents that have been released don’t appear to be sufficient to prove anyone guilty of crimes in a court of law. But given that Donald Trump is President and is probably doing everything he can to suppress and redact any such evidence that does exist (at the very least against himself), this absence of evidence is not particularly strong evidence of absence. The best we can really say at this juncture is that it looks verysuspicious about an awful lot of famous people.

I guess it’s honestly possible that some of these people knew Epstein well but really didn’t know about his secret life sexually abusing children. Sometimes monsters can hide in plain sight. But several of these people have been credibly accused of sex crimes of their own, and many of them circled the wagons to defend each other whenever new accusations came out. And once someone pleads guilty and is convicted (as Epstein was in 2008), you really should stop defending him.

It honestly seems like QAnon wasn’t entirely wrong after all! There was a secret cabal of famous, powerful people sexually abusing children! They just got some (okay, nearly all) of the details wrong, and for some reason thought that Donald Trump was going to bring that cabal down, rather than do everything in his power to suppress and redact all files related to it and still end up being mentioned in said files over 38,000 times. But honestly, the whole idea sounded crazy to me, and apparently it was basically correct! (Even at least one Rothschild seems to have been involved!)

I am particularly disturbed by the academics on this list: Chomsky, Hawking, Krauss, Summers, and Trivers. These men are (or were) taking up scarce tenure slots at highly prestigious universities, while at best being guilty of very bad judgment, and quite likely actually guilty of serious sex crimes. Even if they aren’t actually criminals themselves, keeping them on at prestigious institutions—as several top universities did, for years, after much was already known—besmirches the reputation of those institutions and is a disservice to the many qualified academics with better reputations who would happily replace them.

To that list I might add Chopra, who has also taught at extremely prestigious universities, but doesn’t actually do much credible research, preferring instead to peddle pseudoscientific nonsense. I don’t understand why universities ever let him teach at all—frankly it’s an insult to every other applicant they haven’t hired. (Having applied to many of these institutions myself, I take it quite personally, as a matter of fact. You think he’s better than me?) Chopra’s associations with Epstein are just one more reason to cut ties with him, when they never had any reason to make ties with him in the first place.

I am not optimistic that releasing these files will accomplish very much. Like I said, none of it seems to be conclusive. Even if evidence of crimes did emerge, they’d likely be beyond the statute of limitations. All the secrecy surrounding Epstein and his cohorts actually seems to have been pretty effective at protecting them from facing punishment for their actions.

But please, please, I’m begging here, for the sake of all that is good in the world, could this at least make people stop supporting Donald Trump!?