Jun 5 JDN 2459736

The United States and United Kingdom are both very unaccustomed to inflation. Neither has seen double-digit inflation since the 1980s.

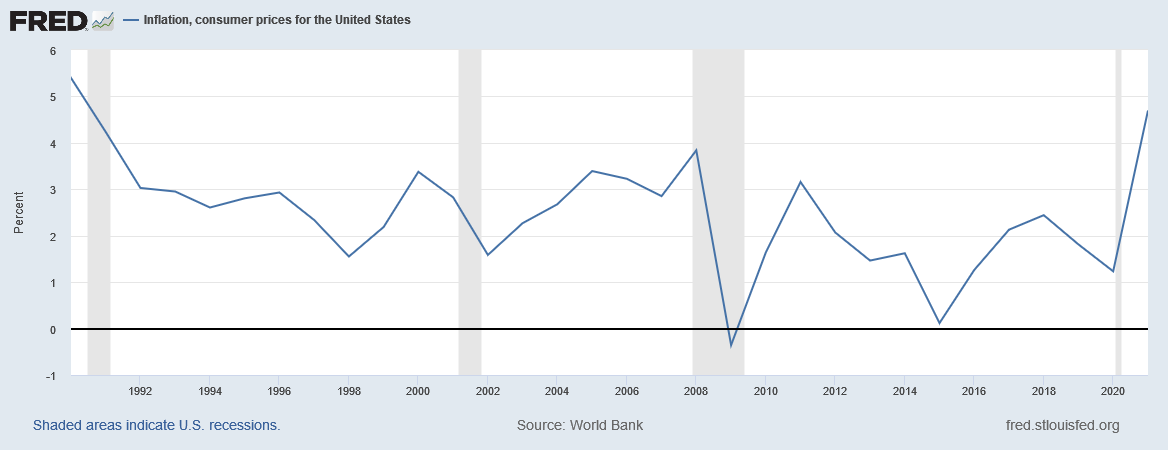

Here’s US inflation since 1990:

And here is the same graph for the UK:

While a return to double-digits remains possible, at this point it likely won’t happen, and if it does, it will occur only briefly.

This is no doubt a major reason why the dollar and the pound are widely used as reserve currencies (especially the dollar), and is likely due to the fact that they are managed by the world’s most competent central banks. Brexit would almost have made sense if the UK had been pressured to join the Euro; but they weren’t, because everyone knew the pound was better managed.

The Euro also doesn’t have much inflation, but if anything they err on the side of too low, mainly because Germany appears to believe that inflation is literally Hitler. In fact, the rise of the Nazis didn’t have much to do with the Weimar hyperinflation. The Great Depression was by far a greater factor—unemployment is much, much worse than inflation. (By the way, it’s weird that you can put that graph back to the 1980s. It, uh, wasn’t the Euro then. Euros didn’t start circulating until 1999. Is that an aggregate of the franc and the deutsche mark and whatever else? The Euro itself has never had double-digit inflation—ever.)

But it’s always a little surreal for me to see how panicked people in the US and UK get when our inflation rises a couple of percentage points. There seems to be an entire subgenre of economics news that basically consists of rich people saying the sky is falling because inflation has risen—or will, or may rise—by two points. (Hey, anybody got any ideas how we can get them to panic like this over rises in sea level or aggregate temperature?)

Compare this to some other countries thathave real inflation: In Brazil, 10% inflation is a pretty typical year. In Argentina, 10% is a really good year—they’re currently pushing 60%. Kenya’s inflation is pretty well under control now, but it went over 30% during the crisis in 2008. Botswana was doing a nice job of bringing down their inflation until the COVID pandemic threw them out of whack, and now they’re hitting double-digits too. And of course there’s always Zimbabwe, which seemed to look at Weimar Germany and think, “We can beat that.” (80,000,000,000% in one month!? Any time you find yourself talking about billion percent, something has gone terribly, terribly wrong.)

Hyperinflation is a real problem—it isn’t what put Hitler into power, but it has led to real crises in Germany, Zimbabwe, and elsewhere. Once you start getting over 100% per year, and especially when it starts rapidly accelerating, that’s a genuine crisis. Moreover, even though they clearly don’t constitute hyperinflation, I can see why people might legitimately worry about price increases of 20% or 30% per year. (Let alone 60% like Argentina is dealing with right now.) But why is going from 2% to 6% any cause for alarm? Yet alarmed we seem to be.

I can even understand why rich people would be upset about inflation (though the magnitudeof their concern does still seem disproportionate). Inflation erodes the value of financial assets, because most bonds, options, etc. are denominated in nominal, not inflation-adjusted terms. (Though there are such things as inflation-indexed bonds.) So high inflation can in fact make rich people slightly less rich.

But why in the world are so many poor people upset about inflation?

Inflation doesn’t just erode the value of financial assets; it also erodes the value of financial debts. And most poor people have more debts than they have assets—indeed, it’s not uncommon for poor people to have substantial debt and no financial assets to speak of (what little wealth they have being non-financial, e.g. a car or a home). Thus, their net wealth position improves as prices rise.

The interest rate response can compensate for this to some extent, but most people’s debts are fixed-rate. Moreover, if it’s the higher interest rates you’re worried about, you should want the Federal Reserve and the Bank of England not to fight inflation too hard, because the way they fight it is chiefly by raising interest rates.

In surveys, almost everyone thinks that inflation is very bad: 92% think that controlling inflation should be a high priority, and 90% think that if inflation gets too high, something very bad will happen. This is greater agreement among Americans than is found for statements like “I like apple pie” or “kittens are nice”, and comparable to “fair elections are important”!

I admit, I question the survey design here: I would answer ‘yes’ to both questions if we’re talking about a theoretical 10,000% hyperinflation, but ‘no’ if we’re talking about a realistic 10% inflation. So I would like to see, but could not find, a survey asking people what level of inflation is sufficient cause for concern. But since most of these people seemed concerned about actual, realistic inflation (85% reported anger at seeing actual, higher prices), it still suggests a lot of strong feelings that even mild inflation is bad.

So it does seem to be the case that a lot of poor and middle-class people really strongly dislike inflation even in the actual, mild levels in which it occurs in the US and UK.

The main fear seems to be that inflation will erode people’s purchasing power—that as the price of gasoline and groceries rise, people won’t be able to eat as well or drive as much. And that, indeed, would be a real loss of utility worth worrying about.

But in fact this makes very little sense: Most forms of income—particularly labor income, which is the only real income for some 80%-90% of the population—actually increases with inflation, more or less one-to-one. Yes, there’s some delay—you won’t get your annual cost-of-living raise immediately, but several months down the road. But this could have at most a small effect on your real consumption.

To see this, suppose that inflation has risen from 2% to 6%. (Really, you need not suppose; it has.) Now consider your cost-of-living raise, which nearly everyone gets. It will presumably rise the same way: So if it was 3% before, it will now be 7%. Now consider how much your purchasing power is affected over the course of the year.

For concreteness, let’s say your initial income was $3,000 per month at the start of the year (a fairly typical amount for a middle-class American, indeed almost exactly the median personal income). Let’s compare the case of no inflation with a 1% raise, 2% inflation with a 3% raise, and 5% inflation with a 6% raise.

If there was no inflation, your real income would remain simply $3,000 per month, until the end of the year when it would become $3,030 per month. That’s the baseline to compare against.

If inflation is 2%, your real income would gradually fall, by about 0.16% per month, before being bumped up 3% at the end of the year. So in January you’d have $3,000, in February $2,995, in March $2,990. Come December, your real income has fallen to $2,941. But then next January it will immediately be bumped up 3% to $3,029, almost the same as it would have been with no inflation at all. The total lost income over the entire year is about $380, or about 1% of your total income.

If inflation instead rises to 6%, your real income will fall by 0.49% per month, reaching a minimum of $2,830 in December before being bumped back up to $3,028 next January. Your total loss for the whole year will be about $1110, or about 3% of your total income.

Indeed, it’s a pretty good heuristic to say that for an inflation rate of x% with annual cost-of-living raises, your loss of real income relative to having no inflation at all is about (x/2)%. (This breaks down for really high levels of inflation, at which point it becomes a wild over-estimate, since even 200% inflation doesn’t make your real income go to zero.)

This isn’t nothing, of course. You’d feel it. Going from 2% to 6% inflation at an income of $3000 per month is like losing $700 over the course of a year, which could be a month of groceries for a family of four. (Not that anyone can really raise a family of four on a single middle-class income these days. When did The Simpsons begin to seem aspirational?)

But this isn’t the whole story. Suppose that this same family of four had a mortgage payment of $1000 per month; that is also decreasing in real value by the same proportion. And let’s assume it’s a fixed-rate mortgage, as most are, so we don’t have to factor in any changes in interest rates.

With no inflation, their mortgage payment remains $1000. It’s 33.3% of their income this year, and it will be 33.0% of their income next year after they get that 1% raise.

With 2% inflation, their mortgage payment will also fall by 0.16% per month; $998 in February, $996 in March, and so on, down to $980 in December. This amounts to an increase in real income of about $130—taking away a third of the loss that was introduced by the inflation.

With 6% inflation, their mortgage payment will also fall by 0.49% per month; $995 in February, $990 in March, and so on, until it’s only $943 in December. This amounts to an increase in real income of over $370—again taking away a third of the loss.

Indeed, it’s no coincidence that it’s one third; the proportion of lost real income you’ll get back by cheaper mortgage payments is precisely the proportion of your income that was spent on mortgage payments at the start—so if, like too many Americans, they are paying more than a third of their income on mortgage, their real loss of income from inflation will be even lower.

And what if they are renting instead? They’re probably on an annual lease, so that payment won’t increase in nominal terms either—and hence will decrease in real terms, in just the same way as a mortgage payment. Likewise car payments, credit card payments, any debt that has a fixed interest rate. If they’re still paying back student loans, their financial situation is almost certainly improved by inflation.

This means that the real loss from an increase of inflation from 2% to 6% is something like 1.5% of total income, or about $500 for a typical American adult. That’s clearly not nearly as bad as a similar increase in unemployment, which would translate one-to-one into lost income on average; moreover, this loss would be concentrated among people who lost their jobs, so it’s actually worse than that once you account for risk aversion. It’s clearly better to lose 1% of your income than to have a 1% chance of losing nearly all your income—and inflation is the former while unemployment is the latter.

Indeed, the only reason you lost purchasing power at all was that your cost-of-living increases didn’t occur often enough. If instead you had a labor contract that instituted cost-of-living raises every month, or even every paycheck, instead of every year, you would get all the benefits of a cheaper mortgage and virtually none of the costs of a weaker paycheck. Convince your employer to make this adjustment, and you will actually benefit from higher inflation.

So if poor and middle-class people are upset about eroding purchasing power, they should be mad at their employers for not implementing more frequent cost-of-living adjustments; the inflation itself really isn’t the problem.

People like predictability and the idea that someone is in control. Sudden changes are anxiogenic.

LikeLike

[…] lot of people seem really upset about inflation. I’ve previously discussed why this is a bit weird; inflation really just isn’t that bad. In fact, I am increasingly concerned that the usual […]

LikeLike