This post will go live on my 37th birthday. I’m now at an age where birthdays don’t really feel like a good thing.

This past year has been one of my worst ever.

It started with returning home from the UK, burnt out, depressed, suffering from frequent debilitating migraines. I had no job prospects, and I was too depressed to search for any. I moved in with my mother, who lately has been suffering health problems of her own.

Gradually, far too gradually, some aspects of my situation improved; my migraines are now better controlled, my depression has been reduced. I am now able to search for jobs at least—but I still haven’t found one. I would say that my mother’s health is better than it was—but several of her conditions are chronic, and much of this struggle will continue indefinitely.

I look back on this year feeling shame, despair, failure and defeat. I haven’t published anything—either fiction, nonfiction, or scientific—in years, and after months of searching I still haven’t found a job that would let me and my husband move to a home of our own. My six figures of student debt are now in forbearance, because the SAVE plan was struck down in court. (At least they’re not accruing interest….) I can’t think of anything I’ve done this year that I would count as a meaningful accomplishment. I feel like I’m just treading water, trying not to drown.

I see others my age finding careers, buying homes, starting families. Honestly they’re a little old to be doing these things now—we Millennials have drawn the short straw on homeownership for sure. (The median age of first-time homebuyers is now 38 years old—the highest ever recorded. In 1981, it was only 29.) I don’t see that happening for me any time soon, and I feel a deep grief over that.

I have not had a year go this badly since high school, when I was struggling even more with migraines and depression. Back then I had debilitating migraines multiple times per week, and my depression sometimes kept me from getting out of bed. I even had suicidal thoughts for a time, though I never made any plans or attempts.

Somehow, despite all that, I still managed to maintain straight As in high school and became a kind of de facto valedictorian. (My school technically didn’t have a valedictorian, but I had the best grades, and I successfully petitioned for special dispensation to deliver a much longer graduation speech than any other student.) Some would say this was because I was so brilliant, but I say it was because high school was too easy—and that this set me up for unrealistic expectations later in life. I am a poster child for Gifted Kid Syndrome and Impostor Syndrome. Honestly, maybe I would have gotten better help for my conditions sooner if my grades had slipped.

Will the coming year be better?

In some ways, probably. Now that my migraines and depression are better controlled—but by no means gone—I have been able to actively search for jobs, and I should be able to find one that fits me eventually (or so I keep trying to convince myself, when it all feels hopeless and pointless). And once I do have a job, whenever that happens, I might be able to start saving up for a home and finally move forward into feeling like a proper adult in this society.

But I look to the coming year feeling fear and dread, as Trump will soon take office and already looks primed to be far worse the second time around. In all likelihood I personally won’t suffer very much from Trump’s incompetence and malfeasance—but millions of other people will, and I don’t know how I can help them, especially when I seem so ineffectual at helping myself.

I’ve been under a great deal of stress lately. Somehow I ended up needing to finish my dissertation, get married, and move overseas to start a new job all during the same few months—during a global pandemic.

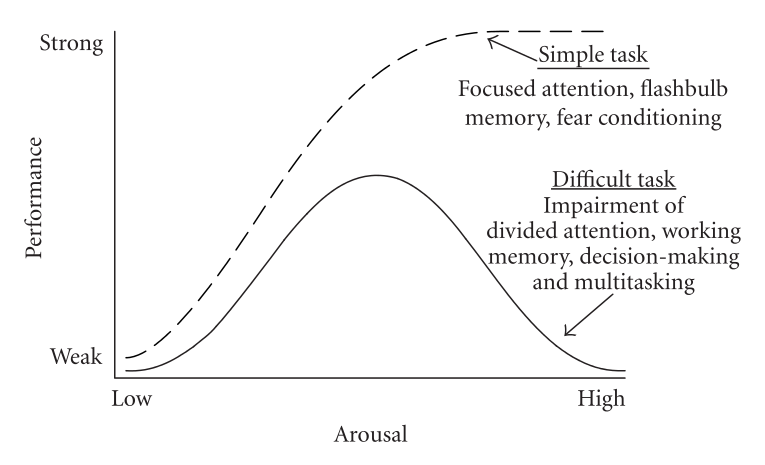

A little bit of stress is useful, but too much can be very harmful. On complicated tasks (basically anything that involves planning or careful thought), increased stress will increase performance up to a point, and then decrease it after that point. This phenomenon is known as theYerkes-Dodson law.

The Yerkes-Dodson curve very closely resembles the Laffer curve, which shows that since extremely low tax rates raise little revenue (obviously), and extremely high tax rates also raise very little revenue (because they cause so much damage to the economy), the tax rate that maximizes government revenue is actually somewhere in the middle. There is a revenue-maximizing tax rate (usually estimated to be about 70%).

Instead of a revenue-maximizing tax rate, the Yerkes-Dodson law says that there is a performance-maximizing stress level. You don’t want to have zero stress, because that means you don’t care and won’t put in any effort. But if your stress level gets too high, you lose your ability to focus and your performance suffers.

Since stress (like taxes) comes with a cost, you may not even want to be at the maximum point. Performance isn’t everything; you might be happier choosing a lower level of performance in order to reduce your own stress.

But once thing is certain: You do not want to be to the right of that maximum. Then you are paying the cost of not only increased stress, but also reduced performance.

And yet I think many of us spent a great deal of our time on the wrong side of the Yerkes-Dodson curve. I certainly feel like I’ve been there for quite awhile now—most of grad school, really, and definitely this past month when suddenly I found out I’d gotten an offer to work in Edinburgh.

My current circumstances are rather exceptional, but I think the general pattern of being on the wrong side of the Yerkes-Dodson curve is not.

For once, I think it’s actually fair to blame capitalism.

One thing capitalism is exceptionally good at is providing strong incentives for work. This is often a good thing: It means we get a lot of work done, so employment is high, productivity is high, GDP is high. But it comes with some important downsides, and an excessive level of stress is one of them.

But this can’t be the whole story, because if markets were incentivizing us to produce as much as possible, that ought to put us near the maximum of the Yerkes-Dodson curve—but it shouldn’t put us beyond it. Maximizing productivity might not be what makes us happiest—but many of us are currently so stressed that we aren’t even maximizing productivity.

I think the problem is that competition itself is stressful. In a capitalist economy, we aren’t simply incentivized to do things well—we are incentivized to do them better than everyone else. Often quite small differences in performance can lead to large differences in outcome, much like how a few seconds can make the difference between an Olympic gold medal and an Olympic “also ran”.

An optimally productive economy would be one that incentivizes you to perform at whatever level maximizes your own long-term capability. It wouldn’t be based on competition, because competition depends too much on what other people are capable of. If you are not especially talented, competition will cause you great stress as you try to compete with people more talented than you. If you happen to be exceptionally talented, competition won’t provide enough incentive!

Here’s a very simple model for you. Your total performance p is a function of two components, your innate ability aand your effort e. In fact let’s just say it’s a sum of the two: p = a + e

People are randomly assigned their level of capability from some probability distribution, and then they choose their effort. For the very simplest case, let’s just say there are two people, and it turns out that person 1 has less innate ability than person 2, so a1 < a2.

Let’s assume that the value of winning and cost of effort are the same across different people. (It would be simple to remove this assumption, but it wouldn’t change much in the results.) The value of winning I’ll call y, and I will normalize the cost of effort to 1.

Then this is each person’s expected payoff ui:

ui = (ai + ei)/(a1+e1+a2 + e2) V – ei

You choose effort, not ability, so maximize in terms of ei:

(a2 + e2) V = (a1 +e1+a2 + e2)2 = (a1 + e1) V

a1 + e1 = a2 + e2

p1 = p2

In equilibrium, both people will produce exactly the same level of performance—but one of them will be contributing more effort to compensate for their lesser innate ability.

I’ve definitely had this experience in both directions: Effortlessly acing math tests that I knew other people barely passed despite hours of studying, and running until I could barely breathe to keep up with other people who barely seemed winded. Clearly I had too little incentive in math class and too much in gym class—and competition was obviously the culprit.

If you vary the cost of effort between people, or make it not linear, you can make the two not exactly equal; but the overall pattern will remain that the person who has more ability will put in less effort because they can win anyway.

Yet presumably the amount of effort we want to incentivize isn’t less for those who are more talented. If anything, it may be more: Since an hour of work produces more when done by the more talented person, if the cost to them is the same, then the net benefit of that hour of work is higher than the same hour of work by someone less talented.

In a large population, there are almost certainly many people whose talents are similar to your own—but there are also almost certainly many below you and many above you as well. Unless you are properly matched with those of similar talent, competition will systematically lead to some people being pressured to work too hard and others not pressured enough.

But if we’re all stressed, where are the people not pressured enough? We see them on TV. They are celebrities and athletes and billionaires—people who got lucky enough, either genetically (actors who were born pretty, athletes who were born with more efficient muscles) or environmentally (inherited wealth and prestige), to not have to work as hard as the rest of us in order to succeed. Indeed, we are constantly bombarded with images of these fantastically lucky people, and by the availability heuristic our brains come to assume that they are far more plentiful than they actually are.

This dramatically exacerbates the harms of competition, because we come to feel that we are competing specifically with the people who were handed the world on a silver platter. Born without the innate advantages of beauty or endurance or inheritance, there’s basically no chance we could ever measure up; and thus we feel utterly inadequate unless we are constantly working as hard as we possibly can, trying to catch up in a race in which we always fall further and further behind.

How can we break out of this terrible cycle? Well, we could try to replace capitalism with something like the automated luxury communism of Star Trek; but this seems like a very difficult and long-term solution. Indeed it might well take us a few hundred years as Roddenberry predicted.

In the shorter term, we may not be able to fix the economic problem, but there is much we can do to fix the psychological problem.

By reflecting on the full breadth of human experience, not only here and now, but throughout history and around the world, you can come to realize that you—yes, you, if you’re reading this—are in fact among the relatively fortunate. If you have a roof over your head, food on your table, clean water from your tap, and ibuprofen in your medicine cabinet, you are far more fortunate than the average person in Senegal today; your television, car, computer, and smartphone are things that would be the envy even of kings just a few centuries ago. (Though ironically enough that person in Senegal likely has a smartphone, or at least a cell phone!)

Likewise, you can reflect upon the fact that while you are likely not among the world’s most very most talented individuals in any particular field, there is probably something you are much better at than most people. (A Fermi estimate suggests I’m probably in the top 250 behavioral economists in the world. That’s probably not enough for a Nobel, but it does seem to be enough to get a job at the University of Edinburgh.) There are certainly many people who are less good at many things than you are, and if you must think of yourself as competing, consider that you’re also competing with them.

Yet perhaps the best psychological solution is to learn not to think of yourself as competing at all. So much as you can afford to do so, try to live your life as if you were already living in a world that rewards you for making the best of your own capabilities. Try to live your life doing what you really think is the best use of your time—not your corporate overlords. Yes, of course, we must do what we need to in order to survive, and not just survive, but indeed remain physically and mentally healthy—but this is far less than most First World people realize. Though many may try to threaten you with homelessness or even starvation in order to exploit you and make you work harder, the truth is that very few people in First World countries actually end up that way (it couldbe brought to zero, if our public policy were better), and you’re not likely to be among them. “Starving artists” are typically a good deal happier than the general population—because they’re not actually starving, they’ve just removed themselves from the soul-crushing treadmill of trying to impress the neighbors with manicured lawns and fancy SUVs.

I’m traveling this week, so I have less time for blogging than usual and airlines are very much on my mind. So I thought I’d write a short post about things I would change if I were to run my own airline.

1. Instead of overpriced first-class seats, offer the option of seats with more space for a proportional amount.First class prices are almost never worth it, and people seem to be figuring that out: Use of first class is in decline. But sitting in that middle seat is so miserable, why not simply eliminate it? I think a lot of people would be willing to pay 50% more for 50% more space.

2. Offer every passenger two free checked bags, butcharge for the carry-on.Carry-on bags are far more awkward and disruptive, and slow down boarding and deboarding much more, than checked bags. The airline should be trying to incentivize passengers to use checked baggage as much as possible. I’d still give each passenger a free personal item (like a purse, backpack or laptop bag), and some people would still want a carry-on bag (e.g. for cameras that can be damaged by radiation); but most people really don’t need to have a roller bag as a carry-on.

3. Power outlets in every seat. This is a trivial amount of cost in terms of manufacturing and electricity, compared to what an airplane already requires; but it makes flying much more convenient for your passengers, and thereby allows you to demand higher prices. This is a no-brainer. (Some airlines, like Delta, already do this.)

4. Assign seats and load the plane based on the seating positions. The first boarding group should be the people who sit furthest in the back, so that no one needs to pass seated passengers in order to find their own seat. Ideally window seats would be filled before aisle seats, but since people like to board and sit together, that might not be feasible. But at the very least we can make boarding faster by seating the back rows first.

6. Explain why you need to put on your own oxygen mask first. Standard airplane safety instructions always include the line “Put on your mask before assisting others.” But since they almost never explain why, I strongly suspect that in a real emergency a lot of parents try to put on their children’s masks first and thereby needlessly endanger themselves. Wording these instructions might be tricky, because any talk of such things is bound to scare people, but the core idea is this: Hypoxia will cause delirium or unconsciousness long before it will cause permanent brain damage or death. You want to first make sure you aren’t incapacitated, and then you can help save others. If you put on your mask first, your kid may get confused or pass out, but you’ll be able to help them and they’ll be fine. If you put on your kid’s mask first, you may get confused or pass out, and your kid won’t be able to help you. Then unless someone else saves you, you may die pointlessly because you didn’t follow instructions. Depending on altitude and how severe the hull breach is, you have about 30 seconds before you lose consciousness. But your kid has at least three minutes before you need to worry about permanent brain damage, and probably as many as fifteen before they’d die.

7. Include carbon offsets in the ticket price, and advertise this aggressively. Despite the fact that airplanes are a major source of carbon emissions, carbon offsets are actually remarkably cheap compared to the cost of airline tickets. Adding offsets would typically raise the price of a ticket by about $30, which on a $300 ticket is unlikely to shock people. And by advertising the carbon-neutrality of your airline, you can probably get a lot of customers who are willing to pay more, potentially even more than the additional cost of the carbon offsets themselves. This could be a win-win for the airline and the environment.

9. Include snacks at every seat before passengers even board. Putting a bag of pretzels and a water bottle at every seat would be trivially easy, and would allow passengers the opportunity to be eating while the plane takes off—and chewing reduces the discomfort of changing air pressure. If the worry is that people will try to put their tray tables down (which is genuinely unsafe during takeoff), install electronic locks that prevent tray tables from being lowered except when authorized.

10. Install seats that don’t recline. The additional comfort for the passenger reclining is far smaller than the reduced comfort for the passenger behind them. Combine that with the additional cost of maintaining the seats and the additional risk of injury during rough landings, and the answer is obvious: Seats shouldn’t recline.

11. Offer better food. Charging less for airplane food honestly isn’t feasible: Because space and weight are at such a premium, it really is that expensive to store and transport food on an aircraft. But the cost comes mostly from the bulk and weight of the food; it really doesn’t much matter what kind of food it is. To that end, airlines should offer high-quality food that people feel more comfortable paying such high prices for. A steak weighs about the same as a hamburger, and champagne has about the same density as Sprite.

12. Reduce, or even eliminate, fees to change flights. Yes, it’s expensive to have empty seats on a moving airplane. But most flights can be filled by standby passengers, and those that can’t often weren’t full anyway. It’s actually fairly rare for a cancellation to result in an empty seat that would otherwise have been full. And the additional goodwill you get from making life easier for your passengers will make up the difference. (Southwest figured this out; other airlines don’t yet seem to have caught on.)

Would these changes revolutionize air travel? No. But I do think they’d make it a bit more pleasant, without greatly reducing the profits of the airline.

When this post goes live, it will be April 15, 2018. My father was born April 15, 1954 and died August 31, 2017, so this is the first time we will be celebrating his birthday without him.

I’m not sure that grief ever really goes away. The shock of the unexpected death fades eventually, and at last you can accept that this has really happened and make it a part of your life. But the sum total of all missed opportunities for life events you could have had together only continues to increase.

There are many cliches about this sort of thing: “Death is a part of life.” “Everything happens for a reason.” It’s all making excuses for the dragon. If we could find a way to make people stop dying, we ought to do it. The other consequences are things we could figure out later.

But, alas, we can’t, at least not in general. We have managed to cure or vaccinate against a wide variety of diseases, and as a result people do, on average, live longer than ever before in human history. But none of us live “on average”—and sometimes you get a very unlucky draw.

Yet somehow, we do learn to go on. I’m not sure how. I guess it’s a kind of desensitization: Right after my father’s death, any reminder of him was painful. But over time, that pain began to lessen. Each new reminder hurts a little less than the last, until eventually the pain is mild enough that it can mostly be ignored. It never really goes away, I think; but eventually it is below your just-noticeable-difference.

I had hoped to do more with this post. I had hoped that reflecting on the grief I’ve felt for the last several months would allow me to find some greater insight that I could share. Instead, I find myself re-writing the same sentences over and over again, trying in vain to express something that might help me, or help someone else who is going through similar grief. I keep looking for ways to distract myself, other things to think about—anything but this. Maybe there are no simple insights, no way for words to shorten the process that everyone must go through.

My father died suddenly and unexpectedly from a ruptured intracranial aneurysm. I received a call that he was in the hospital Wednesday morning at 11:30 AM PDT, took the first flight to Michigan I could find, and arrived around 10:30 PM EDT. By the time I got there, my father was already unconscious and under intensive care. I stayed up all night in the hospital. My father never regained consciousness. He was declared dead at 8:30 AM on Thursday morning.

In lieu of a proper blog post this week, I decided to post the eulogy I gave at my father’s funeral this past Sunday. It follows below.

What is a soul? What is it made of? Most people imagine a soul as something immaterial, something somehow “beyond” this physical world. But at its core, a soul is simply what makes us who we are. Today we have cognitive science, and now understand the human soul better than it was understood by all the billions of people in all the thousands of years of human civilization before us. Thanks to cognitive science, we now know what the soul is made of: It is made of information.

My father wasn’t made of some mysterious substance “beyond” our physical world, but nor was hejust the molecules of his body you see here. My father was made of hopes and dreams, laughter and tears, words and ideas. He was made of James Joyce novels and Catullus poems, Spider-Man comics and Arnold Schwarzenegger movies, road trips across America, gazes over the Grand Canyon, spelunking in Carlsbad Caverns, walks on the beaches of the Gulf of Mexico and the Pacific, warm hugs, gentle smiles, sophisticated puns, obsessive organizing, and reading literally thousands of books, on everything from Celtic literature to quantum physics. (I think he knew the former a lot better than the latter, while for me, it is the reverse.)

And coffee. Lots and lots of coffee.

Most of what my father was is now gone, and I don’t think we should try to deny that. I don’t think it’s healthy—or even effective—to tell ourselves that he isn’t really gone or that he’s in some better place. Deep down we all know the loss we feel. We know the regrets we have of all the things we thought we’d get to do together, but now we know we never will. There are three that are especially painful for me: My father will never get to see my PhD diploma, never know me as “Doctor Patrick Neal Russell Julius.” My father will never get to see my wedding. And above all, my father will never get to meet his grandchildren. If I had known, I could have tried to make these things happen sooner, so that my father would get to share them with me. I thought that I had 20 years left to do all these things with my father beside me—but the reality turned out differently. And one of the best definitions of reality is this: Reality, when you stop believing in it, doesn’t go away. We grieve this loss for a reason. It hurts so much to lose my father because we know how much joy he once brought to our lives, and how much he would have if he’d been allowed to go on living. A friend of mine offered me this aphorism: Grief is the price we pay for love.

But my father is not completely gone, either. Our souls are made of information too, and there are little fragments of my father’s soul in every one of us. Every memory we have of him, every time he touched our lives, a fragment of him was downloaded into each of us, and as long as we remember him, he will not be entirely gone.

There are a few memories in particular I’d like to share with you all know—back them up in the cloud if you will—so that the essence of who my father was will live on awhile longer. Human long-term memory is stored in the form of narrative, so I thought it best if I told a few stories.

The first story is about gentleness. We were driving through New Mexico. I had moved recently to Long Beach to study for my master’s degree at CSU; after coming back to Ann Arbor for a visit, Dad had driven with me in my little Smart car all the way across the country. We planned our route to pass the Very Large Array, a gigantic assembly of radio telescopes probably best known for being featured in the film Contact, one of my favorites, based on a Carl Sagan novel I love even more. I had wanted to see it for a long time, so Dad added a few hours to our trip so we could go past it.

When we arrived at the array, we could hardly find any people around. Instead what we found were bugs—grasshoppers I think, and millions of them. Everywhere. The ground was literally covered in them; there wasn’t even any room to walk. Most people would probably have just gone ahead and walked right on top of them, crushing them as they went—but not my father. His gentleness extended even to the lowliest of creatures, and he wanted to make sure we didn’t harm any of the bugs. So he found a way for us to creep, slowly, across the desert, shooing away the bugs at each step, so that they would give us room to pass. We didn’t step on a single grasshopper that day, and I finally got the chance to touch one of the radio telescopes.

The second story is about generosity. We had just bought a baby grand piano, and my mother was learning to play it. For her birthday she had asked for a metronome. So, my father and I went out shopping to find a nice metronome. We found one that seemed perfect, but then the store offered us one that was twice the price, and as far as I can tell, not any better whatsoever. Dad asked me, “Isn’t your mother worth it?” Already a budding economist, I had to explain, “Of course, but that’s not the question. The question is, is the metronome worth it? Save the money and we’ll buy her something else too.” But that’s how Dad was: When buying things for himself, he was frugal, even miserly; several times I saw him find rare books—first editions of Joyce, folio editions of Shakespeare—that he had wanted for decades to get, then pass them up to save $100 or maybe $200. But when buying for other people, money was no object; he’d spend that same $200 buying me another video game system without a second thought. He was generous to a fault; he’d never use his credit cards all year, then max them out every Christmas. As I got older, I actually started scaling back my Christmas lists on purpose, for fear he might go broke buying me everything I had asked for. Sometimes I think I was still a little too greedy, and should have scaled them back even more. I never was able to talk him out of buying me that folding bicycle that now sits in a corner of my apartment in Irvine—at least I talked him down from the model that cost twice as much.

The third and final story is about curiosity. Dad actually taught my high school English AP class. I was originally assigned to a different class, but in that one I was completely miserable. The very first day of class was a demonstration where he asked us all to raise our hands if we expected an A. Since this was an AP class and we were all top-achieving students, most of us did. Then the teacher asked us rhetorically: “How realistic is that?” as though there were some inherent law of the universe making such an outcome impossible. I think he saw grading as a ranking, or even a race; the notion that we could all earn mastery in the subject struck him like the notion that everyone in the Indy 500 could win first place. The next day was a quiz to see how much we remembered of the summer reading. No review, no discussion, no introduction between the students and the teacher—just the quiz. It became clear that this teacher had no interest in educating us; his goal was to evaluate us. After about a week of this I asked to be transferred to a different class. They said all they had was my dad’s class, which seemed awkward to all involved, but I decided to go with that anyway.

I ended up very glad that I had. Dad’s approach to teaching was completely different: He actually wanted us to learn. He didn’t even call them “quizzes”; they were FLAIs, spelled “F-L-A-I” which stands for “Friendly Little Assessment Instrument”. The students who were used to grade-grubbing for an extra few points found his grading system aggravating, because he refused to give a precise point tally for everything (and if you asked for one, he’d make up some nonsensical number on the spot, like “52 million” or “pi”). But the rest of us found it a breath of fresh air. We could stop worrying about how many points this quiz was worth, stop cramming for the next multiple-choice scantron exam—and actually focus our efforts on reading and learning and appreciating literature. My dad didn’t use a lot of fancy gadgets or sophisticated educational techniques; a lot of the time he was just talking and writing on a chalkboard. But his unbounded intellectual curiosity was infectious. If a student showed interest in something, he’d just start talking about that for awhile, even if it didn’t seem relevant; at first students thought this meant they could waste class time by pulling him off on a tangent. But that was never really what happened; he always managed to teach us something unexpected, and usually managed to tie it back to whatever we were studying in class. Sometimes we managed to teach him something too; usually that would be something about physics from me or something about biology from Esther Alfred or Casey Boucher. My favorite class project of all time was for my dad’s class: After reading both Vladimir Nabokov’s Pale Fire and Kurt Vonnegut’s Slaughterhouse-Five, I asked if I could write my paper about Slaughterhouse-Five in the style of Pale Fire, meaning as a series of endnotes that bear some passing relevance to the text in question, but are over-interpreted to an absurd degree to the point where they end up telling a completely different story. Most teachers would probably have balked at the idea, but Dad thought it was fabulous. I don’t think he would have thought any differently if I hadn’t been his son; he simply enjoyed nurturing his student’s creativity in that way. I probably didn’t read as many books in that class as I would have in the other English AP class; but my dad’s class fanned the flames of a love of literature that the other class would have done everything it could to extinguish.

That’s about all I have. Thank you for listening, and taking the time to be here today. The world lost a very good man this week, and I know he will be sorely missed by all of us. No words can fully capture our sorrow, but there are a few in particular I think my father would have appreciated, said always on such occasions by one of his favorite authors:

So it goes.

I don’t think most people—or even most economists—have any concept of just how fundamentally perverse and destructive our financial system has become, and a large chunk of it ultimately boils down to one thing: Selling debt.

Certainly collateralized debt obligations (CDOs), and their meta-form, CDO2s (pronounced “see-dee-oh squareds”), are nothing more than selling debt, and along with credit default swaps (CDS; they are basically insurance, but without those pesky regulations against things like fraud and conflicts of interest) they were directly responsible for the 2008 financial crisis and the ensuing Great Recession and Second Depression.

But selling debt continues in a more insidious way, underpinning the entire debt collection industry which raises tens of billions of dollars per year by harassment, intimidation and extortion, especially of the poor and helpless. Frankly, I think what’s most shocking is how little money they make, given the huge number of people they harass and intimidate.

John Oliver did a great segment on debt collections (with a very nice surprise at the end):

But perhaps most baffling to me is the number of people who defend the selling of debt on the grounds that it is a “free market” activity which must be protected from government “interference in personal liberty”. To show this is not a strawman, here’s the American Enterprise Institute saying exactly that.

So let me say this in no uncertain terms: Selling debt goes against everything the free market stands for.

One of the most basic principles of free markets, one of the founding precepts of capitalism laid down by no less than Adam Smith (and before him by great political philosophers like John Locke), is the freedom of contract. This is the good part of capitalism, the part that makes sense, the reason we shouldn’t tear it all down but should instead try to reform it around the edges.

Indeed, the freedom of contract is so fundamental to human liberty that laws can only be considered legitimate insofar as they do not infringe upon it without a compelling public interest. Freedom of contract is right up there with freedom of speech, freedom of the press, freedom of religion, and the right of due process.

The freedom of contract is the right to make agreements, including financial agreements, with anyone you please, and under conditions that you freely and rationally impose in a state of good faith and transparent discussion. Conversely, it is the right not to make agreements with those you choose not to, and to not be forced into agreements under conditions of fraud, intimidation, or impaired judgment.

Freedom of contract is the basis of my right to take on debt, provided that I am honest about my circumstances and I can find a lender who is willing to lend to me. So taking on debt is a fundamental part of freedom of contract.

But selling debt is something else entirely. Far from exercising the freedom of contract, it violates it. When I take out a loan from bank A, and then they turn around and sell that loan to bank B, I suddenly owe money to bank B, but I never agreed to do that. I had nothing to do with their decision to work with bank B as opposed to keeping the loan or selling it to bank C.

Current regulations prohibit banks from “changing the terms of the loan”, but in practice they change them all the time—they can’t change the principal balance, the loan term, or the interest rate, but they can change the late fees, the payment schedule, and lots of subtler things about the loan that can still make a very big difference. Indeed, as far as I’m concerned they have changed the terms of the loan—one of the terms of the loan was that I was to pay X amount to bank A, not that I was to pay X amount to bank B. I may or may not have good reasons not to want to pay bank B—they might be far less trustworthy than bank A, for instance, or have a far worse social responsibility record—and in any case it doesn’t matter; it is my choice whether or not I want anything to do with bank B, whatever my reasons might be.

I take this matter quite personally, for it is by the selling of debt that, in moral (albeit not legal) terms, a British bank stole my parents’ house. Indeed, not just any British bank; it was none other than HSBC, the money launderers for terrorists.

When they first obtained their mortgage, my parents did not actually know that HSBC was quite so evil as to literally launder money for terrorists, but they did already know that they were involved in a great many shady dealings, and even specifically told their lender that they did not want the loan sold, and if it was to be sold, it was absolutely never to be sold to HSBC in particular. Their mistake (which was rather like the “mistake” of someone who leaves their car unlocked and has it stolen, or forgets to arm the home alarm system and suffers a burglary) was not to get this written into the formal contract, rather than simply made as a verbal agreement with the bankers. Such verbal contracts are enforceable under the law, at least in theory; but that would require proof of the verbal contract (and what proof could we provide?), and also probably have cost as much as the house in litigation fees.

Oh, by the way, they were given a subprime interest rate of 8% despite being middle-class professionals with good credit, no doubt to maximize the broker’s closing commission. Most banks reserved such behavior for racial minorities, but apparently this one was equal-opportunity in the worst way.Perhaps my parents were naive to trust bankers any further than they could throw them.

As a result, I think you know what happened next: They sold the loan to HSBC.

Now, had it ended there, with my parents unwittingly forced into supporting a bank that launders money for terrorists, that would have been bad enough. But it assuredly did not.

By a series of subtle and manipulative practices that poked through one loophole after another, HSBC proceeded to raise my parents’ payments higher and higher. One particularly insidious tactic they used was to sit on the checks until just after the due date passed, so they could charge late fees on the payments, then they recapitalized the late fees. My parents caught on to this particular trick after a few months, and started mailing the checks certified so they would be date-stamped; and lo and behold, all the payments were suddenly on time! By several other similarly devious tactics, all of which were technically legal or at least not provable, they managed to raise my parents’ monthly mortgage payments by over 50%.

Note that it was a fixed-rate, fixed-term mortgage. The initial payments—what should have been always the payments, that’s the point of a fixed-rate fixed-term mortgage—were under $2000 per month. By the end they were paying over $3000 per month. HSBC forced my parents to overpay on a mortgage an amount equal to the US individual poverty line, or the per-capita GDP of Peru.

They tried to make the payments, but after being wildly over budget and hit by other unexpected expenses (including defects in the house’s foundation that they had to pay to fix, but because of the “small” amount at stake and the overwhelming legal might of the construction company, no lawyer was willing to sue over), they simply couldn’t do it anymore, and gave up. They gave the house to the bank with a deed in lieu of foreclosure.

And that is the story of how a bank that my parents never agreed to work with, never would have agreed to work with, indeed specifically said they would not work with, still ended up claiming their house—our house, the house I grew up in from the age of 12. Legally, I cannot prove they did anything against the law. (I mean, other than laundered money for terrorists.) But morally, how is this any less than theft? Would we not be victimized less had a burglar broken into our home, vandalized the walls and stolen our furniture?

Indeed, that would probably be covered under our insurance! Where can I buy insurance against the corrupt and predatory financial system? Where are my credit default swaps to pay me when everything goes wrong?

And all of this could have been prevented, if banks simply weren’t allowed to violate our freedom of contract by selling their loans to other banks.

Indeed, the Second Depression could probably have been likewise prevented. Without selling debt, there is no securitization. Without securitization, there is far less leverage. Without leverage, there are not bank failures. Without bank failures, there is no depression. A decade of global economic growth was lost because we allowed banks to sell debt whenever they please.

I have heard the counter-arguments many times:

“But what if banks need the liquidity?” Easy. They can take out their own loans with those other banks. If bank A finds they need more cashflow, they should absolutely feel free to take out a loan from bank B. They can even point to their projected revenues from the mortgage payments we owe them, as a means of repaying that loan. But they should not be able to involve us in that transaction. If you want to trust HSBC, that’s your business (you’re an idiot, but it’s a free country). But you have no right to force me to trust HSBC.

“But banks might not be willing to make those loans, if they knew they couldn’t sell or securitize them!” THAT’S THE POINT. Banks wouldn’t take on all these ridiculous risks in their lending practices that they did (“NINJA loans” and mortgages with payments larger than their buyers’ annual incomes), if they knew they couldn’t just foist the debt off on some Greater Fool later on. They would only make loans they actually expect to be repaid. Obviously any loan carries some risk, but banks would only take on risks they thought they could bear, as opposed to risks they thought they could convince someone else to bear—which is the definition of moral hazard.

“Homes would be unaffordable if people couldn’t take out large loans!” First of all, I’m not against mortgages—I’m against securitizationof mortgages. Yes, of course, people need to be able to take out loans. But they shouldn’t be forced to pay those loans to whoever their bank sees fit. If indeed the loss of subprime securitized mortgages made it harder for people to get homes, that’s a problem; but the solution to that problem was never to make it easier for people to get loans they can’t afford—it is clearly either to reduce the price of homes or increase the incomes of buyers. Subsidized housing construction, public housing, changes in zoning regulation, a basic income, lower property taxes, an expanded earned-income tax credit—these are the sort of policies that one implements to make housing more affordable, not “go ahead and let banks exploit people however they want”.

Remember, a regulation against selling debt would protect the freedom of contract. It would remove a way for private individuals and corporations to violate that freedom, like regulations against fraud, intimidation, and coercion. It should be uncontroversial that no one has any right to force you to do business with someone you would not voluntarily do business with, certainly not in a private transaction between for-profit corporations. Maybe that sort of mandate makes sense in rare circumstances by the government, but even then it should really be implemented as a tax, not a mandate to do business with a particular entity. The right to buy what you choose is the foundation of a free market—and implicit in it is the right not to buy what you do not choose.

There are many regulations on debt that do impose upon freedom of contract: As horrific as payday loans are, if someone really honestly knowingly wants to take on short-term debt at 400% APR I’m not sure it’s my business to stop them. And some people may really be in such dire circumstances that they need money that urgently and no one else will lend to them. Insofar as I want payday loans regulated, it is to ensure that they are really lending in good faith—as many surely are not—and ultimately I want to outcompete them by providing desperate people with more reasonable loan terms. But a ban on securitization is like a ban on fraud; it is the sort of law that protects our rights.

You may have noticed a couple of big changes in the blog today. The first is that I’ve retitled it “Human Economics” to emphasize the positive, and the second is that I’ve moved it to my domain http://patrickjuli.us which is a lot shorter and easier to type. I’ll be making two bite-sized posts a week, just as I have been piloting for the last few weeks.

Look! The “above $100,000” is the only increasing category! That means standard of living in the US is increasing! There’s no inequality problem!

The AEI has an agenda to sell you, which is that the free market is amazing and requires absolutely no intervention, and government is just a bunch of big bad meanies who want to take your hard-earned money and give it away to lazy people. They chose very carefully what data to use for this plot in order to make it look like inequality isn’t increasing.

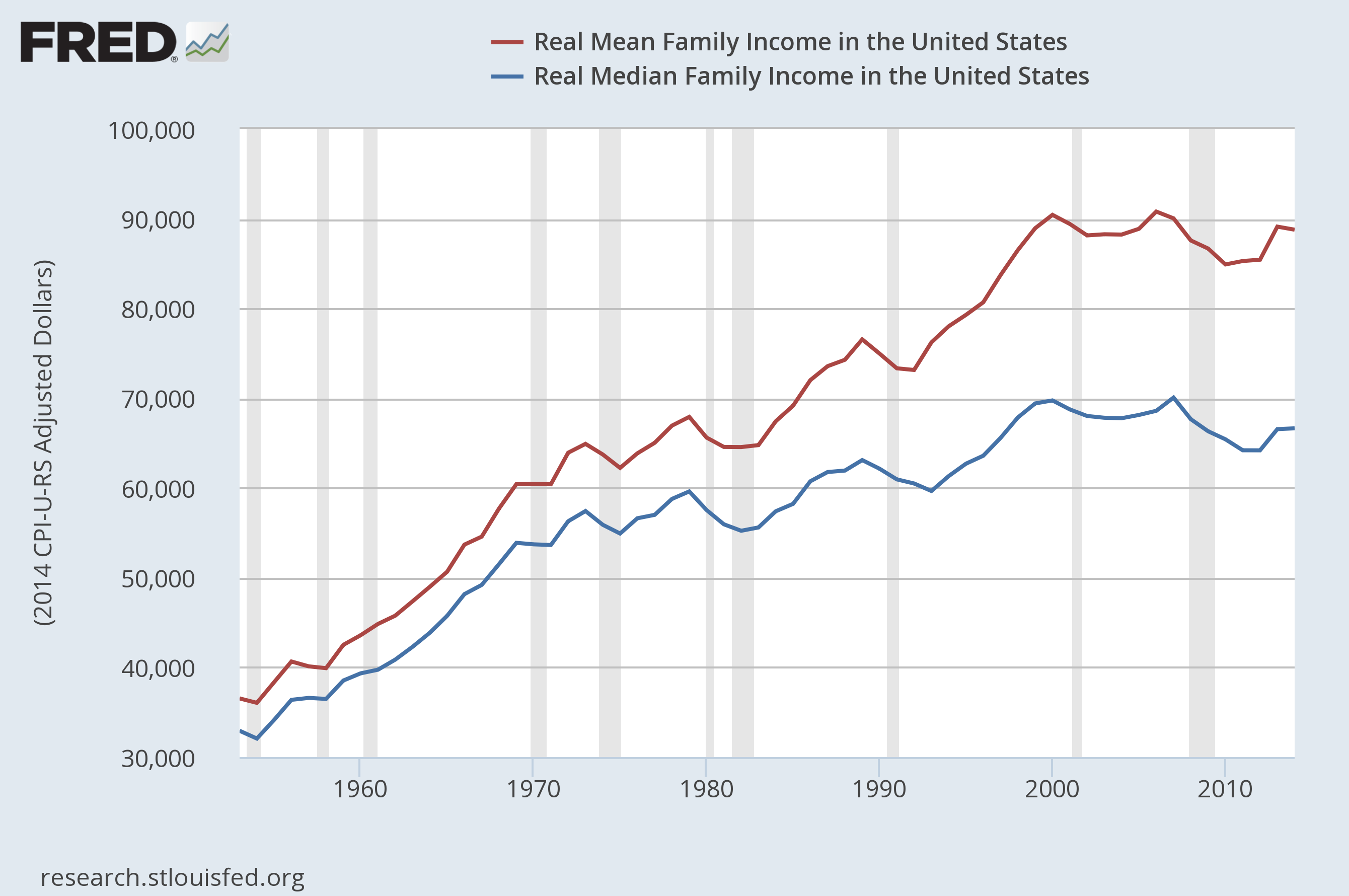

Here’s a more impartial way of looking at the situation, the most obvious, pre-theoretical way of looking at inequality: What has happened to mean income versus median income?

As a refresher from intro statistics, the mean is what you get by adding up the total money and dividing by the number of people; the median is what a person in the exact middle has. So for example if there are three people in a room, one makes $20,000, the second makes $50,000, and the third is Bill Gates making $10,000,000,000, then the mean income is $3,333,333,356 but the median income is $50,000. In a distribution similar to the power-law distribution that incomes generally fall into, the mean is usually higher than the median, and how much higher is a measure of how much inequality there is. (In my example, the mean is much higher, because there’s huge inequality with Bill Gates in the room.) This confuses people, because when people say “the average”, they usually intend the mean; but when they say “the average person”, they usually intend the median. The average person in my three-person example makes $50,000, but the average income is $3.3 billion.

So if we look at mean income versus median income in the US over time, this is what we see:

In 1953, mean household income was $36,535 and median household income was $32,932. Mean income was therefore 10.9% higher than median income.

In 2013, mean household income was $88,765 and median income was $66,632. Mean household income was therefore 33.2% higher than median income.

That, my dear readers, is a substantial increase in inequality. To be fair, it’s also a substantial increase in standard of living; these figures are already adjusted for inflation, so the average family really did see their standard of living roughly double during that period.

But this also isn’t the whole story.

First, notice that real median household income is actually about 5% lower now than it was in 2007. Real mean household income is also lower than its peak in 2006, but only by about 2%. This is why in a real sense we are still in the Second Depression; income for most people has not retained its pre-recession peak.

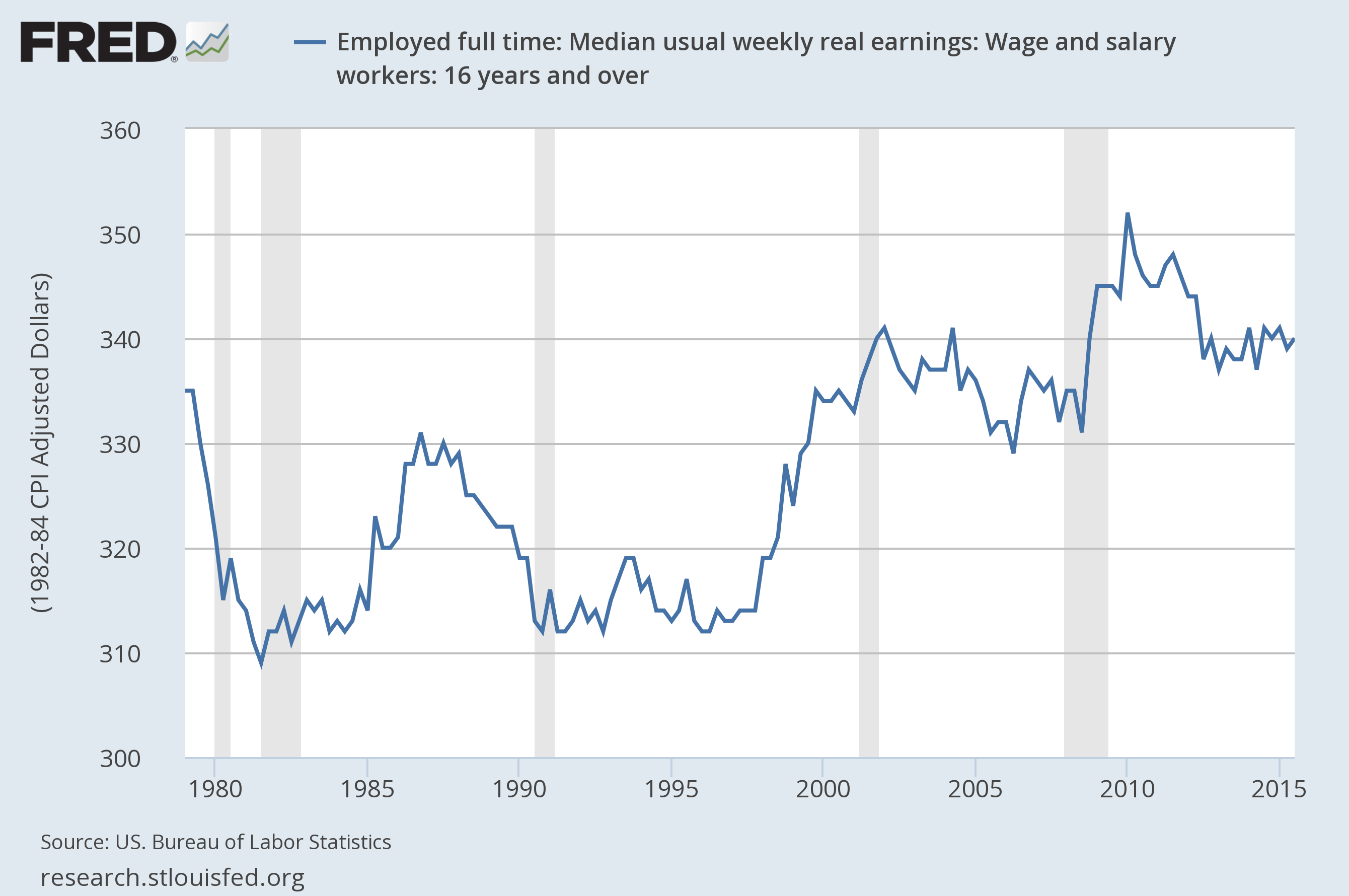

Furthermore, real median earnings for full-time employees have not meaningfully increased over the last 35 years; in 1982 dollars, they were $335 in 1979 and they are $340 now:

At first I thought this was because people were working more hours, but that doesn’t seem to be true; average weekly hours of work have fallen from 38.2 to 33.6:

The main reason seems to be actually that women are entering the workforce, so more households have multiple full-time incomes; while only 43% of women were in the labor force in 1970, almost 57% are now.

I must confess to a certain confusion on this point, however, as the difference doesn’t seem to be reflected in any of the measures of personal income. Median personal income was about 41% of median family income in 1974, and now it’s about 43%. I’m not sure exactly what’s going on here.

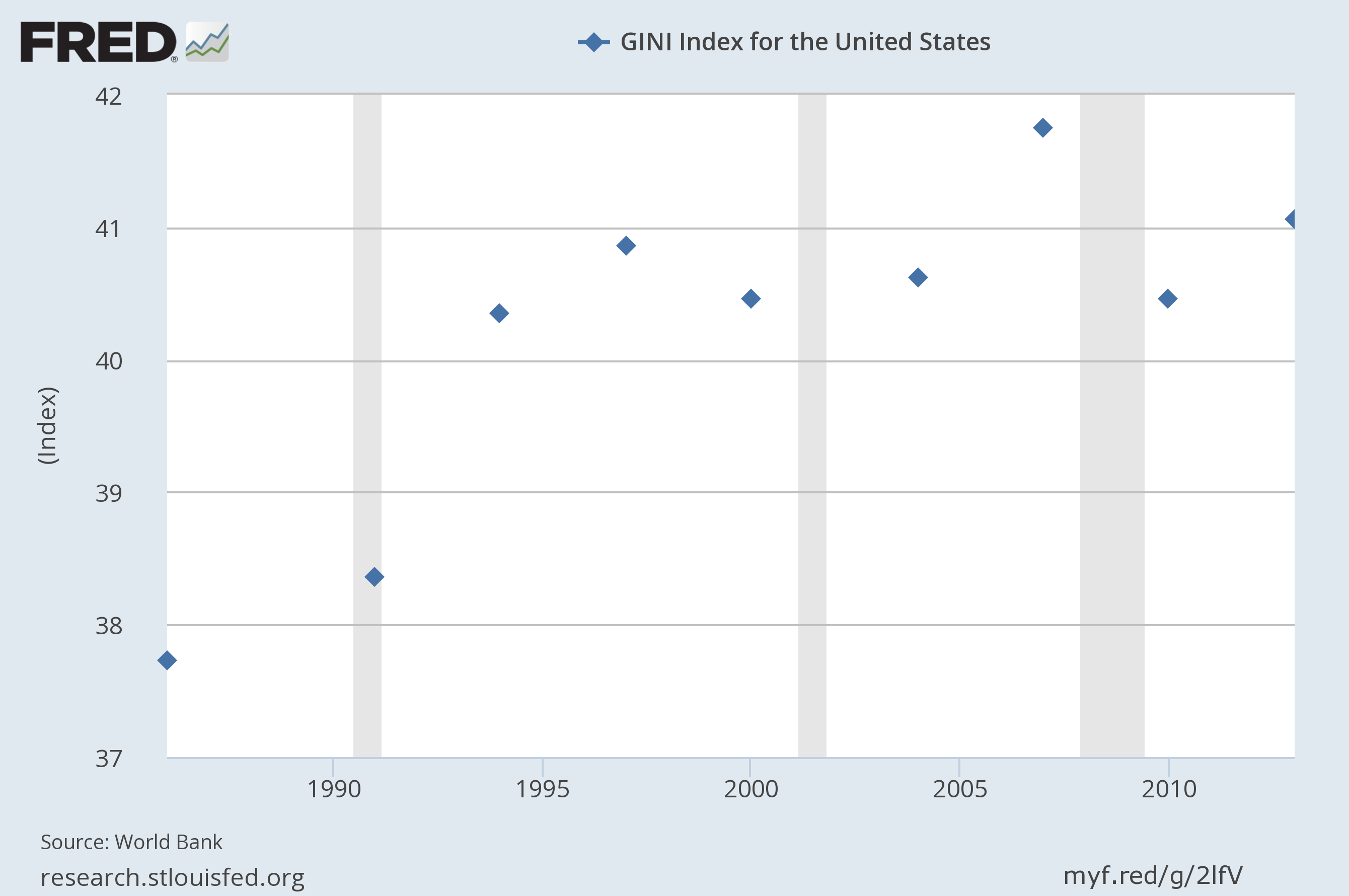

The Gini index, a standard measure of income inequality, is only collected every few years, yet shows a clear rising trend from 37% in 1986 to 41% in 2013:

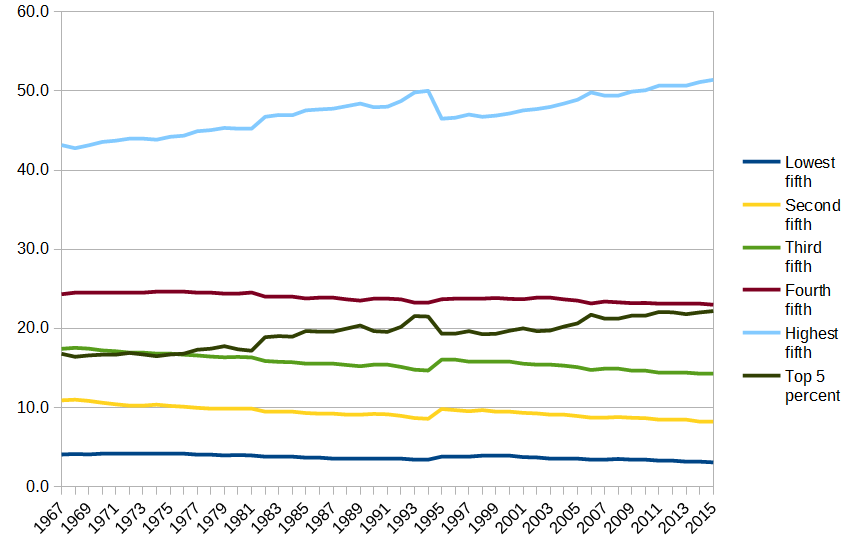

But perhaps the best way to really grasp our rising inequality is to look at the actual proportions of income received by each portion of the population.

This is what it looks like if you use US Census data, broken down by groups of 20% and the top 5%; notice how since 1977 the top 5% have taken in more than the 40%-60% bracket, and they are poised to soon take in more than the 60%-80% bracket as well:

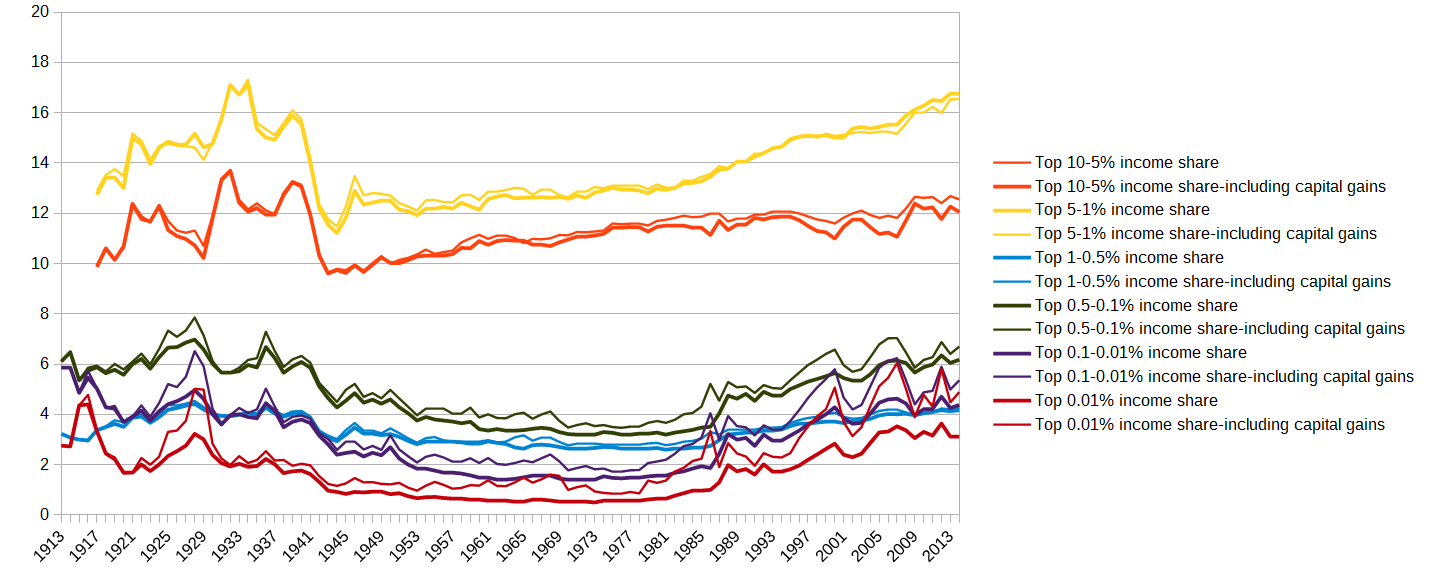

The result is even more striking if you use the World Top Incomes Database. You can watch the share of income rise for the top 10%, 5%, 1%, 0.1%, and 0.01%:

But in fact it’s even worse than it sounds. What I’ve just drawn double-counts a lot of things; it includes the top 0.01% in the top 0.1%, which is in turn included in the top 1%, and so on. If you exclude these, so that we’re only looking at the people in the top 10% but not the top 5%, the people in the top 5% but not the top 1%, and so on, something even more disturbing happens:

While the top 10% does see some gains, the top 5% gains faster, and the gains accrue even faster as you go up the chain.

Since 1970, the top 10%-5% share grew 10%. The top 0.01% share grew 389%.

Year

Top 10-5% share

Top 10-5% share incl. cap. gains

Top 5-1% share

Top 5-1% share incl cap. gains

Top 1-0.5% share

Top 1-0.5% share incl. cap. gains

Top 0.5-0.1% share

Top 0.5-0.1% share incl. cap. gains

Top 0.1-0.01% share

Top 0.1-0.01% share incl. cap. gains

Top 0.01% share

Top 0.01% share incl. cap. gains

1970

11.13

10.96

12.58

12.64

2.65

2.77

3.22

3.48

1.41

1.78

0.53

1

2014

12.56

12.06

16.78

16.55

4.17

4.28

6.18

6.7

4.38

5.36

3.12

4.89

Relative gain

12.8%

10.0%

33.4%

30.9%

57.4%

54.5%

91.9%

92.5%

210.6%

201.1%

488.7%

389.0%

To be clear, these are relative gains in shares. Including capital gains, the share of income received by the top 10%-5% grew from 10.96% to 12.06%, a moderate increase. The share of income received by the top 0.01% grew from 1.00% to 4.89%, a huge increase. (Yes, the top 0.01% now receive almost 5% of the income, making them on average almost 500 times richer than the rest of us.)

The pie has been getting bigger, which is a good thing. But the rich are getting an ever-larger piece of that pie, and the piece the very rich get is expanding at an alarming rate.

It’s certainly a reasonable question what is causing this rise in inequality, and what can or should be done about it. By people like the AEI try to pretend it doesn’t even exist, and that’s not economic policy analysis; that’s just plain denial.

You’ll notice it’s Sunday, not Saturday; I apologize for not actually posting on time this week. Due to the holiday season I was whisked away to family activities in Cleveland, and could not find wifi that was both free and reliable.

But since it is the Christmas season—Christmas Day was last Thursday—the time during which most Americans spend more than we can probably afford buying gifts (the highest rate of consumer spending all year long, much of it on credit cards, a significant boost for the economy in these times of depression), I thought it would be worthwhile to talk about why gifts are so important to us.

As I’ve already mentioned a few posts ago, neoclassical economists are typically baffled by gift-giving, and several have written research papers and books about why Christmas gifts are economically inefficient and should be stopped. Oddly it never seems to occur to them that if this is true, then there is widespread irrational consumer behavior that has nothing to do with government intervention or perverse incentives—which already means neoclassical economic theory is in serious trouble. Nobody forces you to buy gifts, so if it’s such a bad idea but we do it anyway, we must not be rational agents.

But in fact it’s not such a bad idea, and it’s “inefficient” only in a very narrow-minded sense that takes no account of relationships or human emotions. Gifts only make us not “rational agents” in that we are not infinite identical psychopaths. There is in fact nothing irrational about gifts.

Gift-giving is a human universal; it has been with us far longer than money or markets or indeed civilization itself. Everyone from tribal hunter-gatherers to neoclassical economists gives gifts, and in fact most people who descend from populations that lived in higher latitudes (that is, “White people”, though perhaps in a later post I’ll explain why our “race” categories are genetically absurd) actually celebrate some sort of gift-giving ceremony around the time of the Winter Solstice. Many of our Christmas traditions actually come from the Germanic holiday Yule, which is why we say things like “Yuletide greetings” even though that has absolutely nothing to do with Jesus. We celebrate around the Solstice because it was such a momentous season for us, the darkest night of the year; as if the darkness and cold weren’t bad enough by themselves they are the harbinger of the dreaded winter that prevents our crops from growing and may not allow us all to survive. We reaffirm our family ties and promise to help each other through this dangerous time. Music, gifts, and feasting are simply the way that humans organize our celebrations—again this is universal.

What do gifts accomplish that a simple transfer of cash would not? I can think of three things:

Convey closeness: First of all there is of course the fact that by buying someone a gift at all, you are expressing the fact that you care about them and want to be close to them. But the choice of the gift also matters. Your closest friends always buy you the best gifts, because they know you the best. Thus the sort of gift you receive from someone is a measure of how well they know you. Many of us give each other lists of ideas to buy, but I always include more on the list than I expect to receive and encourage people to buy things that are not on the list that they think I might enjoy. A computer program can buy things off a list; the point is that we express our relationships by choosing things we know people want without them having to ask. We trust people to know us well enough to get it right most of the time; they’ll probably make mistakes (most people think they know others better than they actually do), but the mistakes are made up for by the successes. The disappointment in getting something you didn’t want isn’t even so much in the thing as it is in the fear that your loved ones don’t know you as well as you thought they did; this is why I consider it important to express—gently and tactfully of course—when you really don’t like a gift you received; you want them to know you better and do better next time, not keep giving you things you hate while you brood behind fake smiles. What you choose to buy conveys what you know and how you feel; this is why the best gift is one you love to have but didn’t ask for. That’s why I’m honestly more excited about my new travel pillow and copy of Randall Monroe’s What If? than I am about my new Bluetooth headset; of course the headset is more expensive and more useful, but I specifically asked for it. My sister and my mother knew me well enough that the book and the travel pillow I didn’t have to ask for.

Grant permission to indulge: This is particularly important in the United States, because our society has Puritanical roots that make us suspicious of any activity that isn’t directly linked to productive efficiency. Honestly when those economists criticize Christmas as “inefficient” they are not so much making a serious economic argument as they are expressing in terms familiar to them the centuries-old Puritanical norm. It is considered unseemly to buy things for yourself that are purely for fun, particularly if they are expensive. You are expected to buy only the minimum you need, because any more is greedy; the notion seems to be that there is only so much stuff to go around, and if you take more others will have less. (This could scarcely be further from the truth; your frivolous consumer purchases can save children from starvation by giving their parents jobs in factories.) Neoclassical economists often think they are immune to this sort of norm, but aside from their discomfort with Christmas, the sense of righteousness they often have around “raising the savings rate” says otherwise. The link from savings to investment is tenuous at best, but one thing saving definitely does do is prevent you from spending indulgently. But since buying things that make us happy is actually kind of the entire point of having an economy in the first place, it is necessary to find workarounds for this oppressive ethic. One solution is gifts; to give someoneelse an indulgent gift allows them to engage in indulgent activities, while preserving their own status as someone who wouldn’t normally waste money in that way, and since you are not the one indulging you can hardly be accused of frivolity either. This is also what gift cards accomplish; in economic terms gift cards seem weird, because they are at best as good as cash, and often far worse. But gift cards are typically for retail stores where it is hard to buy something that’s not indulgent, thus offering permission to indulge. This is why a gift card for GameStop or Dick’s Sporting Goods makes sense, but a gift card to Walmart or Kroger seems odd. This is also why receiving cash or an Amazon gift card doesn’t feel as good; since you can buy just about anything, the social norm toward spending responsibly returns. (Neverbuy anyone a VISA gift card; it’s basically the same as cash except you’re giving some of the money to VISA.)

Conveys your own status: By buying expensive things for other people, you raise your own reputation as an individual. This one is easy to become cynical about, so it’s important to be clear what it actually means. Conveying your own status doesn’t necessarily mean arrogantly domineering over other people. It certainly can mean that, which is why if your cousin has $20 million and buys everyone in the family a new car every year, you’d honestly not be that thrilled about it; yeah, it’s nice getting a new car, but your cousin is clearly showboating his superior wealth and trying to make everyone else look cheap and/or poor. But there is a way to elevate your own status without downgrading everyone else’s, and truly generous gifts are a way of doing that. If the things you buy are really things your loved ones truly need, then you express your generosity and love for them by buying more than you can easily afford. Philanthropy is also a means of conveying status, and again comes in both forms. When Carnegie built buildings and named them after himself, he was being arrogant and domineering. When Bill Gates established a foundation to combat malaria and poverty in Africa, he was being genuinely generous. This kind of status is always a bit paradoxical: The best way to earn a reputation as a good person is to honestly try to help people and have little concern for your own reputation; people who try too hard to improve their own reputations just end up seeming arrogant and narcissistic. In order to deserve status, it is necessary not to directly seekit. The clearest example here is Jonas Salk: He invented a vaccine that saved the lives of thousands of children, making him more deserving of a billion dollars than anyone else I can think of. And he had a chance at a billion dollars, but he specifically gave it up, because in order to get it he would have had to enforce a patent that would raise the price of the vaccine and allow children to needlessly suffer and die. It was the very character that made him deserve the wealth that caused him to refuse it. The only way to hit the target is to aim much higher.

If you really want to insist, yes, there’s also some sort of net transfer of wealth involved in gift-giving, because it is expected that the richer you are the more you’ll spend on gifts. But that’s a very small part; even in hunter-gather societies that have negligible levels of inequality human beings still give each other gifts. Gifts are a part of us; they are written in the language of life itself upon the ancient thread that binds us to our ancestors and makes us who we are—by which I mean, of course, DNA. We could probably no more stop giving gifts than we could stop feeling love.

On a personal note, I can now proudly report that I have successfully defended my thesis “Corruption, ‘the Inequality Trap’, and ‘the 1% of the 1%’ “, and I now have completed a master’s degree in economics. I’m back home in Michigan for the holidays (hence my use of Eastern Standard Time), and then, well… I’m not entirely sure. I have a gap of about six months before PhD programs start. I have a number of job applications out, but unless I get a really good offer (such as the position at the International Food Policy Research Institute in DC) I think I may just stay in Michigan for awhile and work on my own projects, particularly publishing two of my books (my nonfiction magnum opus, The Mathematics of Tears and Joy, and my first novel, First Contact) and making some progress on a couple of research papers—ideally publishing one of them as well. But the future for me right now is quite uncertain, and that is now my major source of stress. Ironically I’d probably be less stressed if I were working full-time, because I would have a clear direction and sense of purpose. If I could have any job in the world, it would be a hard choice between a professorship at UC Berkeley or a research position at the World Bank.

Which brings me to the topic of today’s post: The people who do my dream job have just released a report showing that they basically agree with me on how it should be done.

If you have some extra time, please take a look at the World Bank World Development Report. They put one out each year, and it provides a rigorous and thorough (236 pages) but quite readable summary of the most important issues in the world economy today. It’s not exactly light summer reading, but nor is it the usual morass of arcane jargon. If you like my blog, you can probably follow most of the World Development Report. If you don’t have time to read the whole thing, you can at least skim through all the sidebars and figures to get a general sense of what it’s all about. Much of the report is written in the form of personal vignettes that make the general principles more vivid; but these are not mere anecdotes, for the report rigorously cites an enormous volume of empirical research.

The title of the 2015 report? “Mind, Society, and Behavior”. In other words, cognitive economics. The world’s foremost international economic institution has just endorsed cognitive economics and rejected neoclassical economics, and their report on the subject provides a brilliant introduction to the subject replete with direct applications to international development.

For someone like me who lives and breathes cognitive economics, the report is pure joy. It’s all there, from anchoring heuristicto social proof, corruption to discrimination. The report is broadly divided into three parts.

Part 1 explains the theory and evidence of cognitive economics, subdivided into “thinking automatically” (heuristics), “thinking socially” (social cognition), and “thinking with mental models” (bounded rationality). (If I wrote it I’d also include sections on the tribal paradigm and narrative, but of course I’ll have to publish that stuff in the actual research literature first.) Anyway the report is so amazing as it is I really can’t complain. It includes some truly brilliant deorbits on neoclassical economics, such as this one from page 47: ” In other words, the canonical model of human behavior is not supported in any society that has been studied.”

Part 2 uses cognitive economic theory to analyze and improve policy. This is the core of the report, with chapters on poverty, childhood, finance, productivity, ethnography, health, and climate change. So many different policies are analyzed I’m not sure I can summarize them with any justice, but a few particularly stuck out: First, the high cognitive demands of poverty can basically explain the whole observed difference in IQ between rich and poor people—so contrary to the right-wing belief that people are poor because they are stupid, in fact people seem stupid because they are poor. Simplifying the procedures for participation in social welfare programs (which is desperately needed, I say with a stack of incomplete Medicaid paperwork on my table—even I find these packets confusing, and I have a master’s degree in economics) not only increases their uptake but also makes people more satisfied with them—and of course a basic income could simplify social welfare programs enormously. “Are you a US citizen? Is it the first of the month? Congratulations, here’s $670.” Another finding that I found particularly noteworthy is that productivity is in many cases enhanced by unconditional gifts more than it is by incentives that are conditional on behavior—which goes against the very core of neoclassical economic theory. (It also gives us yet another item on the enormous list of benefits of a basic income: Far from reducing work incentives by the income effect, an unconditional basic income, as a shared gift from your society, may well motivate you even more than the same payment as a wage.)

Part 3 is a particularly bold addition: It turns the tables and applies cognitive economics to economists themselves, showing that human irrationality is by no means limited to idiots or even to poor people (as the report discusses in chapter 4, there are certain biases that poor people exhibit more—but there are also some they exhibit less.); all human beings are limited by the same basic constraints, and economists are human beings. We like to think of ourselves as infallibly rational, but we are nothing of the sort. Even after years of studying cognitive economics I still sometimes catch myself making mistakes based on heuristics, particularly when I’m stressed or tired. As a long-term example, I have a number of vague notions of entrepreneurial projects I’d like to do, but none for which I have been able to muster the effort and confidence to actually seek loans or investors. Rationally, I should either commit or abandon them, yet cannot quite bring myself to do either. And then of course I’ve never met anyone who didn’t procrastinate to some extent, and actually those of us who are especially smart often seem especially prone—though we often adopt the strategy of “active procrastination”, in which you end up doing something else useful when procrastinating (my apartment becomes cleanest when I have an important project to work on), or purposefully choose to work under pressure because we are more effective that way.

And the World Bank pulled no punches here, showing experiments on World Bank economists clearly demonstrating confirmation bias, sunk-cost fallacy, and what the report calls “home team advantage”, more commonly called ingroup-outgroup bias—which is basically a form of the much more general principle that I call the tribal paradigm.

If there is one flaw in the report, it’s that it’s quite long and fairly exhausting to read, which means that many people won’t even try and many who do won’t make it all the way through. (The fact that it doesn’t seem to be available in hard copy makes it worse; it’s exhausting to read lengthy texts online.) We only have so much attention and processing power to devote to a task, after all—which is kind of the whole point, really.