I’m calling it now: We officially live in the dystopian cyberpunk future. We’re not headed that way; it’s not on the horizon. It is here, now. The United States is a cyberpunk dystopia, exactly as we were warned it would become. Maybe there is still hope for the rest of the world.

I haven’t been writing blog posts as often for the last few weeks, mainly because the future feels so bleak that I can no longer tell the difference between the reality of this cyberpunk dystopia and my own crushing depression. I don’t want to add any more bleakness to the world than it already has, and I don’t even know if anything I write (or anything I do) even really matters anymore. The Fourth of July this year doesn’t feel like a birthday; it feels like a funeral.

But I couldn’t let this one go, so here we are: This man now owns 1 TRILLION DOLLARS in assets.

I want you to understand just how insane an amount of money that is. I want you to understand that no just society could ever remotely allow something like this to happen as long as there is a single child unfed or unhoused. I want you to understand that the time to reverse course on our society’s inequality was five orders of magnitude ago.

How much is 1 trillion dollars?

If you made a comfortable salary of $110,000 per year (more than most American families make), and you saved it all, spending nothing (or, equivalently, spent only the interest on your savings), it would take you nine million years to save up $1 trillion. Humans have not existed for that long. Even australopithecines hadn’t evolved yet. Nine million years ago, our ancestors were chimpanzees.

If you made $1 per second—that’s $86,500, more than most individual Americans make in a year, every single day—and likewise only spent the interest, you’d take 31,000 years to save up $1 trillion—longer than human civilization has existed. You could have started saving when the Great Pyramid was a twinkle in its architect’s eye, and you’d only have saved up 15% of the total.

If he wanted to, Elon Musk could personally end world hunger. And don’t tell me he couldn’t really do that because his wealth is tied up in stocks: UNICEF happily accepts donations in stock.

(As I understand it, SEC rules prevent Musk from selling or giving away his shares for a year after the IPO, so he couldn’t technically give away a trillion dollars today. But he could do it a year from now—and how likely do you think it is that he will?)

Did he earn this wealth?

HE COULDN’T POSSIBLY HAVE.

That is my point. No human being, no matter how great their contribution to the world, could ever possibly have earned this much wealth—and Elon Musk isn’t even on my top-100 list of greatest contributions by human beings; mostly they’d be scientists and humanitarians, but even quite a few science fiction authors and comedians should be ranked well above Elon Musk. In fact, his net contribution to humanity is pretty clearly negative. He is not the worst human to have ever lived (there’s a lot of competition for that spot, unfortunately; Stalin, maybe? Or some ancient mass murderer most people haven’t heard of?), but he is on that list, actually—or did you forget about those millions of children he sentenced to death?

He does not work a million times harder than you. He is not a million times smarter than you. He has not contributed to the world a million times more than you have. But I’m willing to bet he has a million times as much wealth as you do—because if he doesn’t, you’d have to be a millionaire, and I doubt most of my readers are millionaires.

This is the world we live in now. The dystopia is here.

Why do I make less money than, say, Mr. Beast (who now has a game show, apparently)?

The proximal answer to this question is obvious: He has a lot more people viewing his content, so he can sell ads that make him enormous amounts of money.

But that still leaves a deeper, more ultimate question unanswered:

Why are so many people interested in that?

Mr. Beast’s first truly viral YouTube videos was literally just him counting, one by one, from 1 to 100,000. He edited the footage to speed it up slightly so that the 40-hour ordeal would fit within a 24-hour video.

This is something that literally anyone could do that literally no one benefits from.

I also can’t imagine it was particularly entertaining to watch! Like, maybe he made it a little more entertaining than you might at first imagine (I don’t know; I have no desire to watch the actual video), but I still can’t imagine it would rate among even the top 100 most interesting things to do with 24 hours—or even the top 100 most interesting things that I could do right now from the comfort of my own home.

Right now you might be thinking I’m bitter about this, but if I am bitter, it is at our economic system as a whole; I harbor no ill will toward Mr. Beast in particular, who is actually something of a philanthropist. What I really am is utterly confused.

I don’t understand why anyone—let alone millions of people—would choose to watch that video. (Though it’s a bit easier to understand if you recognize that most viewers surely did not watch the entire thing.) I don’t understand how a man can make a highly successful career doing stupid stunts on video.

And I’m also quite certain that if I, right now, tried to do some similarly stupid stunt and post it on YouTube, it would get maybe a few dozen hits and nothing more would come of it.

Maybe Mr. Beast has something I don’t: A charm, a charisma, a salesmanship. Maybe he is spectacularly persistent in a way that I really can’t be (one certainly must be that to count to 100,000!). He likely is utterly unfazed by rejection, while I am severely oversensitive to it. So I’m not making the claim that there is nothing about Mr. Beast’s individual characteristics or talents that contributed to his success.

But I think it’s pretty clear at this point that the most important reason for Mr. Beast’s success is in fact no reason at all; his video is just the one that happened to go viral at that particular moment, and he managed to leverage that publicity into making yet more viral videos until he could become a multi-millionaire for doing stupid stunts in front of a webcam.

He is what I propose we call a stochastic superstar.

His success is not driven by talent, or intellect, or expertise; it is driven by luck. A million others have tried to imitate his exact methods and failed, not because they were any worse at it—but because he did it first.

This phenomenon is not entirely new; it certainly can be traced back at least as far as any form of mass media; radio and TV stars were often famous for no other reason that they were famous.

But I think it’s pretty clear that the Internet, and social media in particular, have made it much easier to become a stochastic superstar. Arcane, mysterious algorithms promote some content over other content in ways that hardly anyone—or perhaps literally no one, if LLMs are now involved—fully understands, and thousands of people doing basically the same thing get zero compensation for it, while one becomes rich and famous for no apparent reason.

This is not a healthy way to run an economy.

Yes, it certainly results in creating a lot of content, some of which is genuinely valuable. (Mr. Beast would not be high on my list of that either.) The Internet is an unfathomably grand and diverse place, and if you know where to look you can learn about almost anything in the world; or, you know, you can be fed complete misinformation and come away with fundamental misconceptions. Or you can just watch cat videos, which I’ll admit add some joy to the world, but probably not nearly enough to justify the amount of effort and time spent creating and viewing them.

It’s bad enough that glorifying superstars glorifies risk; but at least superstar athletes are objectively in peak physical condition and are the best players at the games they play. (I still don’t really get why people invest so much in these games, but whatever.) But it isn’t even clear that viral YouTubers are producing the best video content; they are just somehow producing the most successful video content in a way that seems basically orthogonal to actual quality or value for society.

I think this should lead us to a very important question:

Are there other systems we could use to compensate people for content?

What if ad revenue was divided evenly between all contributors to a platform, rather than just those with the highest view rates? Or what if there was some benefit to getting higher views, but there was some sort of mechanism to reduce the income inequality generated this way, like paying higher rates for views when you have fewer total views (e.g. $0.01 per view for the first 1000, $0.009 for the next 10,000, $0.008 for the next 100,000, etc.)? (Are there perverse incentives here, too? Surely. But are they worse than what we have right now?)

What if we didn’t run ads at all, but instead people paid microtransactions to subscribe to content? Patreon already sort of does this (and my Patreon is also an utter failure), but I think the transactions still aren’t micro enough. I want people to pay $0.05 to read an article—because that’s all the ad revenue they would give by reading that article anyway. Nobody should have to pay $5 to read what advertisers only pay $0.05 for. I want you to be able to see the title of a blog post and a brief snippet, and think, “Sure, I’ll pay a nickel to read that.” I don’t want you to have to decide whether you’re willing to commit to subscribing for an entire month for $5.

I would like to believe, at least, that people would be more willing to pay $0.05 to read good journalism and serious intellectual content, rather than a random guy counting to 100,000 for no reason. But even if that’s not true, at least we wouldn’t be so constantly inundated by ads!

Or what if social media platforms were maintained as public infrastructure, not yielding profits to any corporation, and instead of running ads, their hosting costs (which really are not all that high; I pay for my own hosting on this blog, for instance) were covered by tax revenue? Or what if you simply paid a subscription to use the social media site, and it was no longer used to harvest your data and target ads to you?

With an alternative system like one of the above, stochastic superstars would still be able to get famous randomly, and there are benefits (and drawbacks) that come directly from being famous; but maybe at least there would be fewer multi-millionaire YouTuber superstars and more ordinary people who are better able to make ends meet by contributing content.

But who am I kidding? This system works great for the billionaires who run it (who makes the real money off YouTube? Not Mr. Beast—Sundar Pichai.), and our government has shown very little interest in doing anything that would reduce their wealth and power. So, we can expect this, and everything else, to continue to get worse in exactly the way that cyberpunk fiction explicitly warned us it would, and our government continuing to do absolutely nothing about it!

In my previous post I reflected on the ways that conventional measures of poverty seem inadequate—and that a richer understanding of poverty suggests that it is far more ubiquitous than such measures suggest.

In this post, I will ask: Given this richer understanding of poverty, what would a world without poverty look like? Is it something we can realistically hope to achieve?

In techno-utopian circles (looking at you again, Scott Alexander), it is common to speak of “post-scarcity”: A world where there is no poverty because resources are effectively unlimited.

I don’t think that’s possible.

Not for humans as we know them. Perhaps in a future where greed is a recognized and treatable psychiatric disorder, we could genuinely have an economy where people really just take whatever they want and it works out because nobody wants an unreasonable amount.

But the fact that there are people with hundreds of billions of dollars tells me that among humans as we know them, some people’s greed is just literally insatiable. Give them a moon and they’ll demand a planet; give them a planet and they’ll demand a solar system. Whatever they are getting out of more wealth (status? power? the dopamine hit of number go up?), they’re never going to stop getting it from even more wealth, no matter how much we give them. For if they were going to stop at a reasonable amount, they would have stopped four orders of magnitude ago.

So let’s try to imagine what a world would look like if it really had no poverty, but not by somehow producing such staggering amounts of wealth that everyone could literally take whatever they want.

I think the key is that it would require all basic material needs to be met.

Some of these needs can probably never be completely satisfied—there is an inherent tension between liberty and security which requires us to balance them against each other. A society with zero crime is a horrific totalitarian police state; a society with complete liberty is an equally horrific Hobbesian nightmare. But we have achieved, in most of the First World at least, a reasonable standard of security along with a great deal of liberty, and preserving that balance should be of a very high priority.

Even clean air and water would be difficult to satisfy perfectly: even if we pivot our whole economy to solar, wind, and nuclear power (as we very definitely should be doing!), some amount of pollution is probably necessary just to have a functioning industrial society. So we need to establish reasonable standards for what amounts of pollution exposure are safe, and effective mechanisms for ensuring that people are not exposed to pollution outside those standards—we have largely done the former, but seriously fail at the latter.

But probably the most difficult needs to satisfy are actually difficult to even define.

Just what constitutes a basic standard of education, and a basic standard of healthcare?

These seem like moving targets.

Let’s start with education:

Someone who is illiterate and can barely add two numbers together would be considered to have very poor education today, but would be considered completely average among peasants in the Middle Ages. Someone like me with a PhD has education well beyond what anyone had in the Middle Ages: While Oxford was already graduating doctors in the 12th century, those doctors didn’t have to write dissertations, and didn’t know nearly as much about the world as you must to earn a modern PhD. (Most of the mathematics required to get an economics PhD specifically literally had not been invented.)

So it’s conceivable that educational standards will continue to rise over time, especially if we are able to radically improve learning via new technologies. In the most extreme case, if everyone can just download knowledge like in The Matrix, then it wouldn’t be unreasonable to expect the average person to know as much as a typical PhD today in dozens of fields.

Suppose that such technology did exist. Would it be fair to consider someone poor if they didn’t have access to it?

Yes, I think it would.

Because if it’s really cheap and easy to give breathtakingly vast knowledge on a variety of subjects to anyone instantly, then letting some people have that while others do not puts those others at a severe disadvantage in life. If you must know how to solve partial differential equations to get a job, then someone who only made it through high school algebra isn’t going to be able to find jobs.

So I think what we’re really concerned about here is inequality: The education of a rich person should not be too much better than the education of a poor person, lest “meritocracy” simply reinforce the same generational inequality it was supposed to eliminate.

Now consider healthcare:

This, too, has radically improved over time. Indeed, I’m not really sure it’s fair to call Medieval doctors doctors at all; they lacked basic knowledge of human physiology and their intervention was as likely to hurt patients as to help them. Surgeons certainly existed: They knew how to amputate a gangrenous limb or suture a wound. (They did so without antiseptic, let alone anaesthetic!) But should you come to them with a fever or a headache, they would likely do you as much harm as good.

So we could imagine a world of Star Trek medicine, where you lie in a bed, get scanned for a few moments, and the doctor immediately knows what’s wrong with you and what kind of painless injection to give you to fix it.

Once again, we must ask: If you don’t have that, are you poor?

And again, I’m going to say yes.

If the technology exists to heal people this effortlessly, and some people get access to it while others do not, the latter are being allowed to suffer when their suffering could be easily alleviated.

But now we must consider: what if the technology exists, but it’s too expensive to use routinely?

Most technologies are like this when they are first invented. Over time, the technology improves (and the patents expire!) and they become cheaper and more widely available.

Unlike education, healthcare doesn’t usually impose large advantages on those who receive it—though it can, especially in a society where disabilities are not adequately accommodated.

So I think I’m prepared to allow “early adopters” of new medical technology, people who are rich enough to pay for advanced treatments before they are available to everyone—within certain limits. If some new treatment grants radically higher productivity or lifespan, then in fact I think we have a moral obligation to wait until it can be universally shared before we give it to anyone—precisely because of the risk of reinforcing generational inequality.

Once again, in our effort to define poverty, we end up returning to inequality: The rich should not be allowed to be too much healthier than the poor.

This definitely makes education and healthcare more complicated than the others.

While we can pretty clearly define how much food and water a human being needs to live, and we could provide it to everyone, and then nobody would be poor in terms of food or water.

But making nobody poor in terms of education and healthcare requires meeting a standard that may in fact increase over time, and it is no contradiction to imagine that someone living in the 31st century could be receiving better healthcare than I ever will and yet is still not receiving adequate healthcare based on the technology available.

Furthermore, that person demanding better healthcare is not being ungrateful or envious—they are quite reasonably demanding that society fairly allocate healthcare so that there aren’t some people who live in eternal youth while other people still die of old age.

Are they richer than I am? In some sense, perhaps. We could stipulate that in every material way they are better off than I am now. But there’s a treatment that could extend their life by centuries, and nobody’s giving it to them, because they can’t afford it—and that’s wrong. That makes them poor, and it makes their society unfair and unjust. It isn’t just a question of how many QALY they have; it’s also a question of what it would cost to give them a lot more.

But with all that said, I do believe that a world without poverty is possible.

In fact, I believe that technologically we could already provide that world, if we had the political will to do so. Maybe we don’t quite have the economic output to support it worldwide, but even that is not as far off as most people seem to think.

Providing an adequate standard of food and water, for example, we could already do with existing food supplies. It would cost about one-eighth of Elon Musk’s wealth per year, meaning that, with good stock returns (as hemost certainly gets), he could very likely afford it by himself!

Clean air for all would be harder, but we are moving the right direction now that solar power is so cheap.

Universal liberty and security would require radical shifts in government in dozens of countries, so that one seems especially unlikely to happen any time soon—yet it is very definitely possible, and by construction only requires political change.

Universal education and healthcare would be very expensive, and most countries are too poor to really provide them on their own. They are not simply poor in money, but poor in skills: There aren’t enough doctors and teachers, and so we would need to use the ones we have to train up a new generation, and perhaps a new generation after that, before the world’s needs would really be met. (Fortunately, there are people trying to do this. But they don’t have enough resources to really achieve these goals.) So this is not a technological limitation, but it is an economic one; it will probably be at least another generation before we can solve this one.

What about universal shelter? Now there’s the rub. Even in prosperous First World countries, housing shortages and skyrocketing prices are keeping homeownership out of reach for tens of millions of people, and leaving hundreds of thousands outright homeless. We clearly do have the technology to produce enough homes, especially if we are prepared to build at high density; but the economic cost of doing so would be substantial, and our policymakers don’t seem at all willing to actually pay it. I think as long as housing is viewed as an asset one invests in rather than a good that one needs, this will continue to be the case.

The problem isn’t that we don’t have enough stuff. It’s that we are not sharing it properly.

What is poverty? It seems like a simple question, one we should all already know the answer to; but it turns out to be surprisingly complicated.

In practice, we mainly define some amount of income or consumption that is considered a “poverty line”, and declare that everyone below that line is in poverty, while everyone above it is not.

This post is about why that doesn’t work.

The most obvious question is of course: How do we draw that line? Some absolute level, or relative to income in the rest of society? Different places do it differently.

But I have come to realize that there is actually a deeper reason why there will never be a satisfying choice of “poverty line”:

There is no specific amount of income that could ever decide whether someone is in poverty.

It’s not a question of purchasing power. prices, or inflation. It’s not something you can adjust for statistically. It’s a fundamental error in defining the concept of poverty.

The problem is this:

Human needs are not fungible.

This Less Wrong post on “Anoxistan” really opened my eyes to that: No amount of money can make up for the fact that you’re missing something you need, be it a roof over your head, food on your table, clean water to drink, or medical care—or, as in the parable, air to breathe.

The best definition of poverty, then, is something like this:

Poverty is having to struggle to meet basic human material needs.

(I specify “material” needs, because someone who is alone and unloved has unmet human needs, but it is not the responsibility of even a utopian fully automated luxury communist society to provide for those needs. They may very well be miserable, but it does not make them poor.)

Maybe—maybe—in a well-functioning market economy, we can sort of muddle through by making a list of what everyone needs, finding the prices for all those goods and services, adding that up, and declaring that the poverty line. (This is often what we actually do, in fact.) The notion would then be that, as long as you have at least that amount of money, you can probably buy all the things you need.

But this rapidly breaks down if you aren’t facing the same prices as what were used to make that aggregation—which you almost never are, because nobody is the average American living in the average American city. And it also misses the fact that security is a human need, and simply having the necessary income for now is not at all the same thing as knowing that you’ll continue to have the necessary income in the future.

One Libertarian commentator asked me: “Would you really switch places with Rockefeller if you could?”

I had to think about it: I’d be losing a lot of things, for sure. No Internet, no cell phone, no computer, no video games. The quality of my clothes might actually be worse (though my wardrobe would surely be larger). Finding vegetarian food I enjoy might actually be more of a challenge, though I could surely import it from anywhere. Worst of all, I would lose access to many medical treatments I currently depend upon: Treatment of migraines in the late 19th century was considerably worse, and treatment of depression was essentially nonexistent.

Since this is about wealth, I think we can ignore the fact that I’d be moving into a terrifyingly racist, misogynistic and homophobic society. That itself might actually be the reason I wouldn’t really want to make the switch. But you can simultaneously believe that the late 19th century was a worse time than today for everyone who wasn’t a White cisgender heterosexual man, and also that Rockefeller was much richer than you’ll ever be.

But what would I gain? Power, though I have very little interest in that. Opportunities for philanthropy, which I do care about, but they’d benefit other people more than myself. Real estate—I don’t even own my own home, and Rockefeller owned multiple mansions, including, famously, the Casements in Florida.

But above all, I would gain security. Owning an oil company would allow me to live comfortably for the rest of my life, and most likely also allow my heirs to live comfortably for their entire lives, without me ever needing to work another day. I could still take jobs if I wanted them, but no employer would ever have any power over me. If I was unhappy at a job, I could just leave. If I wanted to spend a month, or a year, or a decade, without working at all, I could just do that. That is what it means to be rich. That is what Rockfeller had that I don’t think I will ever have.

The difference between being rich and being poor is security.

As long as anyone is struggling to make ends meet, poverty exists.

As long as anyone is afraid to lose their job, poverty exists.

As long as anyone is choosing not to have children because they don’t think they can afford them, poverty exists.

As long as bosses can abuse their employees and get away with it, poverty exists.

And in fact, it begins to look like poverty in the United States has not been decreasing over the last two generations, even as our per-capita GDP and median income have continued to rise and our population below “the poverty line” have fallen. (Indeed, that particular measure of “unable to afford children” has very clearly greatly increased, and is a very bad sign for our society’s future.)

This is how our economy is failing. It has given us lots more stuff, and made some things available to all that were once only available to the rich; but it has not freed us from the constant struggle to meet our basic needs, even though there are clearly plenty of resources available to do that.

This post is one I’ve been meaning to write for awhile, but current events keep taking precedence.

In 2023, Taylor Swift did something very interesting from an economic perspective, which turns out to have profound implications for our economic future.

She re-recorded an entire album and released it through a different record company.

The album was called 1989 (Taylor’s Version), and she created it because for the last four years she had been fighting with Big Machine Records over the rights to her previous work, including the original album 1989.

A Marxist might well say she seized the means of production! (How rich does she have to get before she becomes bourgeoisie, I wonder? Is she already there, even though she’s one of a handful of billionaires who can truly say they were self-made?)

But really she did something even more interesting than that. It was more like she said:

“Seize the means of production? I am the means of production.”

Singing and songwriting are what is known as a human-capital-intensive industry. That is, the most important factor of production is not land, or natural resources, or physical capital (yes, you need musical instruments, amplifiers, recording equipment and the like—but these are a small fraction of what it costs to get Talor Swift for a concert), or even labor in the ordinary sense. It’s one where so-called (honestly poorly named) “human capital” is the most important factor of production.

A labor-intensive industry is one where you just need a lot of work to be done, but you can get essentially anyone to do it: Cleaning floors is labor-intensive. A lot of construction work is labor-intensive (though excavators and the like also make it capital-intensive).

No, for a human-capital-intensive industry, what you need is expertise or talent. You don’t need a lot of people doing back-breaking work; you need a few people who are very good at doing the specific thing you need to get done.

Taylor Swift was able to re-record and re-release her songs because the one factor of production that couldn’t be easily substituted was herself. Big Machine Records overplayed their hand; they thought they could control her because they owned the rights to her recordings. But she didn’t need her recordings; she could just sing the songs again.

But now I’m sure you’re wondering: So what?

Well, Taylor Swift’s story is, in large part, the story of us all.

For most of the 18th, 19th, and 20th centuries, human beings in developed countries saw a rapid increase in their standard of living.

Yes, a lot of countries got left behind until quite recently.

Yes, this process seems to have stalled in the 21st century, with “real GDP” continuing to rise but inequality and cost of living rising fast enough that most people don’t feel any richer (and I’ll get to why that may be the case in a moment).

But for millions of people, the gains were real, and substantial. What was it that brought about this change?

The story we are usually told is that it was capital; that as industries transitioned from labor-intensive to capital-intensive, worker productivity greatly increased, and this allowed us to increase our standard of living.

That’s part of the story. But it can’t be the whole thing.

Why not, you ask?

Because very few people actually own the capital.

When capital ownership is so heavily concentrated, any increases in productivity due to capital-intensive production can simply be captured by the rich people who own the capital. Competition was supposed to fix this, compelling them to raise wages to match productivity, but we often haven’t actually had competitive markets; we’ve had oligopolies that consolidate market power in a handful of corporations. We had Standard Oil before, and we have Microsoft now. (Did you know that Microsoft not only owns more than half the consumer operating system industry, but after acquiring Activision Blizzard, is now the largest video game company in the world?) In the presence of an oligopoly, the owners of the capital will reap the gains from capital-intensive productivity.

But standards of living did rise. So what happened?

The answer is that production didn’t just become capital-intensive. It became human-capital-intensive.

More and more jobs required skills that an average person didn’t have. This created incentives for expanding public education, making workers not just more productive, but also more aware of how things work and in a stronger bargaining position.

Today, it’s very clear that the jobs which are most human-capital-intensive—like doctors, lawyers, researchers, and software developers—are the ones with the highest pay and the greatest social esteem. (I’m still not 100% sure why stock traders are so well-paid; it really isn’t that hard to be a stock trader. I could write you an algorithm in 50 lines of Python that would beat the average trader (mostly by buying ETFs). But they pretend to be human-capital-intensive by hiring Harvard grads, and they certainly pay as if they are.)

The most capital-intensive industries—like factory work—are reasonably well-paid, but not that well-paid, and actually seem to be rapidly disappearing as the capital simply replaces the workers. Factory worker productivity is now staggeringly high thanks to all this automation, but the workers themselves have gained only a small fraction of this increase in higher wages; by far the bigger effect has been increased profits for the capital owners and reduced employment in manufacturing.

And of course the real money is all in capital ownership. Elon Musk doesn’t have $400 billion because he’s a great engineer who works very hard. He has $400 billion because he owns a corporation that is extremely highly valued (indeed, clearly overvalued) in the stock market. Maybe being a great engineer or working very hard helped him get there, but it was neither necessary nor sufficient (and I’m sure that his dad’s emerald mine also helped).

Indeed, this is why I’m so worried about artificial intelligence.

Most forms of automation replace labor, in the conventional labor-intensive sense: Because you have factory robots, you need fewer factory workers; because you have mountaintop removal, you need fewer coal miners. It takes fewer people to do the same amount of work. But you still need people to plan and direct the process, and in fact those people need to be skilled experts in order to be effective—so there’s a complementarity between automation and human capital.

But AI doesn’t work like that. AI substitutes for human capital. It doesn’t just replace labor; it replaces expertise.

So far, AI is currently too unreliable to replace any but entry-level workers in human-capital-intensive industries (though there is some evidence it’s already doing that). But it will most likely get more reliable over time, if not via the current LLM paradigm, than through the next one that comes after. At some point, AI will come to replace experienced software developers, and then veteran doctors—and I don’t think we’ll be ready.

The long-term pattern here seems to be transitioning away from human-capital-intensive production to purely capital-intensive production. And if we don’t change the fact that capital ownership is heavily concentrated and so many of our markets are oligopolies—which we absolutely do not seem poised to do anything about; Democrats do next to nothing and Republicans actively and purposefully make it worse—then this transition will be a recipe for even more staggering inequality than before, where the rich will get even more spectacularly mind-bogglingly rich while the rest of us stagnate or even see our real standard of living fall.

The tech bros promise us that AI will bring about a utopian future, but that would only work if capital ownership were equally shared. If they continue to own all the AIs, they may get a utopia—but we sure won’t.

We can’t all be Taylor Swift. (And if AI music catches on, she may not be able to much longer either.)

A lot of people speak about student debt as a “crisis”, which makes it sound like the problem is urgent and will have severe consequences if we don’t soon intervene. I don’t think that’s right. While it’s miserable to be unable to pay your student loans, student loans don’t seem to be driving people to bankruptcy or homelessness the way that medical bills do.

Instead I think what we have here is a long-term problem, something that’s been building for a long time and will slowly but surely continue getting worse if we don’t change course. (I guess you can still call it a “crisis” if you want; climate change is also like this, and arguably a crisis.)

Making all this worse is the fact that some of the most important income-based repayment plans were overturned by a federal court, forcing everyone who was on them into forebearance. Income-based repayment was a big reason why student loans actually weren’t as bad a burden as their high loan balances might suggest; unlike a personal loan or a mortgage, if you didn’t have enough income to repay your student loans at the full amount, you could get on a plan that would let you make smaller payments, and if you paid on that plan for long enough—even if it didn’t add up to the full balance—your loans would be forgiven.

Now the forebearance is ending for a lot of borrowers, and so they are going into default; and most of that loan forgiveness has been ruled illegal. (Supposedly this is because Congress didn’t approve it. I’ll believe that was the reason when the courts overrule Trump’s tariffs, which clearly have just as thin a legal justification and will cause far more harm to us and the rest of the world.)

In theory, student loans don’t really seem like a bad idea.

Most people don’t have enough liquidity to pay for college.

So, we provide loans, so that people can pay for college, and then when they make more money after graduating, they can pay the loans back.

That’s the theory, anyway.

The problem is that average or even median salaries obscure a lot of variation. Some college graduates become doctors, lawyers, or stockbrokers and make huge salaries. Others can’t find jobs at all. In the absence of income-based repayment plans, all students have to pay back their loans in full, regardless of their actual income after graduation.

There is inherent risk in trying to build a career. Our loan system—especially with the recent changes—puts most of this risk on the student. We treat it as their fault they can’t get a good job, and then punish them with loans they can’t afford to repay.

In fact, right now the job market is pretty badfor recent graduates—while usually unemployment for recent college grads is lower than that of the general population, since about 2018 it has actually been higher. (It’s no longer sky-high like it was during COVID; 4.8% is not bad in the scheme of things.)

Actually the job market may even be worse than it looks, because new hires are actually the lowest rate they’ve been since 2020. Our relatively low unemployment currently seems to reflect a lack of layoffs, not a healthy churn of people entering and leaving jobs. People seem to be locked into their jobs, and if they do leave them, finding another is quite difficult.

What I think we need is a system that makes the government take on more of the risk, instead of the students.

There are lots of ways to do this. Actually, the income-based repayment systems we used to have weren’t too bad.

But there is actually a way to do it without student loans at all. College could be free, paid for by taxes.

Now, I know what you’re thinking: Isn’t this unfair to people who didn’t go to college? Why should they have to pay?

Who said they were paying?

There could simply be a portion of the income tax that you only pay if you have a bachelor’s degree. Then you would only pay this tax if you both graduated from college and make a lot of money.

I don’t think this would create a strong incentive not to get a bachelor’s degree; the benefits of doing so remain quite large, even if your taxes were a bit higher as a result.

It might create incentives to major in subjects that aren’t as closely linked to higher earnings—liberal arts instead of engineering, medicine, law, or business. But this I see as fundamentally a public good: The world needs people with liberal arts education. If the market fails to provide for them, the government should step in.

This plan is not as progressive as Elizabeth Warren’s proposal to use wealth taxes to fund free college; but it might be more politically feasible. The argument that people who didn’t go to college shouldn’t have to pay for people who did actually seems reasonable to me; but this system would ensure that in fact they don’t.

The transfer of wealth here would be from people who went to college and make a lot of money to people who went to college and don’t make a lot of money. It would be the government bearing some of the financial risk of taking on a career in an uncertain world.

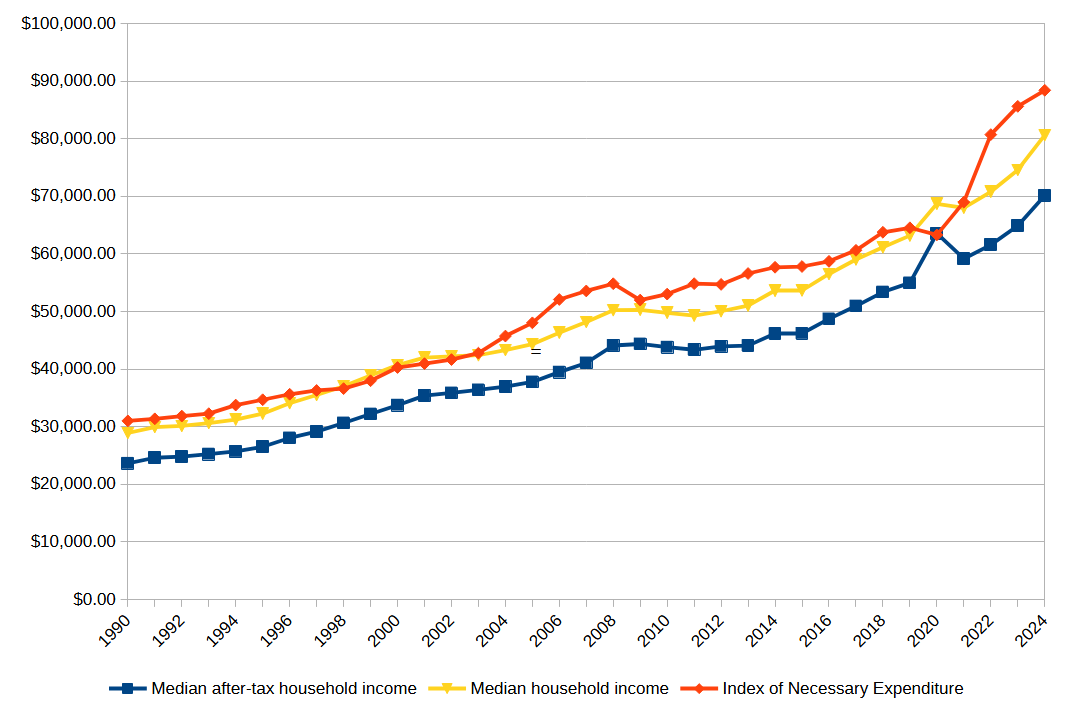

In last week’s post I constructed an Index of National Expenditure (INE), attempting to estimate the total cost of all of the things a family needs and can’t do without, like housing, food, clothing, cars, healthcare, and education. What I found shocked me: The median family cannot afford all necessary expenditures.

I have a couple more thoughts about that.

I still don’t understand why people care so much about gas prices.

Gasoline was a relatively small contribution to INE. It was more than clothing but less than utilities, and absolutely dwarfed by housing, food, or college. I thought maybe since I only counted a 15-mile commute, maybe I didn’t actually include enoughgasoline usage, but based on this estimate of about $2000 per driver, I was in about the right range; my estimate for the same year was $3350 for a 2-car family.

I think I still have to go with my salience hypothesis: Gasoline is the only price that we plaster in real-time on signs on the side of the road. So people are constantly aware of it, even though it isn’t actually that important.

The price surge that should be upsetting people is housing.

If the price of homes had only risen with the rate of CPI inflation instead of what it actually did, the median home price in 2024 would be only $234,000 instead of the $396,000 it actually is; and by my estimation that would save a typical family $11,000 per year—a whopping 15% of their income, and nearly enough to make the INE affordable by itself.

Now, I’ll consider some possible objections to my findings.

Objection 1: A typical family doesn’t actually spend this much on these things.

You’re right, they don’t! Because they couldn’t possibly. Even with substantial debt, you just can’t sustainably spend 125% of your after-tax household income.

My goal here was not to estimate how much families actually spend; it was to estimate how much they need to spend in order to live a good life and not feel deprived.

What I have found is that most American families feel deprived. They are forced to sacrifice something really important—like healthcare, or education, or owning a home—because they simply can’t afford it.

What I’m trying to do here is find the price of the American Dream; and what I’ve found is that the American Dream has a price that most Americans cannot afford.

Objection 2: You should use median healthcare spending, not mean.

I did in fact use mean figures instead of median for healthcare expenditures, mainly because only the mean was readily available. Mean income is higher than median income, so you might say that I’ve overestimated healthcare expenditure—and in a sense that’s definitely true. The median family spends less than this on healthcare.

But the reason that the median family spends less than this on healthcare is not that they want to, but that they have to. Healthcare isn’t a luxury that people buy more of because they are richer. People buy either as much as they need or as much as they can afford—whichever is lower, which is typically the latter. Using the mean instead of the median is a crude way to account for that, but I think it’s a defensible one.

But okay, let’s go ahead and cut the estimate of healthcare spending in half; even if you do that, the INE is still larger than after-tax median household income in most years.

Objection 3: A typical family isn’t a family of four, it’s a family of three.

Part of what I seem to be finding here is that a family of four is unaffordable—literally impossible to afford—on a typical family income.

But a healthy society is one in which typical families have two or three children. That is what we need in order to achieve population replacement. When families get smaller than that, we aren’t having enough children, and our population will decline—which means that we’ll have too many old people relative to young people. This puts enormous pressure on healthcare and pension systems, which rely upon the fact that young people produce more, in order to pay for the fact that old people cost more.

This is bad. This is not sustainable. If the reason families aren’t having enough kids is that they can’t afford them—and this fits with other research on the subject—then this economic failure damages our entire society, and it needs to be fixed.

Objection 4: Many families buy their cars used.

Perhaps 1/10 of a new car every year isn’t an ideal estimate of how much people spend on their cars, but if anything I think it’s conservative, because if you only buy a car every 10 years, and it was already used when you bought it, you’re going to need to spend a lot on maintaining it—quite possibly more than it would cost to get a new one. Motley Fool actually estimates the ownership cost of just one car at substantially more than I estimated for two cars. So if anything your complaint should be that I’ve underestimated the cost by not adequately including maintenance and insurance.

Objection 5: Not everyone gets a four-year college degree.

Fair enough; a substantial proportion get associate’s degrees, and most people get no college degree at all. But some also get graduate degrees, which is even more expensive (ask me how I know).

Moreover, in today’s labor market, having a college degree makes a huge difference in your future earnings; a bachelor’s degree increases your lifetime earnings by a whopping 84%. In theory it’s okay to have a society where most people don’t go to college; in practice, in our society, not going to college puts you at a tremendous disadvantage for the rest of your life. So we either need to find a way to bring wages up for those who don’t go to college, or find a way to bring the cost of college down.

This is probably one of the things that families actually choose to scrimp on, only sending one kid to college or none at all. But because college is such a huge determinant of earnings, this perpetuates intergenerational inequality: Only rich families can afford to send their kids to college, and only kids who went to college grow up to have rich families.

Objection 6: You don’t actually need to save for college; you can use student loans.

Yes, you can, and in practice, most people who to college do. But while this solves the liquidity problem (having enough money right now), it does not solve the solvency problem (having enough money in the long run). Failing to save for college and relying on student loans just means pushing the cost of college onto your children—and since we’ve been doing that for over a generation, feel free to replace the category “college savings” with “repaying student loans”; it won’t meaningfully change the results.

I’m still reeling from the fact that Donald Trump was re-elected President. He seemed obviously horrible at the time, and he still seems horrible now, for many of the same reasons as before (we all knew the tariffs were coming, and I think deep down we knew he would sell out Ukraine because he loves Putin), as well as some brand new ones (I did not predict DOGE would gain access to all the government payment systems, nor that Trump would want to start a “crypto fund”). Kamala Harris was not an ideal candidate, but she was a good candidate, and the comparison between the two could not have been starker.

Now that the dust has cleared and we have good data on voting patterns, I am now less convinced than I was that racism and sexism were decisive against Harris. I think they probably hurt her some, but given that she actually lost the most ground among men of color, racism seems like it really couldn’t have been a big factor. Sexism seems more likely to be a significant factor, but the fact that Harris greatly underperformed Hillary Clinton among Latina women at least complicates that view.

A lot of voters insisted that they voted on “inflation” or “the economy”. Setting aside for a moment how absurd it was—even at the time—to think that Trump (he of the tariffs and mass deportations!) was going to do anything beneficial for the economy, I would like to better understand how people could be so insistent that the economy was bad even though standard statistical measures said it was doing fine.

Krugman believes it was a “vibecession”, where people thought the economy was bad even though it wasn’t. I think there may be some truth to this.

But today I’d like to evaluate another possibility, that what people were really reacting against was not inflation per se but necessitization.

I first wrote about necessitization in 2020; as far as I know, the term is my own coinage. The basic notion is that while prices overall may not have risen all that much, prices of necessities have risen much faster, and the result is that people feel squeezed by the economy even as CPI growth remains low.

In this post I’d like to more directly evaluate that notion, by constructing an index of necessary expenditure (INE).

The core idea here is this:

What would you continue to buy, in roughly the same amounts, even if it doubled in price, because you simply can’t do without it?

For example, this is clearly true of housing: You can rent or you can own, but can’t not have a house. And nor are most families going to buy multiple houses—and they can’t buy partial houses.

It’s also true of healthcare: You need whatever healthcare you need. Yes, depending on your conditions, you maybe could go without, but not without suffering, potentially greatly. Nor are you going to go out and buy a bunch of extra healthcare just because it’s cheap. You need what you need.

I think it’s largely true of education as well: You want your kids to go to college. If college gets more expensive, you might—of necessity—send them to a worse school or not allow them to complete their degree, but this would feel like a great hardship for your family. And in today’s economy you can’t not send your kids to college.

But this is not true of technology: While there is a case to be made that in today’s society you need a laptop in the house, the fact is that people didn’t used to have those not that long ago, and if they suddenly got a lot cheaper you very well might buy another one.

Well, it just so happens that housing, healthcare, and education have all gotten radically more expensive over time, while technology has gotten radically cheaper. So prima facie, this is looking pretty plausible.

But I wanted to get more precise about it. So here is the index I have constructed. I consider a family of four, two adults, two kids, making the median household income.

To get the median income, I’ll use this FRED series for median household income, then use this table of median federal tax burden to get an after-tax wage. (State taxes vary too much for me to usefully include them.) Since the tax table ends in 2020 which was anomalous, I’m going to extrapolate that 2021-2024 should be about the same as 2019.

I assume the kids go to public school, but the parents are saving up for college; to make the math simple, I’ll assume the family is saving enough for each kid to graduate from with a four-year degree from a public university, and that saving is spread over 16 years of the child’s life. 2*4/16 = 0.5; this means that each year the family needs to come up with 0.5 years of cost of attendance. (I had to get the last few years from here, but the numbers are comparable.)

I assume the family owns two cars—both working full time, they kinda have to—which I amortize over 10 year lifetimes; 2*1/10 = 0.2, so each year the family pays 0.2 times the value of an average midsize car. (The current average new car price is $33226; I then use the CPI for cars to figure out what it was in previous years.)

I assume they pay a 30-year mortgage on the median home; they would pay interest on this mortgage, so I need to factor that in. I’ll assume they pay the average mortgage rate in that year, but I don’t want to have to do a full mortgage calculation (including PMI, points, down payment etc.) for each year, so I’ll say that they amount they pay is (1/30 + 0.5 (interest rate))*(home value) per year, which seems to be a reasonable approximation over the relevant range.

I assume that both adults have a 15-mile commute (this seems roughly commensurate with the current mean commute time of 26 minutes), both adults work 5 days per week, 50 weeks per year, and their cars get the median level of gas mileage. This means that they consume 2*15*2*5*50/(median MPG) = 15000/(median MPG) gallons of gasoline per year. I’ll use this BTS data for gas mileage. I’m intentionally not using median gasoline consumption, because when gas is cheap, people might take more road trips, which is consumption that could be avoided without great hardship when gas gets expensive. I will also assume that the kids take the bus to school, so that doesn’t contribute to the gasoline cost.

That I will multiply by the average price of gasoline in June of that year, which I have from the EIA since 1993. (I’ll extrapolate 1990-1992 as the same as 1993, which is conservative.)

I will assume that the family owns 2 cell phones, 1 computer, and 1 television. This is tricky, because the quality of these tech items has dramatically increased over time.

If you try to measure with equivalent buying power (e.g. a 1 MHz computer, a 20-inch CRT TV), then you’ll find that these items have gotten radically cheaper; $1000 in 1950 would only buy as much TV as $7 today, and a $50 Raspberry Pi‘s 2.4 GHz processor is 150 times faster than the 16 MHz offered by an Apple Powerbook in 1991—despite the latter selling for $2500 nominally. So in dollars per gigahertz, the price of computers has fallen by an astonishing 7,500 times just since 1990.

But I think that’s an unrealistic comparison. The standards for what was considered necessary have also increased over time. I actually think it’s quite fair to assume that people have spent a roughly constant nominal amount on these items: about $500 for a TV, $1000 for a computer, and $500 for a cell phone. I’ll also assume that the TV and phones are good for 5 years while the computer is good for 2 years, which makes the total annual expenditure for 2 phones, a TV, and a computer equal to 2/5*500 + 1/5*500 + 1/2*1000 = 800. This is about what a family must spend every year to feel like they have an adequate amount of digital technology.

I will assume that the family buys the equivalent of five months of infant care per year; they surely spend more than this (in either time or money) when they have actual infants, but less as the kids grow. This amounts to about $5000 today, but was only $1600 in 1990—a 214% increase, or 3.42% per year.

For food expenditure, I’m going to use the USDA’s thrifty plan for June of that year. I’ll use the figures assuming that one child is 6 and the other is 9. I don’t have data before 1994, so I’ll extrapolate that with the average growth rate of 3.2%.

The figures I had the hardest time getting were for utilities. It’s also difficult to know what to include: Is Internet access a necessity? Probably, nowadays—but not in 1990. Should I separate electric and natural gas, even though they are partial substitutes? But using these figures I estimate that utility costs rise at about 0.8% per year in CPI-adjusted terms, so what I’ll do is benchmark to $3800 in 2016 and assume that utility costs have risen by (0.8% + inflation rate) per year each year.

Healthcare is also a tough one; pardon the heteronormativity, but for simplicity I’m going to use the mean personal healthcare expenditures for one man and woman (aged 19-44) and one boy and one girl (aged 0-18). Unfortunately I was only able to find that for two-year intervals in the range from 2002 to 2020, so I interpolated and extrapolated both directions assuming the same average growth rate of 3.5%.

So let’s summarize what all is included here:

Estimated payment on a mortgage

0.5 years of college tuition

amortized cost of 2 cars

7500/(median MPG) gallons of gasoline

amortized cost of 2 phones, 1 computer, and 1 television

average spending on clothes

11% of income on food

Estimated utilities spending

Estimated childcare equivalent to five months of infant care

Healthcare for one man, one woman, one boy, one girl

There are obviously many criticisms you could make of these choices. If I were writing a proper paper, I would search harder for better data and run robustness checks over the various estimation and extrapolation assumptions. But for these purposes I really just want a ballpark figure, something that will give me a sense of what rising cost of living feels like to most people.

What I found absolutely floored me. Over the range from 1990 to 2024:

The Index of Necessary Expenditure rose by an average of 3.45% per year, almost a full percentage point higher than the average CPI inflation of 2.62% per year.

Over the same period, after-tax income rose at a rate of 3.31%, faster than CPI inflation, but slightly slower than the growth rate of INE.

The Index of Necessary Expenditure was over 100% of median after-tax household income every year except 2020.

Since 2021, the Index of Necessary Expenditure has risen at an average rate of 5.74%, compared to CPI inflation of only 2.66%. In that same time, after-tax income has only grown at a rate of 4.94%.

Point 3 is the one that really stunned me. The only time in the last 34 years that a family of four has been able to actually pay for all necessities—just necessities—on a typical household income was during the COVID pandemic, and that in turn was only because the federal tax burden had been radically reduced in response to the crisis. This means that every single year, a typical American family has been either going further and further into debt, or scrimping on something really important—like healthcare or education.

No wonder people feel like the economy is failing them! It is!

In fact, I can even make sense now of how Trump could convince people with “Are you better off than you were four years ago?” in 2024 looking back at 2020—while the pandemic was horrific and the disruption to the economy was massive, thanks to the US government finally actually being generous to its citizens for once, people could just about actually make ends meet. That one year. In my entire life.

This is why people felt betrayed by Biden’s economy. For the first time most of us could remember, we actually had this brief moment when we could pay for everything we needed and still have money left over. And then, when things went back to “normal”, it was taken away from us. We were back to no longer making ends meet.

When I went into this, I expected to see that the INE had risen faster than both inflation and income, which was indeed the case. But I expected to find that INE was a large but manageable proportion of household income—maybe 70% or 80%—and slowly growing. Instead, I found that INE was greater than 100% of income in every year but one.

And the truth is, I’m not sure I’ve adequately covered all necessary spending! My figures for childcare and utilities are the most uncertain; those could easily go up or down by quite a bit. But even if I exclude them completely, the reduced INE is still greater than income in most years.

Suddenly the way people feel about the economy makes a lot more sense to me.

What do the police do? Not in theory, in practice. Not what are they supposed to do—what do they actually do?

Ask someone right-wing and they’ll say something like “uphold the law”. Ask someone left-wing and they’ll say something like “protect the interests of the rich”. Both of these are clearly inaccurate. They don’t fit the pattern of how the police actually behave.

What is that pattern? Well, let’s consider some examples.

If you rob a bank, the police will definitely arrest you. That would be consistent with either upholding the law or protecting the interests of the rich, so it’s not a very useful example.

If you run a business with unsafe, illegal working conditions, and someone tells the police about it, the police will basically ignore it and do nothing. At best they might forward it to some regulatory agency who might at some point get around to issuing a fine.

If you strike against your unsafe working conditions and someone calls the police to break up your picket line, they’ll immediately come in force and break up your picket line.

So that definitively refutes the “uphold the law” theory; by ignoring OSHA violations and breaking up legal strikes, the police are actively making it harder to enforce the law. It seems to fit the “protect the interests of the rich” theory. Let’s try some other examples.

If you run a fraudulent business that cons people out of millions of dollars, the police might arrest you, eventually, if they ever actually bother to get around to investigating the fraud. That certainly doesn’t look like upholding the law—but you can get very rich and they’ll still arrest you, as Bernie Madoff discovered. So being rich doesn’t grant absolute immunity from the police.

If your negligence in managing the safety systems of your factory or oil rig kills a dozen people, the police will do absolutely nothing. Some regulatory agency may eventually get around to issuing you a fine. That also looks like protecting the interests of the rich. So far the left-wing theory is holding up.

If you are homeless and camping out on city property, the police will often come to remove you. Sometimes there’s a law against such camping, but there isn’t always; and even when there is, the level of force used often seems wildly disproportionate to the infraction. This also seems to support the left-wing account.

But now suppose you go out and murder several homeless people. That is, if anything, advancing the interests of the rich; it’s certainly not harming them. Yet the police would in fact investigate. It might be low on their priorities, especially if they have a lot of other homicides; but they would, in fact, investigate it and ultimately arrest you. That doesn’t look like advancing the interests of the rich. It looks a lot more like upholding the law, in fact.

Or suppose you are the CEO of a fraudulent company that is about to be revealed and thus collapse, and instead of accepting the outcome or absconding to the Carribbean (as any sane rich psychopath would), you decide to take some SEC officials hostage and demand that they certify your business as legitimate. Are the police going to take that lying down? No. They’re going to consider you a terrorist, and go in guns blazing. So they don’t just protect the interests of the rich after all; that also looks a lot like they’re upholding the law.

I didn’t even express this as the left-wing view earlier, because I’m trying to use the woodman argument; but there are also those on the left who would say that the primary function of the police is to uphold White supremacy. I’d be a fool to deny that there are a lot of White supremacist cops; but notice that in the above scenarios I didn’t even specify the race of the people involved, and didn’t have to. The cops are no more likely to arrest a fraudulent banker because he’s Black, and no more likely to let a hostage-taker go free because he’s White. (They might be less likely to shoot the White hostage-taker—maybe, the data on that actually isn’t as clear-cut as people think—but they’d definitely still arrest him.) While racism is a widespread problem in the police, it doesn’t dictate their behavior all the time—and it certainly isn’t their core function.

What does categorically explain how the police react in all these scenarios?

The police uphold order.

Not law. Order. They don’t actually much seem to care whether what you’re doing is illegal or harmful or even deadly. They care whether it violates civil order.

This is how we can explain the fact that police would investigate murders, but ignore oil rig disasters—even if the latter causes more deaths. The former is a violation of civil order, the latter is not.

It also explains why they would be so willing to tear apart homeless camps and break up protests and strikes. Those are actually often legal, or at worst involve minor infractions; but they’re also disruptive and disorderly.

The police seem to see their core mission as keeping the peace. It could be an unequal, unjust peace full of illegal policies that cause grievous harm and death—but what matters to them is that it’s peace. They will stomp out any violence they see with even greater violence of their own. They have a monopoly on the use of force, and they intend to defend it.

I think that realizing this can help us take a nuanced view of the police. They aren’t monsters or tools of oppression. But they also aren’t brave heroes who uphold the law and keep us safe. They are instruments of civil order.

We do need civil order; there are a lot of very important things in society that simply can’t function if civil order collapses. In places where civil order does fall apart, life becomes entirely about survival; the security that civil order provides is necessary not only for economic activity, but also for much of what gives our lives value.

But nor is civil order all that matters. And sometimes injustice truly does become so grave that it’s worth sacrificing some order in order to redress it. Strikes and protests genuinely are disruptive; society couldn’t function if they were happening everywhere all the time. But sometimes we need to disrupt the way things are going in order to get people to clearly see the injustice around them and do something about it.

I hope that this more realistic, nuanced assessment of the role police play in society may help to pull people away from both harmful political extremes.We can’t simply abolish the police; we need some system for maintaining civil order, and whatever system we have is probably going to end up looking a lot like police. (#ScandinaviaIsBetter, truly, but there are still cops in Norway.) But we also can’t afford to lionize the police or ignore their failures and excesses. When they fight to maintain civil order at the expense of social justice, they become part of the problem.

All of the above really could be done for under $1 trillion. (Some of them would need to be repeated, so we could call it $1 trillion per year.)

I, of course, do not, and will almost certainly never have, anything approaching $1 trillion.

But here’s the thing: There are people who do.

Elon Musk and Jeff Bezos together have a staggering $350 billion. That’s two people with enough money to end world hunger. And don’t give me that old excuse that it’s not in cash: UNICEF gladly accepts donations in stock. They could, right now, give their stocks to UNICEF and thereby end world hunger. They are choosing not to do that. In fact, the goodwill generated by giving, say, half their stocks to UNICEF might actually result in enough people buying into their companies that their stock prices would rise enough to make up the difference—thus costing them literally nothing.

The total net wealth of all the world’s billionaires is a mind-boggling $12.7 trillion. That’s more than half a year of US GDP. Held by just over 2600 people—a small town.

Do these sound like good ideas to you? Would you want to do them? I think most people would want most of them. So now the question becomes: Why aren’t we doing them?

{kind=link}