JDN 2457369

The US corporate income tax is clearly not working.

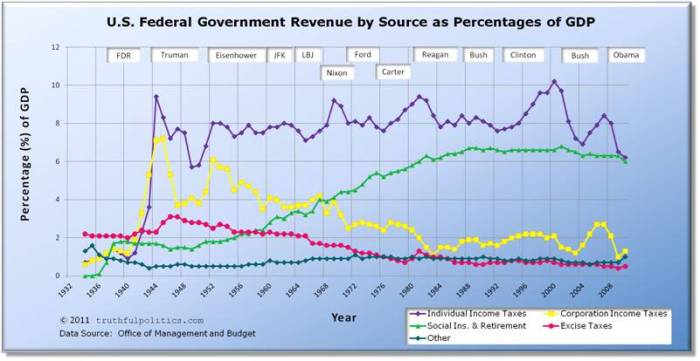

While at one time the corporate income tax took in almost as much revenue as the personal income tax, those days are long gone. In 1934 the personal income tax took in $420 million and the corporate income tax took in $364 million, (adjusted for inflation that’s $7.4 billion and $6.5 billion—still remarkably small! Taxes in the US used to be extremely low; now they are merely quite low). Today, the personal income tax takes in $1.39 trillion while the corporate income tax only takes in $320 billion. As you can see in the graph below (brought to you by Truthful Politics), while personal income tax revenue as a portion of GDP has been about the same since WW2, corporate income tax revenue has been steadily declining.

Part of the problem is that it is so easy for corporations to hide their assets offshore; an estimated $2 trillion is currently held in corporate offshore accounts, almost all of it there to avoid US corporate tax.

The US corporate income tax has some unique features that set it apart from the corporate taxes of most other countries.

One, the rate of the US corporate tax is exceptionally high. That’s highly unusual; for almost every other sort of tax, the US tax rate is among the lowest, particularly when you compare with other First World countries. The United States was in a sense founded upon the idea of not paying taxes, and we have upheld that ideal for two centuries and counting.

Two, the US has a worldwide corporate tax system, whereas most countries have a territorial corporate tax system. In theory, this means that US corporations are required to pay tax on all their profits, wherever they are made, while most countries only require you to pay tax on profits you made in that country.

But wait—didn’t I just say that corporations hide trillions of dollars offshore to avoid US corporate tax? How can they do that, if they’re required to pay tax on all worldwide profits?

In a word? Loopholes.

Two that are particularly popular are inversion and transfer pricing. I won’t bore you with all the details, but basically inversion is when a US company pretends to be owned by a foreign company (I mean, I guess they are legally owned, but only on paper—real leadership rarely changes), so that their profits are now accounted in that foreign country; transfer pricing is a system by which corporations “buy” services from their subsidiaries in other countries, usually at ludicrously high prices in order to justify saying that they took a loss but their subsidiaries (which are not legally US corporations) made huge profits.

Of course, those are far from the only loopholes. There’s a long and ever-expanding list, as loopholes are like the Hydra: Cut off one head and two more shall emerge. For each loophole we close, lobbyists are hard at work creating two more. We must kill it with fire as Hercules did—burn out the entire corporate tax (and lobbying!) system as we know it and make something new.

In fact, most of the money corporations supposedly have “offshore” is actually being stored and spent here in the US. The “accounts” are offshore, but the actual cash, or more likely the actual encrypted servers that store the numbers (for that is what almost all of our money is nowadays—numbers in encrypted servers), are all here in the US. In the rare case that the money itself is actually elsewhere, they just take loans using it as collateral and spend the loan money here—because corporate debt payments are tax-deductible.

So this argument I see a lot that we need a “tax holiday” to encourage corporations to bring their money home and create jobs here is ridiculous. No, they’re already creating any jobs they were planning on creating (which of course they do only on the basis of expected consumer demand).

This money is already being used for everything it would be used for. The only distortion that corporate tax avoidance causes is a lack of tax revenue.

Now, there are two possible ways we could solve this problem in corporate tax reform.

The first is the tack Bernie Sanders takes, and it’s actually one of the few things I strongly disagree with him about. Bernie Sanders plans to reform the corporate tax system in a manner that will force corporations to actually pay taxes on their profits, closing most of these loopholes that allow them to avoid taxation.

The second is the one I favor, and for once I find myself agreeing with the American Enterprise Institute. We should eliminate the corporate tax entirely, and replace it with a higher tax rate on dividends and capital gains. I even rather like their idea of linking the tax rates on capital gains to the tax rates on ordinary income, so there is no longer any incentive to make your income be (or look like—carried interest) capital income instead of labor income.

Now, when I say that I agree with the American Enterprise Institute against Bernie Sanders, an explanation is surely in order. Normally quite the opposite is the case.

Well, first of all I also agree with the business writers in The Atlantic and The New York Times on this one, which should make my view a bit less surprising. But still, I should explain why many liberal economists think that the corporate income tax needs to disappear, since the common perception is that the corporate income tax affects the very rich, and normally liberal economists are all about raising taxes on the very rich in order to raise revenue while minimizing the harms of taxes.

And indeed I am all about raising taxes on the very rich—indeed, my proposed tax plan is the most progressive tax system this side of Eisenhower.

The problem is, we’re not sure if the corporate income tax actually does that.

I created my tax incidence series in large part to make this one fundamental point: The the person who writes the check is not necessarily person who actually pays the tax.

For personal income taxes, we understand their incidence relatively well. While we do think they create some small distortions in the economy as a whole, in general labor is inelastic enough that the burden of a personal income tax falls largely upon the person receiving the income. This makes income taxes a good means of actually redistributing income from one person to another. It’s very hard to disincentivize income; at most we might disincentivize work, and in a country that has twice as many unemployed people as job openings it’s hard for me to see how we have a problem with insufficient work incentives. If the Beveridge Curve ever gets so high up that we actually have more job openings than people looking for jobs, okay, then we can start talking about work incentives. It hasn’t happened at least in my lifetime.

Many economists argue that consumption is an even better thing to tax than income, because they want to increase the savings rate; but I am increasingly convinced that this is not actually a useful thing to do, and indeed that the savings rate is almost literally meaningless. (Perhaps in a future post I’ll talk about why I think so.) I will say this, however: Sales taxes have extremely well-understood incidence. They are the thing that our tax models were originally developed to handle, and they handle it very well. We can predict quite accurately what the effect of increases in sales taxes (or taxes on particular goods, such as alcohol) will be on consumer choices. Their predictability is a reason to recommend them, but in my opinion not sufficient to justify widespread use of sales taxes rather than income taxes.

The incidence of corporate income tax, on the other hand, is almost completely unknown. A substantial amount of research has gone into trying to understand corporate income taxes, but it is still not entirely clear who bears the primary burden of the corporate income tax, whether it is the owners of a corporation, its employees, or its customers. Because, pace Citizens United, corporations are not actually people. Corporations do not experience utility that can be raised or lowered. The money they make ultimately goes to actual human beings, and it’s those actual human beings we are interested in taxing.

To see this, think about what happens when we impose a tax on a corporation’s profits. One possibility is that their behavior is completely inelastic: They’ll just keep doing exactly the same thing they were doing, only now making less profit. But does that seem likely? No, it’s far more likely that they’re going to try to find some way to avoid the tax, or at least reduce how much they have to pay. They’ll use offshore banking and clever accounting methods to make it look like they have less profit than they really do. Even worse, they may even change the way that they run their company—producing fewer products or raising prices, laying off employees or reducing wages. They may decide not to make investments they otherwise would have, or overspend on capital they don’t actually need just for the tax deduction. All of these activities create real distortions in the economy and cause deadweight loss; and the harm they cause to employees or consumers could be much larger than the pain they impose on the owners of the corporation.

If we knew which of these strategies corporations would take, then we could predict the outcome and base our tax policy on that. But at present we are unable to do that. In fact, all of these strategies are probably employed by various corporations, and what we most care about is the aggregate effect—but we are currently unable to predict even that.

Indeed, given that they have so many options, it is most likely that the owners of corporations do not bear the burden of corporate income taxes. As you may recall from my tax incidence series, the person who bears a tax is the one who is least elastic; that is, the one who changes their behavior in response to the tax the least. This is likely to be the one who has the fewest alternatives—and employees and consumers have far fewer alternatives than corporate executives do. Indeed, employees probably have the fewest alternatives, and are likely the most inelastic; thus, they are probably the ones who actually bear the burden of the corporate income tax. And most inelastic of all are the employees at the bottom of the ladder (or should I say primate hierarchy), people like interns, janitors, and cashiers.

It may be counter-intuitive, but it is most likely true: By eliminating the corporate income tax, we will most likely create jobs and raise wages, especially for the people at the bottom. Janitors and cashiers may be the ones who feel the largest increase in pay.

There is a legitimate concern that raising capital gains rates could even have a similar effect. Under certain assumptions, the Atkinson-Stiglitz Theorem famously says that taxes on capital income cannot be used to redistribute wealth because they will impose more cost on workers than they raise in revenue for the transfer. They would reduce inequality only at the cost of reducing overall income, which clearly isn’t what we want. That would actually violate the Difference Principle, the seminal contribution to the theory of distributive justice we owe to John Rawls.

But the assumptions of that theorem are highly unrealistic, as I discussed in an earlier post. With a realistic idea of how capital income is actually allocated (I honestly can’t bear to say “earned” in this context), it becomes fairly obvious that taxes on capital income create minimal, if any, real distortions on hiring and investment. While corporate profits are fairly closely tied to the actual production and distribution of goods, capital income most assuredly is not. A corporate income tax takes money away from a corporation such as Apple or Boeing (well, not Apple or Boeing in particular, since they avoid it expertly; but the corporations that aren’t big enough to avoid corporate taxes are largely ones you’ve never heard of—yet another reason they’re unfair), who then most likely take it from their employees or their customers. A capital gains tax takes money away from people who bought and sold shares of Apple and Boeing, possibly thousands of times per second, people who most likely don’t even work there, have nothing to do with any decisions those companies have ever made, and may not even buy any of their products. I think you can see why in the latter case the decisions of the company are a lot less likely to be distorted.

It’s also harder to avoid capital gains taxes (albeit by no means impossible), especially if they are structured properly without loopholes. Thus, the same nominal rate on capital gains instead of corporate profits would likely raise a great deal more revenue.

In short, the corporate income tax is not working; I say we get rid of it altogether.

[…] during the Roaring Twenties—the top tax rate was 25% from 1925 to 1931. Trump also proposes to cut the corporate tax in half (which I actually like), and eliminate the payroll tax completely—which would only make sense if you absorbed it into […]

LikeLike

[…] I’m actually fairly ambivalent about corporate taxes in general. Their incidence really isn’t well-understood, though as Krugman has pointed out, so much of corporate profit is now monopoly rent that we can reasonably expect most of the incidence to fall on shareholders. What I’d really like to see happen is a repeal of the corporate tax combined with an increase in capital gains taxes. But we haven’t been increasing capital gains taxes; we’ve just been cutting corporate taxes. […]

LikeLike

[…] as a philosophy in general. I actually worry about that; not all conservative ideas are wrong! Low corporate taxes actually make a lot of sense. Minimum wage isn’t that harmful, but it’s also not that beneficial. Climate change is […]

LikeLike