Jan 9 JDN 2459589

Labor markets have been behaving quite strangely lately, due to COVID and its consequences. As I said in an earlier post, the COVID recession was the one recession I can think of that actually seemed to follow Real Business Cycle theory—where it was labor supply, not demand, that drove employment.

I dare say that for the first time in decades, the US government actually followed Keynesian policy. US federal government spending surged from $4.8 trillion to $6.8 trillion in a single year:

That is a staggering amount of additional spending; I don’t think any country in history has ever increased their spending by that large an amount in a single year, even inflation-adjusted. Yet in response to a recession that severe, this is exactly what Keynesian models prescribed—and for once, we listened. Instead of balking at the big numbers, we went ahead and spent the money.

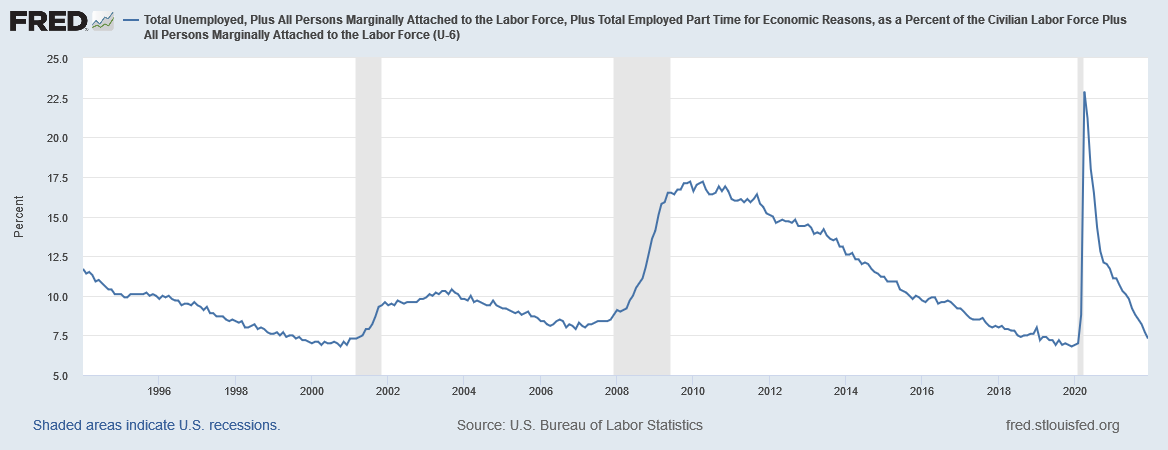

And apparently it worked, because unemployment spiked to the worst levels seen since the Great Depression, then suddenly plummeted back to normal almost immediately:

Nor was this just the result of people giving up on finding work. U-6, the broader unemployment measure that includes people who are underemployed or have given up looking for work, shows the same unprecedented pattern:

The oddest part is that people are now quitting their jobs at the highest rate seen in over 20 years:

[FRED_quits.png]

This phenomenon has been dubbed the Great Resignation, and while its causes are still unclear, it is clearly the most important change in the labor market in decades.

In a previous post I hypothesized that this surge in strikes and quits was a coordination effect: The sudden, consistent shock to all labor markets at once gave people a focal point to coordinate their decision to strike.

But it’s also quite possible that it was the Keynesian stimulus that did it: The relief payments made it safe for people to leave jobs they had long hated, and they leapt at the opportunity.

When that huge surge in government spending was proposed, the usual voices came out of the woodwork to warn of terrible inflation. It’s true, inflation has been higher lately than usual, nearly 7% last year. But we still haven’t hit the double-digit inflation rates we had in the late 1970s and early 1980s:

Indeed, most of the inflation we’ve had can be explained by the shortages created by the supply chain crisis, along with a very interesting substitution effect created by the pandemic. As services shut down, people bought goods instead: Home gyms instead of gym memberships, wifi upgrades instead of restaurant meals.

As a result, the price of durable goods actually rose, when it had previously been falling for decades. That broader pattern is worth emphasizing: As technology advances, services like healthcare and education get more expensive, durable goods like phones and washing machines get cheaper, and nondurable goods like food and gasoline fluctuate but ultimately stay about the same. But in the last year or so, durable goods have gotten more expensive too, because people want to buy more while supply chains are able to deliver less.

This suggests that the inflation we are seeing is likely to go away in a few years, once the pandemic is better under control (or else reduced to a new influenza where the virus is always there but we learn to live with it).

But I don’t think the effects on the labor market will be so transitory. The strikes and quits we’ve been seeing lately really are at a historic level, and they are likely to have a long-lasting effect on how work is organized. Employers are panicking about having to raise wages and whining about how “no one wants to work” (meaning, of course, no one wants to work at the current wage and conditions on offer). The correct response is the one from Goodfellas [language warning].

For the first time in decades, there are actually more job vacancies than unemployed workers:

This means that the tables have turned. The bargaining power is suddenly in the hands of workers again, after being in the hands of employers for as long as I’ve been alive. Of course it’s impossible to know whether some other shock could yield another reversal; but for now, it looks like we are finally on the verge of major changes in how labor markets operate—and I for one think it’s about time.