JDN 2457341

One of the most important aspects of taxation is also one of the most counter-intuitive and (relatedly) least-understood: Taxes are not externally applied to pre-existing exchanges of money. Taxes endogenously interact with the system of prices, changing what the prices will be and then taking a portion of the money exchanged.

The price of something “before taxes” is not actually the price you would pay for it if there had been no taxes on it. Your “pre-tax income” is not actually the income you would have had if there were no income or payroll taxes.

The most obvious case to consider is that of government employees: If there were no taxes, public school teachers could not exist, so the “pre-tax income” of a public school teacher is a meaningless quantity. You don’t “take taxes out” of a government salary; you decide how much money the government employee will actually receive, and then at the same time allocate a certain amount into other budgets based on the tax code—a certain amount into the state general fund, a certain amount into the Social Security Trust Fund, and so on. These two actions could in principle be done completely separately; instead of saying that a teacher has a “pre-tax salary” of $50,000 and is taxed 20%, you could simply say that the teacher receives $40,000 and pay $10,000 into the appropriate other budgets.

In fact, when there is a conflict of international jurisdiction this is sometimes literally what we do. Employees of the World Bank are given immunity from all income and payroll taxes (effectively, diplomatic immunity, though this is not usually how we use the term) based on international law, except for US citizens, who have their taxes paid for them by the World Bank. As a result, all World Bank salaries are quoted “after-tax”, that is, the actual amount of money employees will receive in their paychecks. As a result, a $120,000 salary at the World Bank is considerably higher than a $120,000 salary at Goldman Sachs; the latter would only (“only”) pay about $96,000 in real terms.

For private-sector salaries, it’s not as obvious, but it’s still true. There is actually someone who pays that “before-tax” salary—namely, the employer. “Pre-tax” salaries are actually a measure of labor expenditure (sometimes erroneously called “labor costs”, even by economists—but a true labor cost is the amount of effort, discomfort, stress, and opportunity cost involved in doing labor; it’s an amount of utility, not an amount of money). The salary “before tax” is the amount of money that the employer has to come up with in order to pay their payroll. It is a real amount of money being exchanged, divided between the employee and the government.

The key thing to realize is that salaries are not set in a vacuum. There are various economic (and political) pressures which drive employers to set different salaries. In the real world, there are all sorts of pressures that affect salaries: labor unions, regulations, racist and sexist biases, nepotism, psychological heuristics, employees with different levels of bargaining skill, employers with different concepts of fairness or levels of generosity, corporate boards concerned about public relations, shareholder activism, and so on.

But even if we abstract away from all that for a moment and just look at the fundamental economics, assuming that salaries are set at the price the market will bear, that price depends upon the tax system.

This is because taxes effectively drive a wedge between supply and demand.

Indeed, on a graph, it actually looks like a wedge, as you’ll see in a moment.

Let’s pretend that we’re in a perfectly competitive market. Everyone is completely rational, we all have perfect information, and nobody has any power to manipulate the market. We’ll even assume that we are dealing with hourly wages and we can freely choose the number of hours worked. (This is silly, of course; but removing this complexity helps to clarify the concept and doesn’t change the basic result that prices depend upon taxes.)

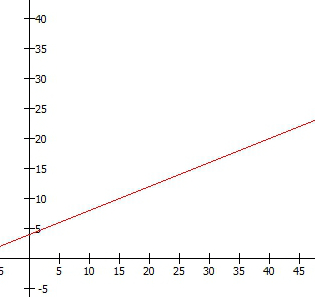

We’ll have a supply curve, which is a graph of the minimum price the worker is willing to accept for each hour in order to work a given number of hours. We generally assume that the supply curve slopes upward, meaning that people are willing to work more hours if you offer them a higher wage for each hour. The idea is that it gets progressively harder to find the time—it eats into more and more important alternative activities. (This is in fact a gross oversimplification, but it’ll do for now. In the real world, labor is the one thing for which the supply curve frequently bends backward.)

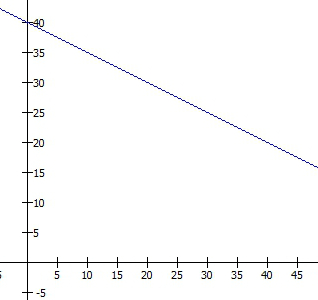

We’ll also have a demand curve, which is a graph of the maximum price the employer is willing to pay for each hour, if the employee works that many hours. We generally assume that the demand curve slopes downward, meaning that the employer is willing to pay less for each hour if the employee works more hours. The reason is that most activities have diminishing marginal returns, so each extra hour of work generally produces less output than the previous hour, and is therefore not worth paying as much for. (This too is an oversimplification, as I discussed previously in my post on the Law of Demand.)

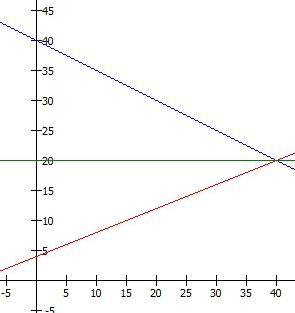

Put these two together, and in a competitive market the price will be set at the point at which supply is equal to demand, so that the very last hour of work was worth exactly what the employer paid for it. That last hour is just barely worth it to the employer, and just barely worth it to the worker; any additional time would either be too expensive for the employer or not lucrative enough for the worker. But for all the previous hours, the value to the employer is higher than the wage, and the cost to the worker is lower than the wage. As a result, both the employer and the worker benefit.

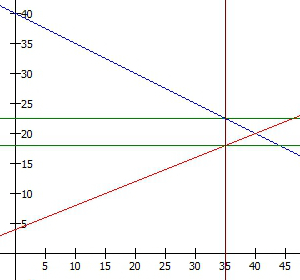

But now, suppose we implement a tax. For concreteness, suppose the previous market-clearing wage was $20 per hour, the worker was working 40 hours, and the tax is 20%. If the employer still offers a wage of $20 for 40 hours of work, the worker is no longer going to accept it, because they will only receive $16 per hour after taxes, and $16 isn’t enough for them to be willing to work 40 hours. The worker could ask for a pre-tax wage of $25 so that the after-tax wage would be $20, but then the employer will balk, because $25 per hour is too expensive for 40 hours of work.

In order to restore the balance (and when we say “equilibrium”, that’s really all we mean—balance), the employer will need to offer a higher pre-tax wage, which means they will demand fewer hours of work. The worker will then be willing to accept a lower after-tax wage for those reduced hours.

In effect, there are now two prices at work: A supply price, the after-tax wage that the worker receives, which must be at or above the supply curve; and a demand price, the pre-tax wage that the employer pays, which must be at or below the demand curve. The difference between those two prices is the tax.

In this case, I’ve set it up so that the pre-tax wage is $22.50, the after-tax wage is $18, and the amount of the tax is $4.50 or 20% of $22.50. In order for both the employer and the worker to accept those prices, the amount of hours worked has been reduced to 35.

As a result of the tax, the wage that we’ve been calling “pre-tax” is actually higher than the wage that the worker would have received if the tax had not existed. This is a general phenomenon; it’s almost always true that your “pre-tax” wage or salary overestimates what you would have actually gotten if the tax had not existed. In one extreme case, it might actually be the same; in another extreme case, your after-tax wage is what you would have received and the “pre-tax” wage rises high enough to account for the entirety of the tax revenue. It’s not really “pre-tax” at all; it’s the after-tax demand price.

Because of this, it’s fundamentally wrongheaded for people to complain that taxes are “taking your hard-earned money”. In all but the most exceptional cases, that “pre-tax” salary that’s being deducted from would never have existed. It’s more of an accounting construct than anything else, or like I said before a measure of labor expenditure. It is generally true that your after-tax salary is lower than the salary you would have gotten without the tax, but the difference is generally much smaller than the amount of the tax that you see deducted. In this case, the worker would see $4.50 per hour deducted from their wage, but in fact they are only down $2 per hour from where they would have been without the tax. And of course, none of this includes the benefits of the tax, which in many cases actually far exceed the costs; if we extended the example, it wouldn’t be hard to devise a scenario in which the worker who had their wage income reduced received an even larger benefit in the form of some public good such as national defense or infrastructure.

[…] Our journey through the world of taxes continues. I’ve already talked about how taxes have upsides and downsides, as well as how taxes directly affect prices and “before-tax” prices are almost meaningless. […]

LikeLike

[…] return to our previous example, where a 20% tax raised the original wage from $22.50 and thus resulted in an after-tax wage of […]

LikeLike

[…] earlier posts I discussed how taxes have important downsides, then talked about how taxes can distort prices, then explained that taxes are actually what gives money its value. In the most recent post in the […]

LikeLike