JDN 2457299 EDT 17:03

In recent posts I talked about demand and then I talked about supply. Now it’s time to talk about both at once–which is where the real magic happens. Alfred Marshall famously compared supply and demand to the lower and upper blades of a pair of scissors:

We might as reasonably dispute whether it is the upper or the under blade of a pair of scissors that cuts a piece of paper, as whether value is governed by utility or cost of production. It is true that when one blade is held still, and the cutting is effected by moving the other, we may say with careless brevity that the cutting is done by the second; but the statement is not strictly accurate, and is to be excused only so long as it claims to be merely a popular and not a strictly scientific account of what happens.

Before Marshall, it was actually rather common to debate whether prices are determined by supply or by demand. Actually there seems to be a certain branch of Marxists today who insist upon the “labor theory of value” that seems to rest upon a similar sort of confusion, basically saying that the real value of something is entirely determined by its cost of supply. If the value of something were strictly determined by the labor put into making it, there would be literally no reason to ever make anything. If the value you get from a good is precisely equal to the labor put into it, there is no net benefit to ever making any goods. At most, embodying labor in a product might allow you to transfer labor from one person to another; but there would be no such thing as real economic growth. In order to have real economic growth, products must end up being worth more than what it cost to make them—that is, their value of demand must exceed their cost of supply.

Toward the other end of the political spectrum, we have “Say’s Law”, which says that “supply creates its own demand”; that is, that there is never any such thing as too much or too little overall demand in an economy, because supplying a good automatically makes that good available to trade for something else. I hate to even call it a “law” because isn’t even like the Pirate Code; it’s not even useful as a guideline, it’s just flat wrong. There is absolutely no reason that making something would make someone else want to buy it from you. You can make all sorts of things that nobody wants to buy; the possibilities are endless, really. Balls of lint dusted with powdered sugar, broken ballpoint pens dipped in motor oil, burnt-out lightbulbs covered in melted Swiss cheese. It’s possible that someone might want to buy such bizarre items (call them “postmodernist found art” or something), but there clearly isn’t a large market for such goods, even if you should decide to manufacture thousands of them. Even in an aggregate sense, there’s also no particular reason to think that we can’t have an economy where millions of products pile up on shelves because no one can afford to buy them; indeed, that’s basically what happens in a recession.

In fact, the converse, “demand creates its own supply”, is considerably closer to true. It’s still not strictly true—centuries of searching for the elixir of immortality have failed to produce it, though modern genetic engineering just might finally succeed where all else has failed. (After all, every new technology is impossible… until it isn’t.) But in the long run, this converse law (it doesn’t have a name so far as I know) does contain an important grain of truth: If people want something badly enough, they will spend enormous resources in order to find a way to get it. If you know that a lot of people want something that no one is supplying, it behooves you to find a way to provide it—it might just make you a billionaire. Over centuries of technological advancement, humanity has found ways to provide many goods and services that were previously thought impossible, and one of the central benefits of a capitalist economy is that it provides powerful economic incentives for entrepreneurs to innovate and find ways to provide goods that people have always wanted but never had. Yet, even so, it isn’t true that demand creates its own supply—certainly not in the short run.

Neither supply or demand on its own does much of anything. You can have insatiable demand for something nobody can supply (the aforementioned elixir of immortality), and it still won’t be sold. You can have endless supply of something nobody demands (vacuum?), and it will remain worthless. It’s only when you have both supply and demand that a market becomes possible.

One of the central insights of modern economics is that prices and quantities in a capitalist market are determined simultaneously by supply and demand. In general, both supply and demand are constantly changing in response to events in the world, and thus the prices and quantities of goods shift from one equilibrium to another. In order to predict exactly how they will shift, we would need to know how both supply and demand have changed.

As Marshall alludes to in the above quotation, in some cases we can take either supply or demand as fixed and then the other one is what matters; but these are only special cases. In general, both supply and demand are subject to the winds of changing markets, and we need to keep track of both at once. If that sounds really difficult, that’s because it is—most of what economists do in the real world ultimately amounts to finding ways to distinguish supply effects from demand effects in various situations. Even most statistical methods in econometrics were basically designed as means of separating out demand-related causes from supply-related causes.

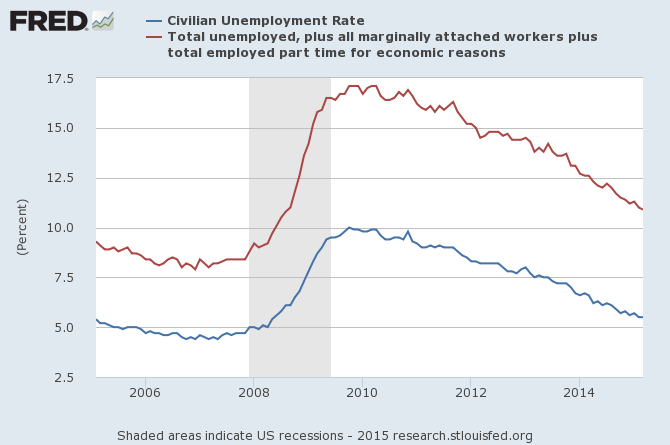

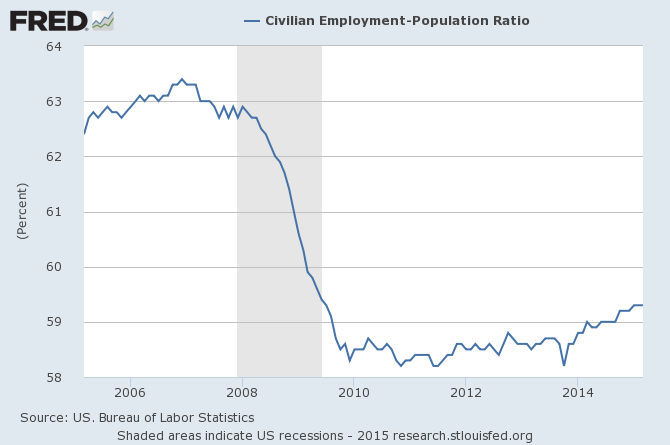

A lot of policy questions ultimately depend upon whether supply or demand is the dominant factor: If the business cycle is primarily driven by changes in demand, it makes sense to use monetary and fiscal policy to stabilize the economy (short version: it is, and it does). If it were instead driven by supply (“supply-side economics”), it would instead be better to make structural changes that reduce costs of production. (Why is this obviously wrong? Because there weren’t sudden increases in production costs in 2008—but there was a sudden collapse of consumer buying power. Maybe the 1973 recession can be explained by a sudden increase in oil prices, but there was no such supply shock in 2008.) If the labor market is primarily driven by demand, we need to find ways to get business to hire more people; but if it’s primarily driven by supply, we need to find ways to get people to get off their butts and try to find work. (Again, I think it’s pretty obvious that the former is true, not the latter—since at least 2000 there have never been as many job openings in the US as there were unemployed people.)

In the above policy questions the liberal view is the demand-side and the conservative view is the supply-side, but that need not be the case. Regarding renewable energy, for example, the more liberal view is that lots of people would want to buy electric cars and solar panels, if they were made available, but they aren’t—we are supply-constrained. The more conservative view is that the reason they aren’t selling more is that nobody particularly wants them and trying to force them on us is a fool’s errand—we are demand-constrained. Likewise when it comes to banking, liberals generally think that the reason there isn’t more credit is that banks refuse to supply loans, while conservatives (particularly from the banks themselves) usually argue that it’s because people aren’t willing to take the risk of taking out more loans.

The point, however, is that a lot of policy debates ultimately hinge upon the question of whether demand or supply is more important in driving a particular market—and since sometimes they are both important, sometimes the policy solution requires a combination of different approaches. One of the advantages of quantitative economic analysis is that we can determine exactly how much the costs and benefits of each policy option will be, and thereby choose the one that is most cost-effective.

In this way, “supply or demand?” is a lot like “nature or nurture?”; the answer is always “both”, but there are times when one factor or the other is more important for the policy question at hand.