JDN 2457345 EST 22:02

As I was writing this, it was very early (I had to wake up at 04:30) and I was groggy, because we were on an urgent road trip to Pennsylvania for the funeral of my aunt who died quite suddenly a few days ago. I have since edited this post more thoroughly to minimize the impact of my sleep deprivation upon its content. Actually maybe this is a good thing; the saying goes, “write drunk, edit sober” and sleep deprivation and alcohol have remarkably similar symptoms, probably because alcohol is GABA-ergic and GABA is involved in sleep regulation.

Awhile ago I wrote a long post on tax incidence, but the primary response I got was basically the online equivalent of a perplexed blank stare. Struck once again by the Curse of Knowledge, I underestimated the amount of background knowledge necessary to understand my explanation. But tax incidence is very important for public policy, so I really would like to explain it.

Therefore I am now starting again, slower, in smaller pieces. Today’s piece is about the downsides of taxation in general, why we don’t just raise taxes as high as we feel like and make the government roll in dough.

To some extent this is obvious; if income tax were 100%, why would anyone bother working for a salary? You might still work for fulfillment, or out of a sense of duty, or simply because you enjoy what you do—after all, most artists and musicians are hardly in it for the money. But many jobs are miserable and not particularly fulfilling, yet still need to get done. How many janitors or bus drivers work purely for the sense of fulfillment it gives them? Mostly they do it to pay the bills—and if income tax were 100%, it wouldn’t anymore. The formal economy would basically collapse, and then nobody would end up actually paying that 100% tax—so the government would actually get very little revenue, if any.

At the other end of the scale, it’s kind of obvious that if your taxes are all 0% you don’t get any revenue. This is actually more feasible than it may sound; provided you spend only a very small amount (say, 4% of GDP, though that’s less than any country actually spends—maybe you could do 6% like Bangladesh) and you can still get people to accept your currency, you could, in principle, have a government that funds its spending entirely by means of printing money, and could do this indefinitely. In practice, that has never been done, and the really challenging part is getting people to accept your money if you don’t collect taxes in it. One of the more counter-intuitive aspects of modern monetary theory (or perhaps I should capitalize it, Modern Monetary Theory, though the part I agree with is not that different from standard Keynesian theory) is that taxation is the primary mechanism by which money acquires its value.

And then of course with intermediate tax rates such as 20%, 30%, and 50% that actual countries actually use, we do get some positive amount of revenue.

Everything I’ve said so far may seem pretty obvious. Yeah, usually taxes raise revenue, but if you taxed at 0% or 100% they wouldn’t; so what?

Well, this leads to quite an important result. Assuming that tax revenue is continuous (which isn’t quite true, but since we can collect taxes in fractions of a percent and pay in pennies, it’s pretty close), it follows directly from the Extreme Value Theorem that there is in fact a revenue-maximizing tax rate. Both below and above that tax rate, the government takes in less total money. These theorems don’t tell us what the revenue-maximizing rate is; but they tell us that it must exist, somewhere between 0% and 100%.

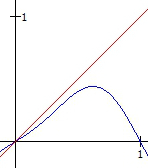

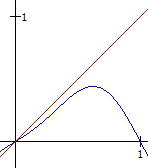

Indeed, it follows that there is what we call the Laffer Curve, a graph of tax revenue as a function of tax rate, and it is in fact a curve, as opposed to the straight line it would be if taxes had no effect on the rest of the economy.

Very roughly, it looks something like this (the blue curve is my sketch of the real-world Laffer curve, while the red line is what it would be if taxes had no distortionary effects):

Now, the Laffer curve has been abused many times; in particular, it’s been used to feed into the “trickle-down” “supply-side” Reaganomics that has been rightly derided as “voodoo economics” by serious economists. Jeb Bush (or should I say, Jeb!) and Marco Rubio would have you believe that we are on the right edge of the Laffer curve, and we could actually increase tax revenue by cutting taxes, particularly on capital gains and incomes at the top 1%; that’s obviously false. We tried that, it didn’t work. Even theoretically we probably should have known that it wouldn’t; but now that we’ve actually done the experiment and it failed, there should be no serious doubt anymore.

No, we are on the left side of the Laffer curve, where increasing taxes increases revenue, much as you’d intuitively expect. It doesn’t quite increase one-to-one, because adding more taxes does make the economy less efficient; but from where we currently stand, a 1% increase in taxes leads to about a 0.9% increase in revenue (actually estimated as between 0.78% and 0.99%).

Denmark may be on the right side of the Laffer curve, where they could raise more revenue by decreasing tax rates (even then I’m not so sure). But Denmark’s tax rates are considerably higher than ours; while in the US we pay about 27% of GDP in taxes, folks in Denmark pay 49% of GDP in taxes.

The fact remains, however, that there is a Laffer curve, and no serious economist would dispute this. Increasing taxes does in fact create distortions in the economy, and as a result raising tax rates does not increase revenue in a one-to-one fashion. When calculating the revenue from a new tax, you must include not only the fact that the government will get an increased portion, but also that the total amount of income will probably decrease.

Now, I must say probably, because it does depend on what exactly you are taxing. If you tax something that is perfectly inelastic—the same amount of it is going to be made and sold no matter what—then total income will remain exactly the same after the tax. It may be distributed differently, but the total won’t change. This is one of the central justifications for a land tax; land is almost perfectly inelastic, so taxing it allows us to raise revenue without reducing total income.

In fact, there are certain kinds of taxes which increase total income, which makes them basically no-brainer taxes that should always be implemented if at all feasible. These are Pigovian taxes, which are taxes on products with negative externalities; when a product causes harm to other people (the usual example is pollution of air and water), taxing that product equal to the harm caused provides a source of government revenue that also increases the efficiency of the economy as a whole. If we had a tax on carbon emissions that was used to fund research into sustainable energy, this would raise our total GDP in the long run. Taxes on oil and natural gas are not “job killing”; they are job creating. This is why we need a carbon tax, a higher gasoline tax, and a financial transaction tax (to reduce harmful speculation); it’s also why we already have high taxes on alcohol and tobacco.

The alcohol tax is one of the great success stories of Pigouvian taxation.The alcohol tax is actually one of the central factors holding our crime rate so low right now. Another big factor is overall economic growth and anti-poverty programs. The most important factor, however, is lead, or rather the lack thereof; environmental regulations reducing pollutants like lead and mercury from the environment are the leading factor in reducing crime rates over the last generation. Yes, that’s right—our fall in crime had little to do with state police, the FBI, the DEA, or the ATF; our most effective crime-fighting agency is the EPA. This is really not that surprising, as a cognitive economist. Most crime is impulsive and irrational, or else born of economic desperation. Rational crime that it would make sense to punish harshly as a deterrent is quite rare (well, except for white-collar crime, which of course we don’t punish harshly enough—I know I harp on this a lot, but HSBC laundered money for terrorists). Maybe crime would be more common if we had no justice system in place at all, but making our current system even harsher accomplishes basically nothing. Far better to tax the alcohol that leads good people to bad decisions.

It also matters whom you tax, though one of my goals in this tax incidence series is to explain why that doesn’t mean quite what most people think it does. The person who writes the check to the government is not necessarily the person who really pays the tax. The person who really pays is the one whose net income ends up lower after the tax is implemented. Often these are the same person; but often they aren’t, for fundamental reasons I’m hoping to explain.

For now, it’s worth pointing out that a tax which primarily hits the top 1% is going to have a very different impact on the economy than one which hits the entire population. Because of the income and substitution effects, poor people tend to work less as their taxes go up, but rich people tend to work more. Even within income brackets, a tax that hits doctors and engineers is going to have a different effect than a tax that hits bankers and stock traders, and a tax that hits teachers is going to have a different effect than a tax that hits truck drivers. A tax on particular products or services will reduce demand for those products or services, which is good if that’s what you’re trying to do (such as alcohol) but not so good if it isn’t.

So, yes, there are cases where raising taxes can actually increase, or at least not reduce, total income. These are the exception, however; as a general rule, in a Pirate Code sort of way, taxes reduce total income. It’s not simply that income goes down for everyone but the government (which would again be sort of obvious); income goes down for everyone including the government. The difference is simply lost, wasted away by a loss in economic efficiency. We call that difference deadweight loss, and for a poorly-designed tax it can actually far exceed the revenue received.

I think an extreme example may help to grasp the intuition: Suppose we started taxing cars at 200,000%, so that a typical new car costs something like $40 million with taxes. (That’s not a Lamborghini, mind you; that’s a Honda Accord.) What would happen? Nobody is going to buy cars anymore. Overnight, you’ve collapsed the entire auto industry. Dozens of companies go bankrupt, thousands of employees get laid off, the economy immediately falls into recession. And after all that, your car tax will raise no revenue at all, because not a single car will sell. It’s just pure deadweight loss.

That’s an intentionally extreme example; most real-world taxes in fact create less deadweight loss than they raise in revenue. But most real-world taxes do in fact create deadweight loss, and that’s a good reason to be concerned about any new tax.

In general, higher taxes create lower total income, or equivalently higher deadweight loss. All other things equal, lower taxes are therefore better.

What most Americans don’t seem to quite grasp is that all other things are not equal. That tax revenue is central to the proper functioning of our government and our monetary system. We need a certain amount of taxes in order to ensure that we can maintain a stable currency and still pay for things like Medicare, Social Security, and the Department of Defense (to name our top three budget items).

Alternatively, we could not spend so much on those things, and that is a legitimate question of public policy. I personally think that Medicare and Social Security are very good things (and I do have data to back that up—Medicare saves thousands of lives), but they aren’t strictly necessary for basic government functioning; we could get rid of them, it’s just that it would be a bad idea. As for the defense budget, some kind of defense budget is necessary for national security, but I don’t think I’m going out on a very big limb here when I say that one country making 40% of all world military spending probably isn’t.

We can’t have it both ways; if you want Medicare, Social Security, and the Department of Defense, you need to have taxes. “Cutting spending” always means cutting spending on something—so what is it you want to cut? A lot of people seem to think that we waste a huge amount of money on pointless bureaucracy, pork-barrel spending, or foreign aid; but that’s simply not true. All government administration is less than 1% of the budget, and most of it is necessary; earmarks are also less than 1%; foreign aid is also less than 1%. Since our deficit is about 15% of spending, we could eliminate all of those things and we’d barely put a dent in it.

Americans don’t like taxes; I understand that. It’s basically one of our founding principles, in fact, though “No taxation without representation” seems to have mutated of late into simply “No taxation”, or maybe “Read my lips, no new taxes!” It’s never pleasant to see that chunk taken out of your paycheck before you even get it. (Though one thing I hope to explain in this series is that these figures are really not very meaningful; there’s no particular reason to think you’d have made the same gross salary if those taxes hadn’t been present.)

There are in fact sound economic reasons to keep taxes low. The Laffer Curve is absolutely a real thing, even though most of its applications are wrong. But sometimes we need taxes to be higher, and that’s a tradeoff we have to make.We need to have a serious public policy discussion about where our priorities lie, not keep trading sound-bytes about “cutting wasteful spending” and “job-killing tax hikes”.