JDN 2457152 EDT 14:54.

I said in my previous post that I consider tax incidence to be one of the top ten things you should know about economics. If I actually try to make a top ten list, I think it goes something like this:

- Supply and demand

- Monopoly and oligopoly

- Externalities

- Tax incidence

- Utility, especially marginal utility of wealth

- Pareto-efficiency

- Risk and loss aversion

- Biases and heuristics, including sunk-cost fallacy, scope neglect, herd behavior, anchoring and representative heuristic

- Asymmetric information

- Winner-takes-all effect

So really tax incidence is in my top five things you should know about economics, and yet I still haven’t talked about it very much. Well, today I will. The basic principles of supply and demand I’m basically assuming you know, but I really should spend some more time on monopoly and externalities at some point.

Why is tax incidence so important? Because of one central fact: The person who pays the tax is not the person who writes the check.

It doesn’t matter whether a tax is paid by the buyer or the seller; it matters what the buyer and seller can do to avoid the tax. If you can change your behavior in order to avoid paying the tax—buy less stuff, or buy somewhere else, or deduct something—you will not bear the tax as much as someone else who can’t do anything to avoid the tax, even if you are the one who writes the check. If you can avoid it and they can’t, other parties in the transaction will adjust their prices in order to eat the tax on your behalf.

Thus, if you have a good that you absolutely must buy no matter what—like, say, table salt—and then we make everyone who sells that good pay an extra $5 per kilogram, I can guarantee you that you will pay an extra $5 per kilogram, and the suppliers will make just as much money as they did before. (A salt tax would be an excellent way to redistribute wealth from ordinary people to corporations, if you’re into that sort of thing. Not that we have any trouble doing that in America.)

On the other hand, if you have a good that you’ll only buy at a very specific price—like, say, fast food—then we can make you write the check for a tax of an extra $5 per kilogram you use, and in real terms you’ll pay hardly any tax at all, because the sellers will either eat the cost themselves by lowering the prices or stop selling the product entirely. (A fast food tax might actually be a good idea as a public health measure, because it would reduce production and consumption of fast food—remember, heart disease is one of the leading causes of death in the United States, making cheeseburgers a good deal more dangerous than terrorists—but it’s a bad idea as a revenue measure, because rather than pay it, people are just going to buy and sell less.)

In the limit in which supply and demand are both completely fixed (perfectly inelastic), you can tax however you want and it’s just free redistribution of wealth however you like. In the limit in which supply and demand are both locked into a single price (perfectly elastic), you literally cannot tax that good—you’ll just eliminate production entirely. There aren’t a lot of perfectly elastic goods in the real world, but the closest I can think of is cash. If you instituted a 2% tax on all cash withdrawn, most people would stop using cash basically overnight. If you want a simple way to make all transactions digital, find a way to enforce a cash tax. When you have a perfect substitute available, taxation eliminates production entirely.

To really make sense out of tax incidence, I’m going to need a lot of a neoclassical economists’ favorite thing: Supply and demand curves. These things pop up everywhere in economics; and they’re quite useful. I’m not so sure about their application to things like aggregate demand and the business cycle, for example, but today I’m going to use them for the sort of microeconomic small-market stuff that they were originally designed for; and what I say here is going to be basically completely orthodox, right out of what you’d find in an ECON 301 textbook.

Let’s assume that things are linear, just to make the math easier. You’d get basically the same answers with nonlinear demand and supply functions, but it would be a lot more work. Likewise, I’m going to assume a unit tax on goods—like $2890 per hectare—as opposed to a proportional tax on sales—like 6% property tax—again, for mathematical simplicity.

The next concept I’m going to have to talk about is elasticity—which is the proportional amount that quantity sold changes relative to price. If price increases 2% and you buy 4% less, you have a demand elasticity of -2. If price increases 2% and you buy 1% less, you have a demand elasticity of -1/2. If price increases 3% and you sell 6% more, you have a supply elasticity of 2. If price decreases 5% and you sell 1% less, you have a supply elasticity of 1/5.

Elasticity doesn’t have any units of measurement, it’s just a number—which is part of why we like to use it. It also has some very nice mathematical properties involving logarithms, but we won’t be needing those today.

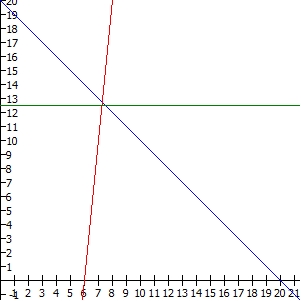

The price that renters are willing and able to pay, the demand price PD will start at their maximum price, the reserve price PR, and then it will decrease linearly according to the quantity of land rented Q, according to a linear function (simply because we assumed that) which will vary according to a parameter e that represents the elasticity of demand (it isn’t strictly equal to it, but it’s sort of a linearization).

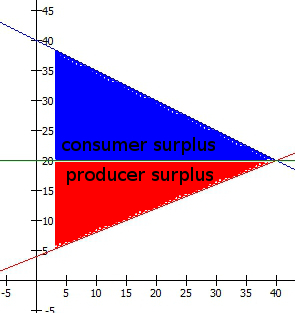

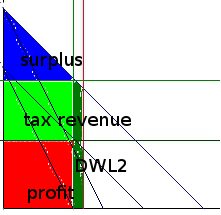

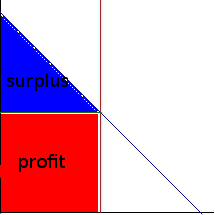

We’re interested in what is called the consumer surplus; it is equal to the total amount of value that buyers get from their purchases, converted into dollars, minus the amount they had to pay for those purchases. This we add to the producer surplus, which is the amount paid for those purchases minus the cost of producing them—which is basically just the same thing as profit. Togerther the consumer surplus and producer surplus make the total economic surplus, which economists generally try to maximize. Because different people have different marginal utility of wealth, this is actually a really terrible idea for deep and fundamental reasons—taking a house from Mitt Romney and giving it to a homeless person would most definitely reduce economic surplus, even though it would obviously make the world a better place. Indeed, I think that many of the problems in the world, particularly those related to inequality, can be traced to the fact that markets maximize economic surplus rather than actual utility. But for now I’m going to ignore all that, and pretend that maximizing economic surplus is what we want to do.

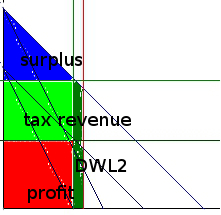

You can read off the economic surplus straight from the supply and demand curves; it’s the area between the lines. (Mathematically, it’s an integral; but that’s equivalent to the area under a curve, and with straight lines they’re just triangles.) I’m going to call the consumer surplus just “surplus”, and producer surplus I’ll call “profit”.

Below the demand curve and above the price is the surplus, and below the price and above the supply curve is the profit:

I’m going to be bold here and actually use equations! Hopefully this won’t turn off too many readers. I will give each equation in both a simple text format and in proper LaTeX. Remember, you can render LaTeX here.

PD = PR – 1/e * Q

P_D = P_R – \frac{1}{e} Q \\

The marginal cost that landlords have to pay, the supply price PS, is a bit weirder, as I’ll talk about more in a moment. For now let’s say that it is a linear function, starting at zero cost for some quantity Q0 and then increases linearly according to a parameter n that similarly represents the elasticity of supply.

PS = 1/n * (Q – Q0)

P_S = \frac{1}{n} \left( Q – Q_0 \right) \\

Now, if you introduce a tax, there will be a difference between the price that renters pay and the price that landlords receive—namely, the tax, which we’ll call T. I’m going to assume that, on paper, the landlord pays the whole tax. As I said above, this literally does not matter. I could assume that on paper the renter pays the whole tax, and the real effect on the distribution of wealth would be identical. All we’d have to do is set PD = P and PS = P – T; the consumer and producer surplus would end up exactly the same. Or we could do something in between, with P’D = P + rT and P’S = P – (1 – r) T.

Then, if the market is competitive, we just set the prices equal, taking the tax into account:

P = PD – T = PR – 1/e * Q – T = PS = 1/n * (Q – Q0)

P= P_D – T = P_R – \frac{1}{e} Q – T= P_S = \frac{1}{n} \left(Q – Q_0 \right) \\

P_R – 1/e * Q – T = 1/n * (Q – Q0)

P_R – \frac{1}{e} Q – T = \frac{1}{n} \left(Q – Q_0 \right) \\

Notice the equivalency here; if we set P’D = P + rT and P’S = P – (1 – r) T, so that the consumer now pays a fraction of the tax r.

P = P’D – rT = P_r – 1/e*Q = P’S + (1 – r) T + 1/n * (Q – Q0) + (1 – r) T

P^\prime_D – r T = P = P_R – \frac{1}{e} Q = P^\prime_S = \frac{1}{n} \left(Q – Q_0 \right) + (1 – r) T\\

The result is exactly the same:

P_R – 1/e * Q – T = 1/n * (Q – Q0)

P_R – \frac{1}{e} Q – T = \frac{1}{n} \left(Q – Q_0 \right) \\

I’ll spare you the algebra, but this comes out to:

Q = (PR – T)/(1/n + 1/e) + (Q0)/(1 + n/e)

Q = \frac{P_R – T}{\frac{1}{n} + \frac{1}{e}} + \frac{Q_0}{1 + \frac{n}{e}}

P = (PR – T)/(1+ n/e) – (Q0)/(e + n)

P = \frac{P_R – T}}{1 + \frac{n}{e}} – \frac{Q_0}{e+n} \\

That’s if the market is competitive.

If the market is a monopoly, instead of setting the prices equal, we set the price the landlord receives equal to the marginal revenue—which takes into account the fact that increasing the amount they sell forces them to reduce the price they charge everyone else. Thus, the marginal revenue drops faster than the price as the quantity sold increases.

After a bunch of algebra (and just a dash of calculus), that comes out to these very similar, but not quite identical, equations:

Q = (PR – T)/(1/n + 2/e) + (Q0)/(1+ 2n/e)

Q = \frac{P_R – T}{\frac{1}{n} + \frac{2}{e}} + \frac{Q_0}{1 + \frac{2n}{e}} \\

P = (PR – T)*((1/n + 1/e)/(1/n + 2/e) – (Q0)/(e + 2n)

P = \left( P_R – T\right)\frac{\frac{1}{n} + \frac{1}{e}}{\frac{1}{n} + \frac{2}{e}} – \frac{Q_0}{e+2n} \\

Yes, it changes some 1s into 2s. That by itself accounts for the full effect of monopoly. That’s why I think it’s worthwhile to use the equations; they are deeply elegant and express in a compact form all of the different cases. They look really intimidating right now, but for most of the cases we’ll consider these general equations simplify quite dramatically.

There are several cases to consider.

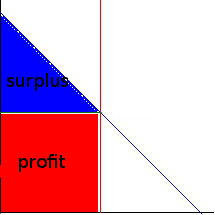

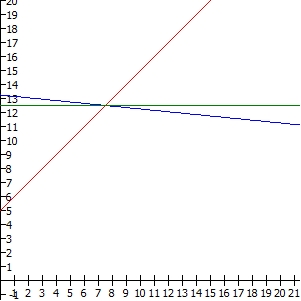

Land has an extremely high cost to create—for practical purposes, we can consider its supply fixed, that is, perfectly inelastic. If the market is competitive, so that landlords have no market power, then they will simply rent out all the land they have at whatever price the market will bear:

This is like setting n = 0 and T = 0 in the above equations, the competitive ones.

Q = Q0

Q = Q_0 \\

P = PR – Q0/e

P = P_R – \frac{Q_0}{e} \\

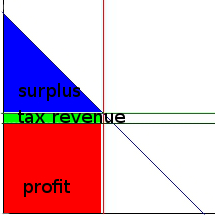

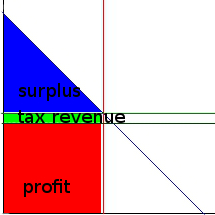

If we now introduce a tax, it will fall completely on the landlords, because they have little choice but to rent out all the land they have, and they can only rent it at a price—including tax—that the market will bear.

Now we still have n = 0 but not T = 0.

Q = Q0

Q = Q_0 \\

P = PR – T – Q0/e

P = P_R – T – \frac{Q_0}{e} \\

The consumer surplus will be:

½ (Q)(PR – P – T) = 1/(2e)* Q02

\frac{1}{2}Q(P_R – P – T) = \frac{1}{2e}Q_0^2 \\

Notice how T isn’t in the result. The consumer surplus is unaffected by the tax.

The producer surplus, on the other hand, will be reduced by the tax:

(Q)(P) = (PR – T – Q0/e) Q0 = PR Q0 – 1/e Q02 – TQ0

(Q)(P) = (P_R – T – \frac{Q_0}{e})Q_0 = P_R Q_0 – \frac{1}{e} Q_0^2 – T Q_0 \\

T appears linearly as TQ0, which is the same as the tax revenue. All the money goes directly from the landlord to the government, as we want if our goal is to redistribute wealth without raising rent.

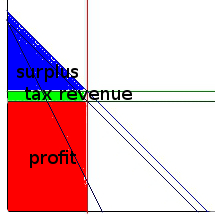

But now suppose that the market is not competitive, and by tacit collusion or regulatory capture the landlords can exert some market power; this is quite likely the case in reality. Actually in reality we’re probably somewhere in between monopoly and competition, either oligopoly or monopolistic competition—which I will talk about a good deal more in a later post, I promise.

It could be that demand is still sufficiently high that even with their market power, landlords have an incentive to rent out all their available land, in which case the result will be the same as in the competitive market.

A tax will then fall completely on the landlords as before:

Indeed, in this case it doesn’t really matter that the market is monopolistic; everything is the same as it would be under a competitive market. Notice how if you set n = 0, the monopolistic equations and the competitive equations come out exactly the same. The good news is, this is quite likely our actual situation! So even in the presence of significant market power the land tax can redistribute wealth in just the way we want.

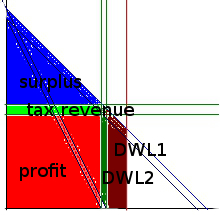

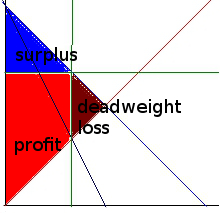

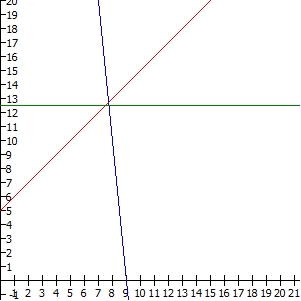

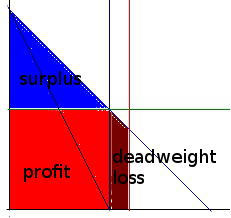

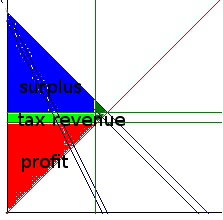

But there are a few other possibilities. One is that demand is not sufficiently high, so that the landlords’ market power causes them to actually hold back some land in order to raise the price:

This will create some of what we call deadweight loss, in which some economic value is wasted. By restricting the land they rent out, the landlords make more profit, but the harm they cause to tenant is created than the profit they gain, so there is value wasted.

Now instead of setting n = 0, we actually set n = infinity. Why? Because the reason that the landlords restrict the land they sell is that their marginal revenue is actually negative beyond that point—they would actually get less money in total if they sold more land. Instead of being bounded by their cost of production (because they have none, the land is there whether they sell it or not), they are bounded by zero. (Once again we’ve hit upon a fundamental concept in economics, particularly macroeconomics, that I don’t have time to talk about today: the zero lower bound.) Thus, they can change quantity all they want (within a certain range) without changing the price, which is equivalent to a supply elasticity of infinity.

Introducing a tax will then exacerbate this deadweight loss (adding DWL2 to the original DWL1), because it provides even more incentive for the landlords to restrict the supply of land:

Q = e/2*(PR – T)

Q = \frac{e}{2} \left(P_R – T\right)\\

P = 1/2*(PR – T)

P = \frac{1}{2} \left(P_R – T\right) \\

The quantity Q0 completely drops out, because it doesn’t matter how much land is available (as long as it’s enough); it only matters how much land it is profitable to rent out.

We can then find the consumer and producer surplus, and see that they are both reduced by the tax. The consumer surplus is as follows:

½ (Q)(PR – 1/2(PR – T)) = e/4*(PR2 – T2)

\frac{1}{2}Q \left( P_R – \frac{1}{2}left( P – T \right) \right) = \frac{e}{4}\left( P_R^2 – T^2 \right) \\

This time, the tax does have an effect on reducing the consumer surplus.

The producer surplus, on the other hand, will be:

(Q)(P) = 1/2*(PR – T)*e/2*(PR – T) = e/4*(PR – T)2

(Q)(P) = \frac{1}{2}\left(P_R – T \right) \frac{e}{2} \left(P_R – T\right) = \frac{e}{4} \left(P_R – T)^2 \\

Notice how it is also reduced by the tax—and no longer in a simple linear way.

The tax revenue is now a function of the demand:

TQ = e/2*T(PR – T)

T Q = \frac{e}{2} T (P_R – T) \\

If you add all these up, you’ll find that the sum is this:

e/2 * (PR^2 – T^2)

\frac{e}{2} \left(P_R^2 – T^2 \right) \\

The sum is actually reduced by an amount equal to e/2*T^2, which is the deadweight loss.

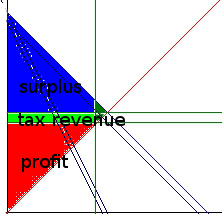

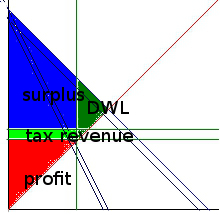

Finally there is an even worse scenario, in which the tax is so large that it actually creates an incentive to restrict land where none previously existed:

Notice, however, that because the supply of land is inelastic the deadweight loss is still relatively small compared to the huge amount of tax revenue.

But actually this isn’t the whole story, because a land tax provides an incentive to get rid of land that you’re not profiting from. If this incentive is strong enough, the monopolistic power of landlords will disappear, as the unused land gets sold to more landholders or to the government. This is a way of avoiding the tax, but it’s one that actually benefits society, so we don’t mind incentivizing it.

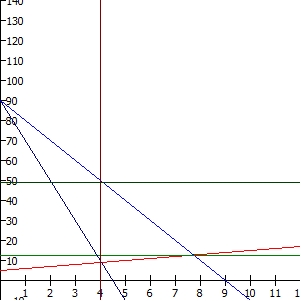

Now, let’s compare this to our current system of property taxes, which include the value of buildings. Buildings are expensive to create, but we build them all the time; the supply of buildings is strongly dependent upon the price at which those buildings will sell. This makes for a supply curve that is somewhat elastic.

If the market were competitive and we had no taxes, it would be optimally efficient:

Property taxes create an incentive to produce fewer buildings, and this creates deadweight loss. Notice that this happens even if the market is perfectly competitive:

Since both n and e are finite and nonzero, we’d need to use the whole equations: Since the algebra is such a mess, I don’t see any reason to subject you to it; but suffice it to say, the T does not drop out. Tenants do see their consumer surplus reduced, and the larger the tax the more this is so.

Now, suppose that the market for buildings is monopolistic, as it most likely is. This would create deadweight loss even in the absence of a tax:

But a tax will add even more deadweight loss:

Once again, we’d need the full equations, and once again it’s a mess; but the result is, as before, that the tax gets passed on to the tenants in the form of more restricted sales and therefore higher rents.

Because of the finite supply elasticity, there’s no way that the tax can avoid raising the rent. As long as landlords have to pay more taxes when they build more or better buildings, they are going to raise the rent in those buildings accordingly—whether the market is competitive or not.

If the market is indeed monopolistic, there may be ways to bring the rent down: suppose we know what the competitive market price of rent should be, and we can establish rent control to that effect. If we are truly correct about the price to set, this rent control can not only reduce rent, it can actually reduce the deadweight loss:

But if we set the rent control too low, or don’t properly account for the varying cost of different buildings, we can instead introduce a new kind of deadweight loss, by making it too expensive to make new buildings.

In fact, what actually seems to happen is more complicated than that—because otherwise the number of buildings is obviously far too small, rent control is usually set to affect some buildings and not others. So what seems to happen is that the rent market fragments into two markets: One, which is too small, but very good for those few who get the chance to use it; and the other, which is unaffected by the rent control but is more monopolistic and therefore raises prices even further. This is why almost all economists are opposed to rent control (PDF); it doesn’t solve the problem of high rent and simply causes a whole new set of problems.

A land tax with a basic income, on the other hand, would help poor people at least as much as rent control presently does—probably a good deal more—without discouraging the production and maintenance of new apartment buildings.

But now we come to a key point: The land tax must be uniform per hectare.

If it is instead based on the value of the land, then this acts like a finite elasticity of supply; it provides an incentive to reduce the value of your own land in order to avoid the tax. As I showed above, this is particularly pernicious if the market is monopolistic, but even if it is competitive the effect is still there.

One exception I can see is if there are different tiers based on broad classes of land that it’s difficult to switch between, such as “land in Manhattan” versus “land in Brooklyn” or “desert land” versus “forest land”. But even this policy would have to be done very carefully, because any opportunity to substitute can create an opportunity to pass on the tax to someone else—for instance if land taxes are lower in Brooklyn developers are going to move to Brooklyn. Maybe we want that, in which case that is a good policy; but we should be aware of these sorts of additional consequences. The simplest way to avoid all these problems is to simply make the land tax uniform. And given the quantities we’re talking about—less than $3000 per hectare per year—it should be affordable for anyone except the very large landholders we’re trying to distribute wealth from in the first place.

The good news is, most economists would probably be on board with this proposal. After all, the neoclassical models themselves say it would be more efficient than our current system of rent control and property taxes—and the idea is at least as old as Adam Smith. Perhaps we can finally change the fact that the rent is too damn high.