Jan 29 JDN 2459973

One of the largest divides in opinion between economists and the general population concerns the question of rent control. While the general public mostly supports rent control (and often votes for it in referenda), economists almost universally oppose it. It’s hard to get a consensus among economists on almost anything, and yet here we have one; but people don’t seem to care.

Why? I think it’s because high rents are a genuine and serious problem, which economists have invested remarkably little effort in trying to solve. Housing prices are one of the chief drivers of long-term inflation, and with most people spending over a third of their income on housing, even relatively small increases in housing prices can cause a lot of suffering.

One thing we do know is that rent control does not work as a long-term solution. Maybe in response to some short-term shock it would make sense. Maybe you do it for awhile as you wait for better long-term solutions to take effect. But simply putting an arbitrary cap on prices will create shortages in the long run—and it is not a coincidence that cities with strict rent control have the worst housing shortages and the greatest rates of homelessness. Rent control doesn’t even do a good job of helping the people who need it most.

Price ceilings in general are just… not a good idea. If people are selling something at a price that you think is too high and you just insist that they aren’t allowed to, they don’t generally sell at a lower price—they just don’t sell at all. There are a few exceptions; in a very monopolistic market, a well-targeted price ceiling might actually work. And short-run housing supply is inelastic enough that rent control isn’t the worst kind of price ceiling. But as a general strategy, price ceilings just aren’t an effective way of making things cheaper.

This is why we so rarely use them as a policy intervention. When the Federal Reserve wants to achieve a certain interest rate on bonds, do they simply demand that people buy the bonds at that price? No. They adjust the supply of bonds in the market until the market price goes to what they want it to be.

Prices aren’t set in a vacuum by the fiat of evil corporations. They are an equilibrium outcome of a market system. There are things you can do to intervene and shift that equilibrium, but if you just outlaw certain prices, it will result in a new equilibrium—it won’t simply be the same amount sold at the new price you wanted.

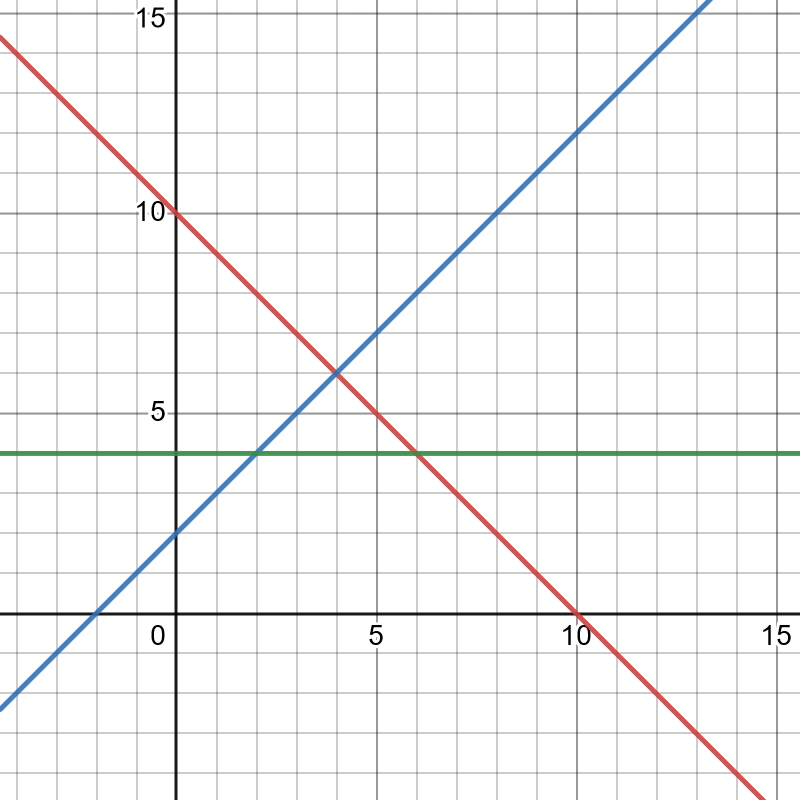

Maybe some graphs would help explain this. In each graph, the red line is the demand and the blue line is the supply.

Here is what the market looks like before intervention: The price is $6. We’ll say that’s too high; people can’t afford it.

[no_intervention.png]

Now suppose we impose a price ceiling at $4 (the green line). You aren’t allowed to charge more than $4. What will happen? Companies will charge $4. But they will also produce and sell a smaller quantity than before.

Far better would be to increase the supply of the good, shifting to a new supply curve (the purple line). Then you would reduce the price and increase the amount of the good available.

[supply_intervention.png]

This is precisely what we do with government bonds when we want to raise interest rates. (A greater supply of bonds makes their prices lower, which makes their yields higher.) And when we want to lower interest rates, we do the opposite.

Of course, with bonds, it’s easy to control the supply; it’s all just numbers in a network. Increasing the supply of housing is a much greater undertaking; you actually need to build new housing. But ultimately, the only way to ensure that housing is available and affordable for everyone is in fact to build more housing.

There are various ways we might accomplish that; one of the simplest would be to simply relax zoning restrictions that make it difficult to build high-density housing in cities. Those are bad laws anyway; they only benefit a small number of people a little bit while harming a large number of people a lot. (The problem is that the people they benefit are the local homeowners who show up to city council meetings.)

But we could do much more. I propose that we really use interest-rate targeting as our model and introduce home price targeting. I want the federal government to exercise eminent domain and order the construction of new high-density housing in any city that has rents above a certain threshold—if you like, the same threshold you were thinking of setting the rent control at.

Is this an extreme solution? Perhaps. But housing affordability is an extreme problem. And I keep hearing from the left wing that economists aren’t willing to consider “radical enough” solutions to housing (by which they always seem to mean the tried-and-failed strategy of rent control). So here’s a radical solution for you. If cities refuse to build enough housing for their people, make them do it. Buy up and bulldoze their “lovely” “historic” suburban neighborhoods that are ludicrous wastes of land (and also environmentally damaging), and replace them with high-rise apartments. (Get rid of the golf courses while you’re at it.)

This would be expensive, of course; we have to pay to build all those new apartments. But hardly so expensive as living in a society where people can’t afford to live where they want.

In fact, estimates suggest that we are losing over one trillion dollars per year in unrealized productivity because people can’t afford to live in the highest-rent cities. Average income per worker in the US has been reduced by nearly $7000 per year because of high housing prices. So that’s the budget you should be comparing against. Keeping things as they are is like taxing our whole population about 9%. (And it’s probably regressive, so more than that for poor people.)

Would this destroy the “charm” of the city? I dunno, maybe a little. But if the only thing your city had going for it was some old houses that are clearly not an efficient use of space, that’s pretty sad. And it is quite possible to build a city at high density and have it still be beautiful and a major draw for tourists; Paris is a lot denser than far-less-picturesque Houston. (Though I’ll admit, Houston is far more affordable than Paris. It’s not just about density.) And is the “charm” of your city really worth making it so unaffordable that people can’t move there without risking becoming homeless?

There are a lot of details to be worked out: How serious must things get before the federal government steps in? (Wherever we draw the line, San Francisco is surely well past it.) It takes a long time to build houses and let prices adjust, so how do we account for that time-lag? Where does the money come from, actually? Debt? Taxes? But these could all be resolved.

Of course, it’s a pipe dream; we’re never going to implement this policy, because homeowners dread the idea of their home values going down (even though it would actually make their property taxes cheaper!). I’d even be willing to consider some kind of program that would let people refinance underwater mortgages to write off the lost equity, if that’s what it takes to actually build enough housing.

Because there is really only one thing that’s ever going to solve the (global!) housing crises:

Build more homes.