Dec6 JDN 2459190

Why do we feel poorer than our parents?

Over the last 20 years, real per-capita GDP has risen from $46,000 to $56,000 (in 2012 dollars):

It’s not just increasing inequality (though it is partly that); real median household income has increased over the same period from $62,500 to $68,700 (in 2019 dollars):

The American Enterprise Institute has utterly the wrong interpretation of what’s going on here, but their graph is actually quite informative if you can read it without their ideological blinders:

Over the past 20 years, some industries have seen dramatic drops in prices, such as televisions, cellphones, toys, and computer software. Other industries have seen roughly constant prices, such as cars, clothing, and furniture. Still other industries have seen modest increases in prices that tracked overall inflation, such as housing and food. And then there are some industries where prices have exploded to staggering heights, such as childcare, college education, and hospital services.

Since wages basically kept up with inflation, this is the relevant comparison: A product or service is more expensive in real terms if its price grew faster than inflation.

It’s not inherently surprising that some prices would rise faster than inflation and some would rise slower; indeed, it would be shocking if that were not the case, since inflation essentially just is an average of all price changes over time. But if you look closely at the kinds of things that got cheaper versus more expensive, you can begin to see why the statistics keep saying we are getting richer but we don’t feel any richer.

The things that increased the most in price are things you basically can’t do without: Education, childcare, and healthcare. Yes, okay, theoretically you could do without these things, but the effects on your life would be catastrophic—indeed, going without healthcare could literally kill you. They are necessities.

The things that decreased the most in price are things that people have done without for most of human history: Cellphones, software, and computer software. They are newfangled high-tech goods that are now ubiquitous, but not at all long ago didn’t even exist. Going without these goods would be inconvenient, but hardly catastrophic. Indeed, they largely only feel as necessary as they are because everyone else already has them. They are luxuries.

This even explains why older generations can be convinced that we are richer than the statistics say: We have all these fancy new high-tech toys that they never had. But what good does that do us when we can’t afford our health insurance?

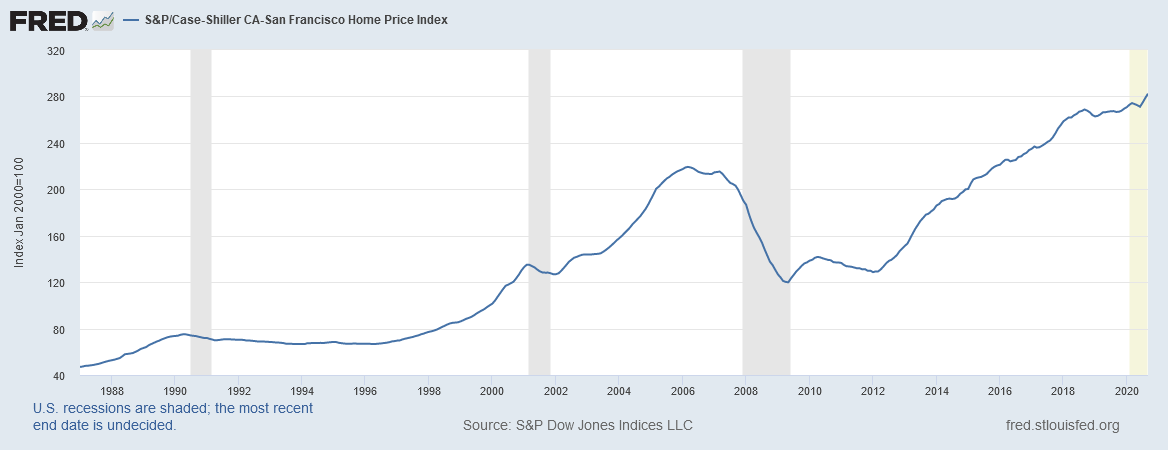

Housing is also an obvious necessity, and while it has not on average increased in price faster than inflation, this average washes out important geographic variation.

San Francisco has seen housing prices nearly triple in the last 20 years:

Over the same period, Detroit’s housing prices plummeted, then returned to normal, and are now only 30% higher than they were 20 years ago (comparable to inflation):

It’s hardly surprising that the cities where the most people are moving to are the most expensive to live in; that’s basic supply and demand. But the magnitude of the difference is so large that most of us are experiencing rising housing prices, even though on average housing prices aren’t really rising.

Put this all together, and we can see that while by the usual measures our “standard of living” is increasing, our financial situation feels ever more precarious, because more and more of our spending is immediately captured by things we can’t do without. I suggest we call this effect necessitization; our consumption has been necessitized.

Healthcare is the most extreme example: In 1960, healthcare spending was only 5% of US GDP. As recently as 2000, it was 13%. Today, it is 18%. Medical technology has greatly improved over that time period, increasing our life expectancy from 70 years in 1960 to 76 years in 2000 to 78 years today, so perhaps this additional spending is worth it? But if we compare 2000 to 2020, we can see that an additional 5% of GDP in the last 20 years has only bought us two years of life. So we have spent an additional 5% of our income to gain 2.6% more life—that doesn’t sound like such a great deal to me. (Also, if you look closely at the data, most of the gains in life expectancy seem to be from things like antibiotics and vaccines that aren’t a large part of our healthcare spending, while most of the increased spending seems to be on specialists, testing, high-tech equipment, and administrative costs that don’t seem to contribute much to life expectancy.)

Moreover, even if we decide that all this healthcare spending is worth it, it doesn’t make us richer in the usual sense. We have better health, but we don’t have greater wealth or financial security.

AEI sees that the industries with the largest price increases have the most government intervention, and blames the government; this is clearly confusing cause with effect. The reason the government intervenes so much in education and healthcare is because these are necessities and they are getting so expensive. Removing those interventions wouldn’t stop prices from rising; they’d just remove the programs like Medicaid and federal student loans that currently allow most people to (barely) afford them.

But they are right about one thing: Prices have risen much faster in some industries than others, and the services that have gotten the most expensive are generally the services that are most important.

Why have these services gotten so expensive? A major reason seems to be that they are difficult to automate. Manufacturing electronics is very easy to automate—indeed, there’s even a positive feedback loop there: the better you get at automating making electronics, the better you get at automating everything, including making electronics. But automating healthcare and education is considerably more difficult. Yes, there are MOOCs, and automated therapy software, and algorithms will soon be outperforming the average radiologist; but there are a lot of functions that doctors, nurses, and teachers provide that are very difficult to replace with machines or software.

Suppose we do figure out how to automate more functions of education and healthcare; would that solve the problem? Maybe—but only if we really do manage to automate the important parts.

Right now, MOOCs are honestly terrible. The sales pitch is that you can get taught by a world-class professor from anywhere in the world, but the truth is that the things that make someone a world-class professor don’t translate over when you are watching recorded video lectures and doing multiple-choice quizzes. Really good teaching requires direct interaction between teacher and student. Of course, a big lecture hall full of hundreds of students often lacks such interaction—but so much the worse for big lecture halls. If indeed that’s the only way colleges know how to teach, then they deserve to be replaced by MOOCs. But there are better ways of teaching that online courses currently cannot provide, and if college administrators were wise, they would be focusing on pressing that advantage. If this doesn’t happen, and education does become heavily automated, it will be cheaper—but it will also be worse.

Similarly, some aspects of healthcare provision can be automated, but there are clearly major benefits to having actual doctors and nurses physically there to interact with patients. If we want to make healthcare more affordable, we will probably have to find other ways (a single-payer health system comes to mind).

For now, it is at least worth recognizing that there are serious limitations in our usual methods of measuring standard of living; due to effects like necessitization, the statistics can say that we are much richer even as we hardly feel richer at all.