JDN 2457359

I think all the pieces are now in place to really talk about tax incidence.

In earlier posts I discussed how taxes have important downsides, then talked about how taxes can distort prices, then explained that taxes are actually what gives money its value. In the most recent post in the series, I used supply and demand curves to show precisely how taxes create deadweight loss.

Now at last I can get to the fundamental question: Who really pays the tax?

The common-sense answer would be that whoever writes the check to the government pays the tax, but this is almost completely wrong. It is right about one aspect, a sort of political economy notion, which is that if there is any trouble collecting the tax, it’s generally that person who is on the hook to pay it. But especially in First World countries, most taxes are collected successfully almost all the time. Tax avoidance—using loopholes to reduce your tax burden—is all over the place, but tax evasion—illegally refusing to pay the tax you owe—is quite rare. And for this political economy argument to hold, you really need significant amounts of tax evasion and enforcement against it.

The real economic answer is that the person who pays the tax is the person who bears the loss in surplus. In essence, the person who bears the tax is the person who is most unhappy about it.

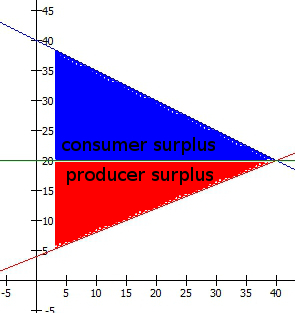

In the previous post in this series, I explained what surplus is, but it bears a brief repetition. Surplus is the value you get from purchases you make, in excess of the price you paid to get them. It’s measured in dollars, because that way we can read it right off the supply and demand curve. We should actually be adjusting for marginal utility of wealth and measuring in QALY, but that’s a lot harder so it rarely gets done.

In the graphs I drew in part 4, I already talked about how the deadweight loss is much greater if supply and demand are elastic than if they are inelastic. But in those graphs I intentionally set it up so that the elasticities of supply and demand were about the same. What if they aren’t?

Consider what happens if supply is very inelastic, but demand is very elastic. In fact, to keep it simple, lets suppose that supply is perfectly inelastic, but demand is perfectly elastic. This means that supply elasticity is 0, but demand elasticity is infinite.

The zero supply elasticity means that the worker would actually be willing to work up to their maximum hours for nothing, but is unwilling to go above that regardless of the wage. They have a specific amount of hours they want to work, regardless of what they are paid.

The infinite demand elasticity means that each hour of work is worth exactly the same amount the employer, with no diminishing returns. They have a specific wage they are willing to pay, regardless of how many hours it buys.

Both of these are quite extreme; it’s unlikely that in real life we would ever have an elasticity that is literally zero or infinity. But we do actually see elasticities that get very low or very high, and qualitatively they act the same way.

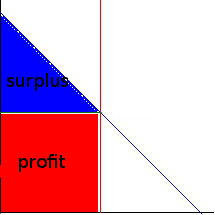

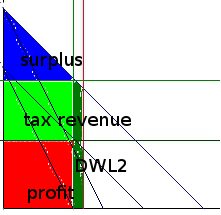

So let’s suppose as before that the wage is $20 and the number of hours worked is 40. The supply and demand graph actually looks a little weird: There is no consumer surplus whatsoever.

Each hour is worth $20 to the employer, and that is what they shall pay. The whole graph is full of producer surplus; the worker would have been willing to work for free, but instead gets $20 per hour for 40 hours, so they gain a whopping $800 in surplus.

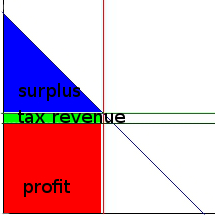

Now let’s implement a tax, say 50% to make it easy. (That’s actually a huge payroll tax, and if anybody ever suggested implementing that I’d be among the people pulling out a Laffer curve to show them why it’s a bad idea.)

Normally a tax would push the demand wage higher, but in this case $20 is exactly what they can afford, so they continue to pay exactly the same as if nothing had happened. This is the extreme example in which your “pre-tax” wage is actually your pre-tax wage, what you’d get if there hadn’t been a tax. This is the only such example—if demand elasticity is anything less than infinity, the wage you see listed as “pre-tax” will in fact be higher than what you’d have gotten in the absence of the tax.

The tax revenue is therefore borne entirely by the worker; they used to take home $20 per hour, but now they only get $10. Their new surplus is only $400, precisely 40% lower. The extra $400 goes directly to the government, which makes this example unusual in another way: There is no deadweight loss. The employer is completely unaffected; their surplus goes from zero to zero. No surplus is destroyed, only moved. Surplus is simply redistributed from the worker to the government, so the worker bears the entirety of the tax. Note that this is true regardless of who actually writes the check; I didn’t even have to include that in the model. Once we know that there was a tax imposed on each hour of work, the market prices decided who would bear the burden of that tax.

By Jove, we’ve actually found an example in which it’s fair to say “the government is taking my hard-earned money!” (I’m fairly certain if you replied to such people with “So you think your supply elasticity is zero but your employer’s demand elasticity is infinite?” you would be met with blank stares or worse.)

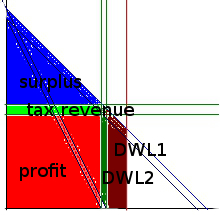

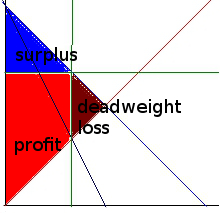

This is however quite an extreme case. Let’s try a more realistic example, where supply elasticity is very small, but not zero, and demand elasticity is very high, but not infinite. I’ve made the demand elasticity -10 and the supply elasticity 0.5 for this example.

Before the tax, the wage was $20 for 40 hours of work. The worker received a producer surplus of $700. The employer received a consumer surplus of only $80. The reason their demand is so elastic is that they are only barely getting more from each hour of work than they have to pay.

Total surplus is $780.

After the tax, the number of hours worked has dropped to 35. The “pre-tax” (demand) wage has only risen to $20.25. The after-tax (supply) wage the worker actually receives has dropped all the way to $10. The employer’s surplus has only fallen to $65.63, a decrease of $14.37 or 18%. Meanwhile the worker’s surplus has fallen all the way to $325, a decrease of $275 or 46%. The employer does feel the tax, but in both absolute and relative terms, the worker feels the tax much more than the employer does.

The tax revenue is $358.75, which means that the total surplus has been reduced to $749.38. There is now $30.62 of deadweight loss. Where both elasticities are finite and nonzero, deadweight loss is basically inevitable.

In this more realistic example, the burden was shared somewhat, but it still mostly fell on the worker, because the worker had a much lower elasticity. Let’s try turning the tables and making demand elasticity low while supply elasticity is high—in fact, once again let’s illustrate by using the extreme case of zero versus infinity.

In order to do this, I need to also set a maximum wage the employer is willing to pay. With nonzero elasticity, that maximum sort of came out automatically when the demand curve hits zero; but when elasticity is zero, the line is parallel so it never crosses. Let’s say in this case that the maximum is $50 per hour.

(Think about why we didn’t need to set a minimum wage for the worker when supply was perfectly inelastic—there already was a minimum, zero.)

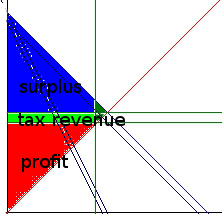

This graph looks deceptively similar to the previous; basically all that has happened is the supply and demand curves have switched places, but that makes all the difference. Now instead of the worker getting all the surplus, it’s the employer who gets all the surplus. At their maximum wage of $50, they are getting $1200 in surplus.

Now let’s impose that same 50% tax again.

The worker will not accept any wage less than $20, so the demand wage must rise all the way to $40. The government will then receive $800 in revenue, while the employer will only get $400 in surplus. Notice again that the deadweight loss is zero. The employer will now bear the entire burden of the tax.

In this case the “pre-tax” wage is basically meaningless; regardless of the value of the tax the worker would receive the same amount, and the “pre-tax” wage is really just an accounting mechanism the government uses to say how large the tax is. They could just as well have said, “Hey employer, give us $800!” and the outcome would be the same. This is called a lump-sum tax, and they don’t work in the real world but are sometimes used for comparison. The thing about a lump-sum tax is that it doesn’t distort prices in any way, so in principle you could use it to redistribute wealth however you want. But in practice, there’s no way to implement a lump-sum tax that would be large enough to raise sufficient revenue but small enough to be affordable by the entire population. Also, a lump-sum tax is extremely regressive, hurting the poor tremendously while the rich feel nothing. (Actually the closest I can think of to a realistic lump-sum tax would be a basic income, which is essentially a negative lump-sum tax.)

I could keep going with more examples, but the basic argument is the same.

In general what you will find is that the person who bears a tax is the person who has the most to lose if less of that good is sold. This will mean their supply or demand is very inelastic and their surplus is very large.

Inversely, the person who doesn’t feel the tax is the person who has the least to lose if the good stops being sold. That will mean their supply or demand is very elastic and their surplus is very small.

Once again, it really does not matter how the tax is collected. It could be taken entirely from the employer, or entirely from the worker, or shared 50-50, or 60-40, or whatever. As long as it actually does get paid, the person who will actually feel the tax depends upon the structure of the market, not the method of tax collection. Raising “employer contributions” to payroll taxes won’t actually make workers take any more home; their “pre-tax” wages will simply be adjusted downward to compensate. Likewise, raising the “employee contribution” won’t actually put more money in the pockets of the corporation, it will just force them to raise wages to avoid losing employees. The actual amount that each party must contribute to the tax isn’t based on how the checks are written; it’s based on the elasticities of the supply and demand curves.

And that’s why I actually can’t get that strongly behind corporate taxes; even though they are formally collected from the corporation, they could simply be hurting customers or employees. We don’t actually know; we really don’t understand the incidence of corporate taxes. I’d much rather use income taxes or even sales taxes, because we understand the incidence of those.