In 2018, David Graeber published a book called Bullshit Jobs, positing that the transition of our economy from industrial manufacturing to ‘post-industrial’ services was in fact largely a transition from meaningful jobs that do actual work to meaningless jobs that employ people without contributing to society.

For instance: in our society, there seems a general rule that, the more obviously one’s work benefits other people, the less one is likely to be paid for it. Again, an objective measure is hard to find, but one easy way to get a sense is to ask: what would happen were this entire class of people to simply disappear? Say what you like about nurses, garbage collectors, or mechanics, it’s obvious that were they to vanish in a puff of smoke, the results would be immediate and catastrophic. A world without teachers or dock-workers would soon be in trouble, and even one without science fiction writers or ska musicians would clearly be a lesser place. It’s not entirely clear how humanity would suffer were all private equity CEOs, lobbyists, PR researchers, actuaries, telemarketers, bailiffs or legal consultants to similarly vanish. (Many suspect it might markedly improve.) Yet apart from a handful of well-touted exceptions (doctors), the rule holds surprisingly well.

I think his claim is a little overstated, but the basic pattern does seem valid: Less and less labor is spent actually making things (or even really doing things) and more and more is spent on selling things and advertising things and suing over things.

While the pattern seems genuine, it’s a little hard to verify empirically, as the usual BLS categories include both useful and useless work in the same categories: “Sales and office occupations” includes far too many things to be useful.

But I think Graeber’s explanations of where the pattern comes from are pretty much totally wrong. He attributes it to “office feudalism” where bosses want to act like lords and “make-work” from government policy trying to create jobs without regard for whether those jobs are useful. I’m not saying these things never happen, but it’s not enough to explain a massive economic transition.

Rather, with a little bit of economic theory, I think it’s not hard to see that these “bullshit jobs” are actually rent-seeking; they don’t produce anything for society, but they are genuinely profitable for the companies that hire them—and thus it’s perfectly rational for a profit-maximizing corporation to behave in this way.

Here’s a simple model to demonstrate the idea.

Suppose there are two corporations, Zero Inc. and One Corp, which both produce cars.

Each factory worker produces r cars. (Presumably they really produce some fraction 1/n of n r cars, but it works out the same.) The labor productivity of factory workers is thus r.

Each factory worker receives a wage wf, which is outside the control of these two corporations (it’s set by a larger labor market).

This means that the marginal cost of producing a car is wf/r. As productivity increases, producing cars becomes cheaper.

The two corporations are in Cournot competition, so they face a total demand for cars that looks like this:

p = a – b (q0 + q1)

where q0 is how many cars Zero produces and q1 is how many cars One produces, and a and b are parameters. This is exogenous; it’s determined by broader market conditions, not by anything the corporations can control.

I’ll spare you the algebra, but this has a well-known equilibrium solution; the two corporations produce the same amount and charge the same price:

q0 = q1 = (a – wf/r)/(3b)

p = (a + 2wf/r)/3

Their profits are also the same, naturally:

F0 = F1 = (p – wf/r)q0 = (a – wf/r)2/(9b)

The number of workers employed making cars is:

L = q/r = 2(a – wf/r)/(3br)

Because the numerator increases with r but so does the denominator, it isn’t obvious whether this is increasing or decreasing in r; more productivity may result in either more or fewer factory workers employed.

By taking the derivative, this can be shown:

dL/dr > 0 iff a > 2w/r

This means that at relatively low levels of productivity, more productivity will increase employment of factory workers; but at high levels of productivity, it will decrease it.

Since profits are proportional to (a – wf/r)2, the higher profits are, the more likely it is that additional productivity will reduce employment of factory workers.

But what if factory workers aren’t the only workers each corporation can employ?

Suppose now that there is another kind of worker they can employ, salesmen.

Zero employs s0 salesmen, while One employs s1. Salesmen are paid a wage ws.

Salesmen don’t actually make anything. They produce no real output. Instead, they allow each firm to take a larger share of the market.

To model this, I’ll use a contest function(I used a similar model in some posts in 2020), where the actual quantity each corporation produces and sells is proportional to the relative number of salesmen employed at each corporation:

q0 = (s0)/(s0 + s1) q

I’ll assume that the total amount of cars produced and sold is the same as before. (Dropping this assumption makes the model much more complicated and hard to solve, without significantly changing the overall conclusions.)

Each corporation’s profits now depend on both how many cars they produce and how many salesmen they hire:

F0 = p q0 – wf/r q0 – ws s0

Again I will spare you the algebra, but it comes out like this:

s0 = s1 = (a – wf/r)2 / (18 b ws)

Unlike employment of factory workers, which may increase or decrease as productivity increases, employment of salesmen always increases.

Thus, as productivity gets higher and higher, we should expect employment of factory workers (“real jobs”) decreasing as employment of salesmen (“bullshit jobs”) increases—even though corporations are being completely rational and maximizing their profits.

Let’s put some numbers on this to make the example more concrete.

Suppose at the start that wf = 1, ws = 2, a = 10, b = 1, and r = 1. (Consider production in cars per day, wages as annual salaries, and money in units of $10,000.)

Then each corporation produces 3 cars per day:

q0 = q1 = (10 – 1/1)/(3*1) = 3

The price of a car is $40,000:

p = (10 + 2*1/1)/3 = 4

The number of factory workers employed is 6:

L = q/r = (3+3)/1

The number of salesmen employed is 4.5 (maybe one is employed half-time):

s = s0 + s1 = (10 – 1/1)2 / (9*1*2) = 81/18 = 4.5

So the majority of workers are factory workers.

But now suppose that productivity greatly increases, to r=10, with everything else the same:

The number of cars produced at each corporation per day increases to 3.3:

q0 = q1 = (10 – 1/10)/(3*1) = 3.3

The price of a car falls to $34,000:

p = (10 + 2*1/10)/3 = 3.4

The number of factory workers employed falls dramatically; there isn’t even one full-time job available, only part-time jobs:

L = (3.3+3.3)/10 = 0.66

But the number of salesmen increases to 5.445 (one additional full-time worker):

s = (10 – 1/10)2 / (9*1*2) = 5.445

Thus, while factory workers used to be 6/(6+4.5) = 57% of the workforce, now they are only 0.66/(0.66+5.445) = 10.8% of the workforce. And this happened because they got more productive!

This is of course a very simple model, but the basic pattern fits:

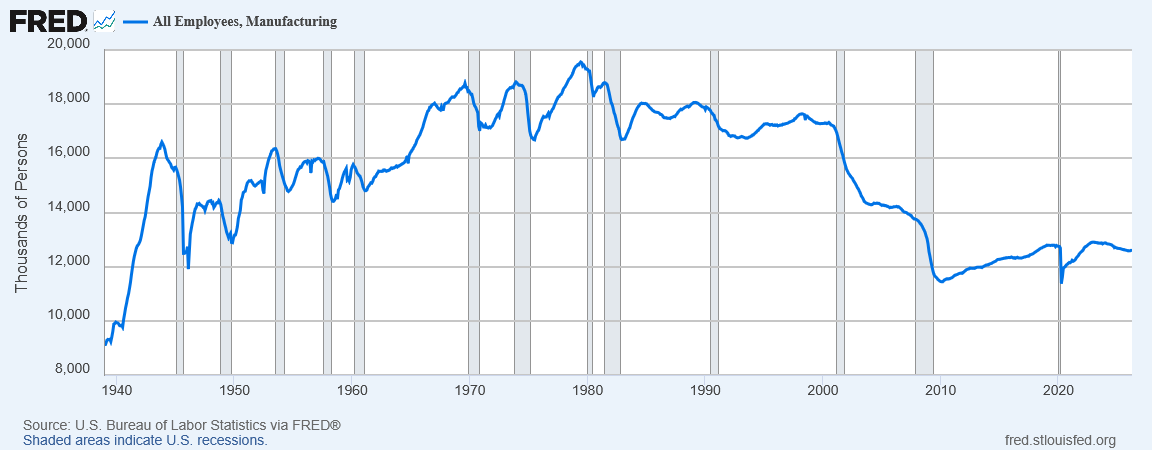

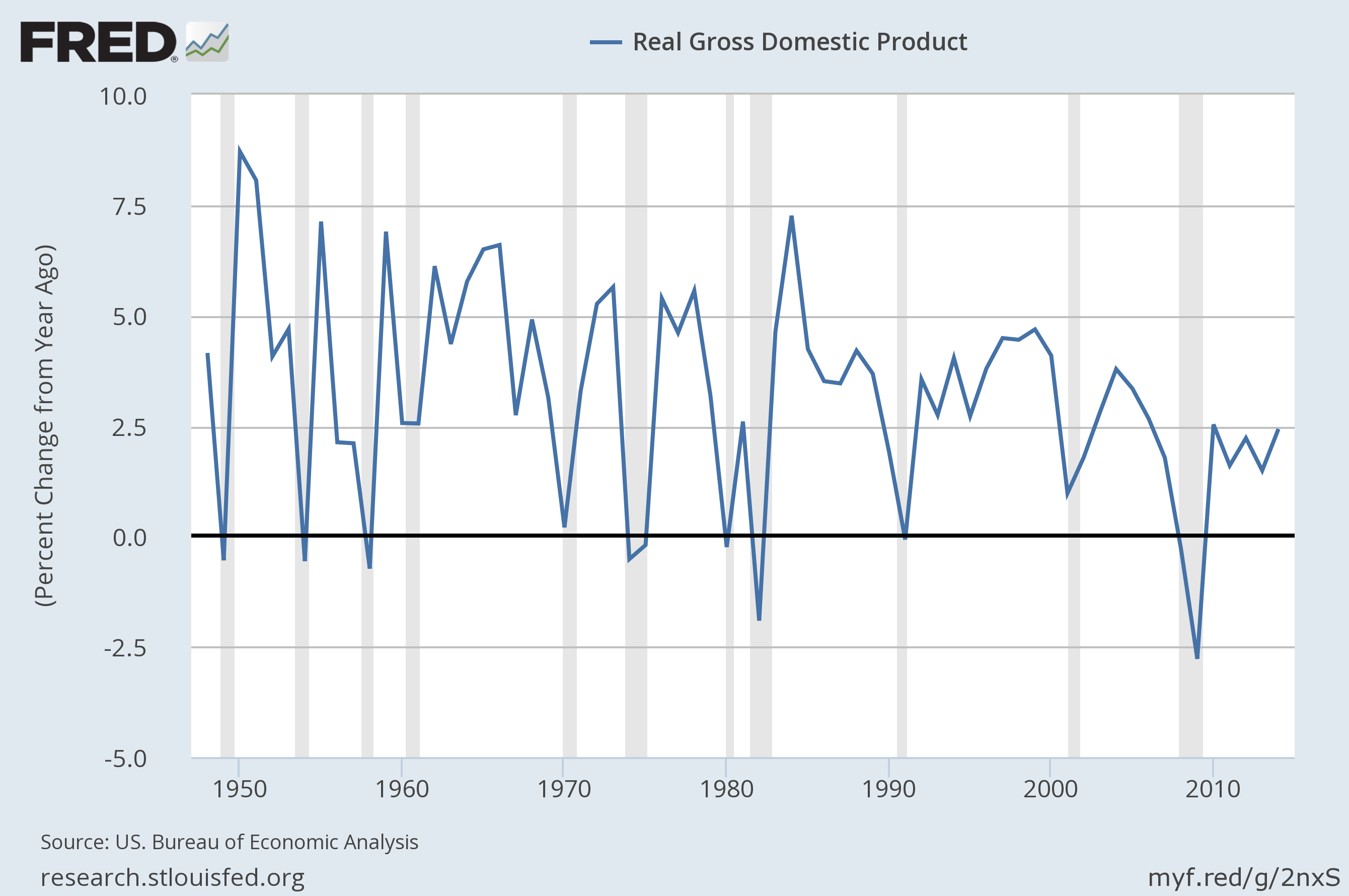

The share of employment that’s in manufacturing has greatly declined since 2000:

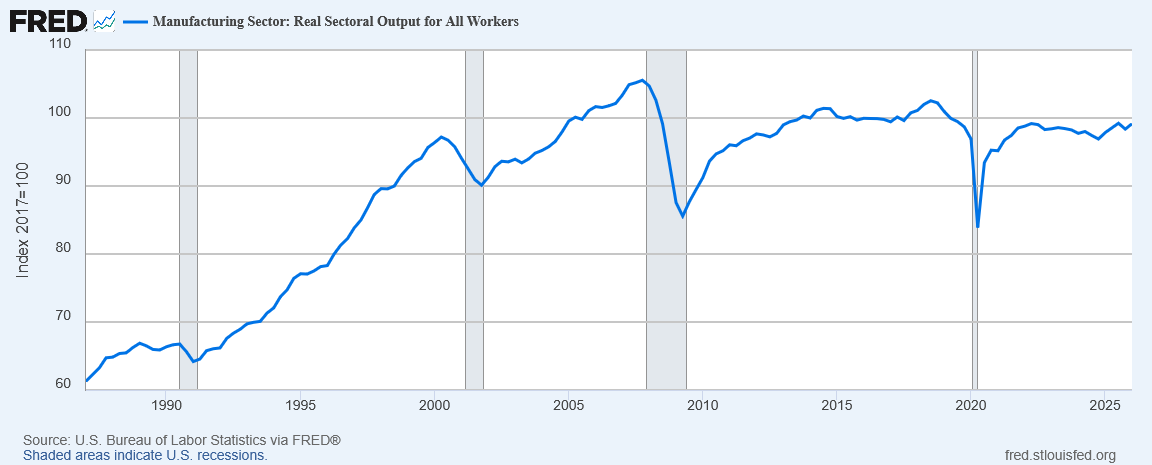

Yet manufacturing output hasn’t really changed:

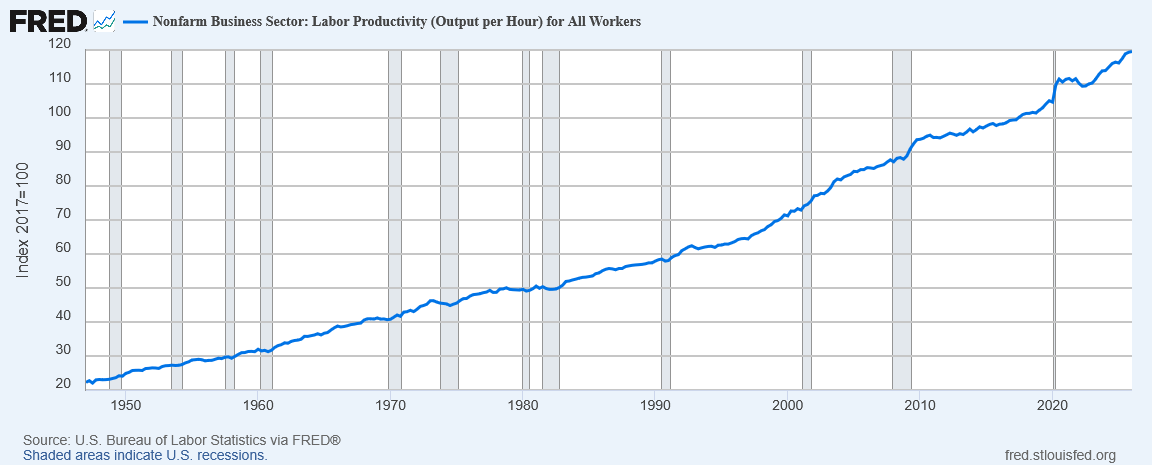

The reason is that labor productivity has continued to rise:

In my model I assumed that factory worker wages haven’t changed, and, well, they really haven’t, despite large increases in productivity. In real terms, a factory worker today makes about 70% more than one in 1950, despite producing nearly six times as much output.

Producing the same amount of stuff now requires fewer people—so fewer people are employed in making stuff. They then end up employed somewhere else; and one of the more profitable ways to employ them these days is in rent-seeking activities like sales and advertising.

What should we do about this?

I already said what I wanted to do years ago: Tax advertising.

So I just finished reading The Meritocracy Trap by David Markovits.

The basic thesis of the book is that America’s rising inequality is not due to a defect in our meritocratic ideals, but is in fact their ultimate fruition. Markovits implores us to reject the very concept of meritocracy, and replace it with… well, something, and he’s never very clear about exactly what.

The most frustrating thing about reading this book is trying to figure out where Markovits draws the line for “elite”. He rapidly jumps between talking about the upper quartile, the upper decile, the top 1%, and even the top 0.1% or top 0.01% while weaving his narrative. The upper quartile of the US contains 75 million people; the top 0.01% contains only 300,000. The former is the size of Germany, the latter the size of Iceland (which has fewer people than Long Beach). Inequality which concentrates wealth in the top quartile of Americans is a much less serious problem than inequality which concentrates wealth in the top 0.01%. It could still be a problem—those lower three quartiles are people too—but it is definitely not nearly as bad.

I think it’s particularly frustrating to me personally, because I am an economist, which means both that such quantitative distinctions are important to me, and also that whether or not I myself am in this “elite” depends upon which line you are drawing. Do I have a post-graduate education? Yes. Was I born into the upper quartile? Not quite, but nearly. Was I raised by married parents in a stable home? Certainly. Am I in the upper decile and working as a high-paid professional? Hopefully I will be soon. Will I enter the top 1%? Maybe, maybe not. Will I join the top 0.1%? Probably not. Will I ever be in the top 0.01% and a captain of industry? Almost certainly not.

So, am I one of the middle class who are suffering alienation and stagnation, or one of the elite who are devouring themselves with cutthroat competition? Based on BLS statistics for economists and job offers I’ve been applying to, my long-term household income is likely to be about 20-50% higher than my parents’; this seems like neither the painful stagnation he attributes to the middle class nor the unsustainable skyrocketing of elite incomes. (Even 50% in 30 years is only 1.4% per year, about our average rate of real GDP growth.) Marxists would no doubt call me petit bourgeoisie; but isn’t that sort of the goal? We want as many people as possible to live comfortable upper-middle class lives in white-collar careers?

Markovits characterizes—dare I say caricatures—the habits of the middle-class versus the elite, and once again I and most people I know cross-cut them: I spend more time with friends than family (elite), but I cook familiar foods, not fancy dinners (middle); I exercise fairly regularly and don’t watch much television (elite) but play a lot of video games and sleep a lot as well (middle). My web searches involve technology and travel (elite), but also chronic illness (middle). I am a donor to Amnesty International (elite) but also play tabletop role-playing games (middle). I have a functional, inexpensive car (middle) but a top-of-the-line computer (elite)—then again that computer is a few years old now (middle). Most of the people I hang out with are well-educated (elite) but struggling financially (middle), civically engaged (elite) but pessimistic (middle). I rent my apartment and have a lot of student debt (middle) but own stocks (elite). (The latter seemed like a risky decision before the pandemic, but as stock prices have risen and student loan interest was put on moratorium, it now seems positively prescient.) So which class am I, again?

I went to public school (middle) but have a graduate degree (elite). I grew up in Ann Arbor (middle) but moved to Irvine (elite). Then again my bachelor’s was at a top-10 institution (elite) but my PhD will be at only a top-50 (middle). The beautiful irony there is that the top-10 institution is the University of Michigan and the top-50 institution is the University of California, Irvine. So I can’t even tell which class each of those events is supposed to represent! Did my experience of Ann Arbor suddenly shift from middle class to elite when I graduated from public school and started attending the University of Michigan—even though about a third of my high school cohort did exactly that? Was coming to UCI an elite act because it’s a PhD in Orange County, or a middle-class act because it’s only a top-50 university?

If the gap between these two classes is such a wide chasm, how am I straddling it? I honestly feel quite confident in characterizing myself as precisely the upwardly-mobile upper-middle class that Markovits claims no longer exists. Perhaps we’re rarer than we used to be; perhaps our status is more precarious; but we plainly aren’t gone.

Markovits keeps talking about “radical differences” “not merely in degree but in kind” between “subordinate” middle-class workers and “superordinate” elite workers, but if the differences are really that stark, why is it so hard to tell which group I’m in? From what I can see, the truth seems less like a sharp divide between middle-class and upper-class, and more like an increasingly steep slope from middle-class to upper-middle class to upper-class to rich to truly super-rich. If I had to put numbers on this, I’d say annual household incomes of about $50,000, $100,000, $200,000, $400,000, $1 million, and $10 million respectively. (And yet perhaps I should add more categories: Even someone who makes $10 million a year has only pocket change next to Elon Musk or Jeff Bezos.) The slope has gotten steeper over time, but it hasn’t (yet?) turned into a sharp cliff the way Markovits describes. America’s Lorenz curve is clearly too steep, but it doesn’t have a discontinuity as far as I can tell.

Some of the inequalities Markovits discusses are genuine, but don’t seem to be particularly related to meritocracy. The fact that students from richer families go to better schools indeed seems unjust, but the problem is clearly not that the rich schools are too good (except maybe at the very top, where truly elite schools seem a bit excessive—five-figure preschool tuition?), but that the poor schools are not good enough. So it absolutely makes sense to increase funding for poor schools and implement various reforms, but this is hardly a radical notion—nor is it in any way anti-meritocratic. Providing more equal opportunities for the poor to raise their own station is what meritocracy is all about.

Other inequalities he objects to seem, if not inevitable, far too costly to remove: Educated people are better parents, who raise their children in ways that make them healthier, happier, and smarter? No one is going to apologize for being a good parent, much less stop doing so because you’re concerned about what it does to inequality. If you have some ideas for how we might make other people into better parents, by all means let’s hear them. But I believe I speak for the entire upper-middle class when I say: when I have kids of my own, I’m going to read to them, I’m not going to spank them, and there’s not a damn thing you can do to change my mind on either front. Quite frankly, this seems like a heavy-handed satire of egalitarianism, right out of Harrison Bergeron: Let’s make society equal by forcing rich people to neglect and abuse their kids as much as poor people do! My apologies to Vonnegut: I thought you were ridiculously exaggerating, but apparently some people actually think like this.

This is closely tied with the deepest flaw in the argument: The meritocratic elite are actually more qualified. It’s easy to argue that someone like Donald Trump shouldn’t rule the world; he’s a deceitful, narcissistic, psychopathic, incompetent buffoon. (The only baffling part is that 40% of American voters apparently disagree.) But it’s a lot harder to see why someone like Bill Gates shouldn’t be in charge of things: He’s actually an extremely intelligent, dedicated, conscientious, hard-working, ethical, and competent individual. Does he deserve $100 billion? No, for reasons I’ve talked about before. But even he knows that! He’s giving most of it away to highly cost-effective charities! Bill Gates alone has saved several million lives by his philanthropy.

Markovits tries to argue that the merits of the meritocratic elite are arbitrary and contextual, like the alleged virtues of the aristocratic class: “The meritocratic virtues, that is, are artifacts of economic inequality in just the fashion in which the pitching virtues are artifacts of baseball.” (p. 264) “The meritocratic achievement commonly celebrated today, no less than the aristocratic virtue acclaimed in the ancien regime, is a sham.” (p. 268)

But it’s pretty hard for me to see how things like literacy, knowledge of history and science, and mathematical skill are purely arbitrary. Even the highly specialized skills of a quantum physicist, software engineer, or geneticist are clearly not arbitrary. Not everyone needs to know how to solve the Schrodinger equation or how to run a polymerase chain reaction, but our civilization greatly benefits from the fact that someone does. Software engineers aren’t super-productive because of high inequality; they are super-productive because they speak the secret language of the thinking machines. I suppose some of the skills involved in finance, consulting, and law are arbitrary and contextual; but he makes it sound like the only purpose graduate school serves is in teaching us table manners.

Precisely by attacking meritocracy, Markovits renders his own position absurd. So you want less competent people in charge? You want people assigned to jobs they’re not good at? You think businesses should go out of their way to hire employees who will do their jobs worse? Had he instead set out to show how American society fails at achieving its meritocratic ideals—indeed, failing to provide equality of opportunity for the poor is probably the clearest example of this—he might have succeeded. But instead he tries to attack the ideals themselves, and fails miserably.

Markovits avoids the error that David Graeber made: Graeber sees that there are many useless jobs but doesn’t seem to have a clue why these jobs exist (and turns to quite foolish Marxian conspiracy theories to explain it). Markovits understands that these jobs are profitable for the firms that employ them, but unproductive for society as a whole. He is right; this is precisely what virtually the entire fields of finance, sales, advertising, and corporate law consist of. Most people in our elite work very hard with great skill and competence, and produce great profits for the corporations that employ them, all while producing very little of genuine societal value. But I don’t see how this is a flaw in meritocracy per se.

Nor does Markovits stop at accusing employment of being rent-seeking; he takes aim at education as well: “when the rich make exceptional investments in schooling, this does reduce the value of ordinary, middle-class training and degrees. […] Meritocratic education inexorably engenders a wasteful and destructive arms educational arms race, which ultimately benefits no one, not even the victors.” (p.153) I don’t doubt that education is in part such a rent-seeking arms race, and it’s worthwhile to try to minimize that. But education is not entirely rent-seeking! At the very least, is there not genuine value in teaching children to read and write and do arithmetic? Perhaps by the time we get to calculus or quantum physics or psychopathology we have reached diminishing returns for most students (though clearly at least some people get genuine value out of such things!), but education is not entirely comprised of signaling or rent-seeking (and nor do “sheepskin effects” prove otherwise).

My PhD may be less valuable to me than it would be to someone in my place 40 years ago, simply because there are more people with PhDs now and thus I face steeper competition. Then again, perhaps not, as the wage premium for college and postgraduate education has been increasing, not decreasing, over that time period. (How much of that wage premium is genuine social benefit and how much is rent-seeking is difficult to say.) In any case it’s definitely still valuable. I have acquired many genuine skills, and will in fact be able to be genuinely more productive as well as compete better in the labor market than I would have without it. Some parts of it have felt like a game where I’m just trying to stay ahead of everyone else, but it hasn’t all been that. A world where nobody had PhDs would be a world with far fewer good scientists and far slower technological advancement.

Abandoning meritocracy entirely would mean that we no longer train people to be more productive or match people to the jobs they are most qualified to do. Do you want a world where surgery is not done by the best surgeons, where airplanes are not flown by the best pilots? This necessarily means less efficient production and an overall lower level of prosperity for society as a whole. The most efficient way may not be the best way, but it’s still worth noting that it’s the most efficient way.

Really, is meritocracy the problem, or is it something else?

Markovits is clearly right that something is going wrong with American society: Our inequality is much too high, and our job market is much too cutthroat. I can’t even relate to his description of what the job market was like in the 1960s (“Old Economy Steve” has it right): “Even applicants for white-collar jobs received startlingly little scrutiny. For most midcentury workers, getting a job did not involve any application at all, in the competitive sense of the term.” (p.203)

In fact, if anything he seems to understate the difference across time, perhaps because it lets him overstate the difference across class (p. 203):

Today, by contrast, the workplace is methodically arranged around gradations of skill. Firms screen job candidates intensively at hiring, and they then sort elite and non-elite workers into separate physical spaces.

Only the very lowest-wage employers, seeking unskilled workers, hire casually. Middle-class employers screen using formal cognitive tests and lengthy interviews. And elite employers screen with urgent intensity, recruiting from only a select pool and spending millions of dollars to probe applicants over several rounds of interviews, lasting entire days.

Today, not even the lowest-wage employers hire casually! Have you ever applied to work at Target? There is a personality test you have to complete, which I presume is designed to test your reliability as an obedient corporate drone. Never in my life have I gotten a job that didn’t involve either a lengthy application process or some form of personal connection—and I hate to admit it, but usually the latter. It is literally now harder to get a job as a cashier at Target than it was to get a job as an engineer at Ford 60 years ago.

But I still can’t shake the feeling that meritocracy is not exactly what’s wrong here. The problem with the sky-high compensation packages at top financial firms isn’t that they are paid to people who are really good at their jobs; it’s that those jobs don’t actually accomplish anything beneficial for society. Where elite talent and even elite compensation is combined with genuine productivity, such as in science and engineering, it seems unproblematic (and I note that Markovits barely even touches on these industries, perhaps because he sees they would undermine his argument). The reason our economic growth seems to have slowed as our inequality has massively surged isn’t that we are doing too good a job of rewarding people for being productive.

Indeed, it seems like the problem may be much simpler: Labor supply exceeds labor demand.

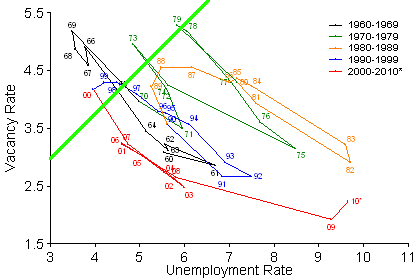

This graph shows the relationship over time between unemployment and job vacancies. As you can see, they are generally inversely related: More vacancies means less unemployment. I have drawn in a green line which indicates the cutoff between having more vacancies than unemployment—upper left—and having more unemployment than vacancies—lower right. We have almost always been in the state of having more unemployment than we have vacancies; notably, the mid-1960s were one of the few periods in which we had significantly more vacancies than unemployment.

For decades we’ve been instituting policies to try to give people “incentives to work”; but there is no shortage of labor in this country. We seem to have plenty of incentives to work—what we need are incentives to hire people and pay them well.

Indeed, perhaps we need incentives not to work—like a basic income or an expanded social welfare system. Thanks to automation, productivity is now astonishingly high, and yet we work ourselves to death instead of enjoying leisure.

And of course there are various other policy changes that have made our inequality worse—chiefly the dramatic drops in income tax rates at the top brackets that occurred under Reagan.

In fact, many of the specific suggestions Markovits makes—which, much to my chagrin, he waits nearly 300 pages to even mention—are quite reasonable, or even banal: He wants to end tax deductions for alumni donations to universities and require universities to enroll more people from lower income brackets; I could support that. He wants to regulate finance more stringently, eliminate most kinds of complex derivatives, harmonize capital gains tax rates to ordinary income rates, and remove the arbitrary cap on payroll taxes; I’ve been arguing for all of those things for years. What about any of these policies is anti-meritocratic? I don’t see it.

More controversially, he wants to try to re-organize production to provide more opportunities for mid-skill labor. In some industries I’m not sure that’s possible: The 10X programmer is a real phenomenon, and even mediocre programmers and engineers can make software and machines that are a hundred times as productive as doing the work by hand would be. But some of his suggestions make sense, such as policies favoring nurse practitioners over specialist doctors and legal secretaries instead of bar-certified lawyers. (And please, please reform the medical residency system! People die from the overwork caused by our medical residency system.)

But I really don’t see how not educating people or assigning people to jobs they aren’t good at would help matters—which means that meritocracy, as I understand the concept, is not to blame after all.

The only thing that hasn’t recovered is labor force participation, which continues to decline. This is how we can have unemployment go back to normal while employment remains depressed; people leave the labor force by retiring, going back to school, or simply giving up looking for work. By the formal definition, someone is only unemployed if they are actively seeking work. No, this is not new, and it is certainly not Obama rigging the numbers. This is how we have measured unemployment for decades.

Actually, it’s kind of the opposite: Since the Clinton administration we’ve also kept track of “broad unemployment”, which includes people who’ve given up looking for work or people who have some work but are trying to find more. But we can’t directly compare it to anything that happened before 1994, because the BLS didn’t keep track of it before then. All we can do is estimate based on what we did measure. Based on such estimation, it is likely that broad unemployment in the Great Depression may have gotten as high as 50%. (I’ve found that one of the best-fitting models is actually one of the simplest; assume that broad unemployment is 1.8 times narrow unemployment. This fits much better than you might think.)

So, yes, we muddle our way through, and the economy eventually heals itself. We could have brought the economy back much sooner if we had better fiscal policy, but at least our monetary policy was good enough that we were spared the worst.

But I think most of us—especially in my generation—recognize that it is still really hard to get a job. Overall GDP is back to normal, and even unemployment looks all right; but why are so many people still out of work?

I have a hypothesis about this: I think a major part of why it is so hard to recover from recessions is that our system of hiring is terrible.

Contrary to popular belief, layoffs do not actually substantially increase during recessions. Quits are substantially reduced, because people are afraid to leave current jobs when they aren’t sure of getting new ones. As a result, rates of job separation actually go down in a recession. Job separation does predict recessions, but not in the way most people think. One of the things that made the Great Recession different from other recessions is that most layoffs were permanent, instead of temporary—but we’re still not sure exactly why.

Both of those show the pattern you’d expect, with openings and hires plummeting in the Great Recession.

But check out this graph, of job separations from 2005 to 2015:

Same pattern!

Unemployment in the Second Depression wasn’t caused by a lot of people losing jobs. It was caused by a lot of people not getting jobs—either after losing previous ones, or after graduating from school. There weren’t enough openings, and even when there were openings there weren’t enough hires.

Part of the problem is obviously just the business cycle itself. Spending drops because of a financial crisis, then businesses stop hiring people because they don’t project enough sales to justify it; then spending drops even further because people don’t have jobs, and we get caught in a vicious cycle.

But we are now recovering from the cyclical downturn; spending and GDP are back to their normal trend. Yet the jobs never came back. Something is wrong with our hiring system.

So what’s wrong with our hiring system? Probably a lot of things, but here’s one that’s been particularly bothering me for a long time.

As any job search advisor will tell you, networking is essential for career success.

But stop and think for a moment about what that means. One of the most important determinants of what job you will get is… what people you know?

It’s not what you are best at doing, as it would be if the economy were optimally efficient.

It’s not even what you have credentials for, as we might expect as a second-best solution.

It’s not even how much money you already have, though that certainly is a major factor as well.

But a good portion of your social network is more or less beyond your control, and above all, says almost nothing about your actual qualifications for any particular job.

There are certain jobs, such as marketing, that actually directly relate to your ability to establish rapport and build weak relationships rapidly. These are a tiny minority. (Actually, most of them are the sort of job that I’m not even sure needs to exist.)

For the vast majority of jobs, your social skills are a tiny, almost irrelevant part of the actual skill set needed to do the job well. This is true of jobs from writing science fiction to teaching calculus, from diagnosing cancer to flying airliners, from cleaning up garbage to designing spacecraft. Social skills are rarely harmful, and even often provide some benefit, but if you need a quantum physicist, you should choose the recluse who can write down the Dirac equation by heart over the well-connected community leader who doesn’t know what an integral is.

At the very least, it strains credibility to suggest that social skills are so important for every job in the world that they should be one of the defining factors in who gets hired. And make no mistake: Networking is as beneficial for landing a job at a local bowling alley as it is for becoming Chair of the Federal Reserve. Indeed, for many entry-level positions networking is literally all that matters, while advanced positions at least exclude candidates who don’t have certain necessary credentials, and then make the decision based upon who knows whom.

Yet, if networking is so inefficient, why do we keep using it?

I can think of a couple reasons.

The first reason is that this is how we’ve always done it. Indeed, networking strongly pre-dates capitalism or even money; in ancient tribal societies there were certainly jobs to assign people to: who will gather berries, who will build the huts, who will lead the hunt. But there were no colleges, no certifications, no resumes—there was only your position in the social structure of the tribe. I think most people simply automatically default to a networking-based system without even thinking about it; it’s just the instinctual System 1 heuristic.

One of the few things I really liked about Debt: The First 5000 Yearswas the discussion of how similar the behavior of modern CEOs is to that of ancient tribal chieftans, for reasons that make absolutely no sense in terms of neoclassical economic efficiency—but perfect sense in light of human evolution. I wish Graeber had spent more time on that, instead of many of these long digressions about international debt policy that he clearly does not understand.

But there is a second reason as well, a better reason, a reason that we can’t simply give up on networking entirely.

The problem is that many important skills are very difficult to measure.

College degrees do a decent job of assessing our raw IQ, our willingness to persevere on difficult tasks, and our knowledge of the basic facts of a discipline (as well as a fantastic job of assessing our ability to pass standardized tests!). But when you think about the skills that really make a good physicist, a good economist, a good anthropologist, a good lawyer, or a good doctor—they really aren’t captured by any of the quantitative metrics that a college degree provides. Your capacity for creative problem-solving, your willingness to treat others with respect and dignity; these things don’t appear in a GPA.

This is especially true in research: The degree tells how good you are at doing the parts of the discipline that have already been done—but what we really want to know is how good you’ll be at doing the parts that haven’t been done yet.

These so-called “soft skills” are difficult to measure—but not impossible. Basically the only reliable measurement mechanisms we have require knowing and working with someone for a long span of time. You can’t read it off a resume, you can’t see it in an interview (interviews are actually a horribly biased hiring mechanism, particularly biased against women). In effect, the only way to really know if someone will be good at a job is to work with them at that job for awhile.

There’s a fundamental information problem here I’ve never quite been able to resolve. It pops up in a few other contexts as well: How do you know whether a novel is worth reading without reading the novel? How do you know whether a film is worth watching without watching the film? When the information about the quality of something can only be determined by paying the cost of purchasing it, there is basically no way of assessing the quality of things before we purchase them.

Networking is an attempt to get around this problem. To decide whether to read a novel, ask someone who has read it. To decide whether to watch a film, ask someone who has watched it. To decide whether to hire someone, ask someone who has worked with them.

The problem is that this is such a weak measure that it’s not much better than no measure at all. I often wonder what would happen if businesses were required to hire people based entirely on resumes, with no interviews, no recommendation letters, and any personal contacts treated as conflicts of interest rather than useful networking opportunities—a world where the only thing we use to decide whether to hire someone is their documented qualifications. Could it herald a golden age of new economic efficiency and job fulfillment? Or would it result in widespread incompetence and catastrophic collapse? I honestly cannot say.

This week’s post will be a bit different: I have a book to review. It’s called Debt: The First 5000 Years, by David Graeber. The book is long (about 400 pages plus endnotes), but such a compelling read that the hours melt away. “The First 5000 Years” is an incredibly ambitious subtitle, but Graeber actually manages to live up to it quite well; he really does tell us a story that is more or less continuous from 3000 BC to the present.

So who is this David Graeber fellow, anyway? None will be surprised that he is a founding member of Occupy Wall Street—he was in fact the man who coined “We are the 99%”. (As I’ve studied inequality more, I’ve learned he made a mistake; it really should be “We are the 99.99%”.) I had expected him to be a historian, or an economist; but in fact he is an anthropologist. He is looking at debt and its surrounding institutions in terms of a cultural ethnography—he takes a step outside our own cultural assumptions and tries to see them as he might if he were encountering them in a foreign society. This is what gives the book its freshest parts; Graeber recognizes, as few others seem willing to, that our institutions are not the inevitable product of impersonal deterministic forces, but decisions made by human beings.

(On a related note, I was pleasantly surprised to see in one of my economics textbooks yesterday a neoclassical economist acknowledging that the best explanation we have for why Botswana is doing so well—low corruption, low poverty by African standards, high growth—really has to come down to good leadership and good policy. For once they couldn’t remove all human agency and mark it down to grand impersonal ‘market forces’. It’s odd how strong the pressure is to do that, though; I even feel it in myself: Saying that civil rights progressed so much because Martin Luther King was a great leader isn’t very scientific, is it? Well, if that’s what the evidence points to… why not? At what point did ‘scientific’ come to mean ‘human beings are helplessly at the mercy of grand impersonal forces’? Honestly, doesn’t the link between science and technology make matters quite the opposite?)

Graeber provides a new perspective on many things we take for granted: in the introduction there is one particularly compelling passage where he starts talking—with a fellow left-wing activist—about the damage that has been done to the Third World by IMF policy, and she immediately interjects: “But surely one has to pay one’s debts.” The rest of the book is essentially an elaboration on why we say that—and why it is absolutely untrue.

Graeber has also made me think quite a bit differently about Medieval society and in particular Medieval Islam; this was certainly the society in which the writings of Socrates were preserved and algebra was invented, so it couldn’t have been all bad. But in fact, assuming that Graeber’s account is accurate, Muslim societies in the 14th century actually had something approaching the idyllic fair and free market to which all neoclassicists aspire. They did so, however, by rejecting one of the core assumptions of neoclassical economics, and you can probably guess which one: the assumption that human beings are infinite identical psychopaths. Instead, merchants in Medieval Muslim society were held to high moral standards, and their livelihood was largely based upon the reputation they could maintain as upstanding good citizens. Theoretically they couldn’t even lend at interest, though in practice they had workarounds (like payment in installments that total slightly higher than the original price) that amounted to low rates of interest. They did not, however, have anything approaching the levels of interest that we have today in credit cards at 29% or (it still makes me shudder every time I think about it) payday loans at 400%. Paying on installments to a Muslim merchant would make you end up paying about a 2% to 4% rate of interest—which sounds to me almost exactly what it should be, maybe even a bit low because we’re not taking inflation into account. In any case, the moral standards of society kept people from getting too poor or too greedy, and as a result there was little need for enforcement by the state. In spite of myself I have to admit that may not have been possible without the theological enforcement provided by Islam.

Graeber also avoids one of the most common failings of anthropologists, the cultural relativism that makes them unwilling to criticize any cultural practice as immoral even when it obviously is (except usually making exceptions for modern Western capitalist imperialism). While at times I can see he was tempted to go that way, he generally avoids it; several times he goes out of his way to point out how women were sold into slavery in hunter-gatherer tribes and how that contributed to the institutions of chattel slavery that developed once Western powers invaded.

Anthropologists have another common failing that I don’t think he avoids as well, which is a primitivist bent in which anthropologists speak of ancient societies as idyllic and modern societies as horrific. That’s part of why I said ‘if Graber’s account is accurate,’ because I’m honestly not sure it is. I’ll need to look more into the history of Medieval Islam to be sure. Graeber spends a great deal of time talking about how our current monetary system is fundamentally based on threats of violence—but I can tell you that I have honestly never been threatened with violence over money in my entire life. Not by the state, not by individuals, not by corporations. I haven’t even been mugged—and that’s the sort of the thing the state exists to prevent. (Not that I’ve never been threatened with violence—but so far it’s always been either something personal, or, more often, bigotry against LGBT people.) If violence is the foundation of our monetary system, then it’s hiding itself extraordinarily well. Granted, the violence probably pops up more if you’re near the very bottom, but I think I speak for most of the American middle class when I say that I’ve been through a lot of financial troubles, but none of them have involved any guns pointed at my head. And you can’t counter this by saying that we theoretically have laws on the books that allow you to be arrested for financial insolvency—because that’s always been true, in fact it’s less true now than any other point in history, and Graeber himself freely admits this. The important question is how many people actually get violence enforced upon them, and at least within the United States that number seems to be quite small.

Graeber describes the true story of the emergence of money historically, as the result of military conquest—a way to pay soldiers and buy supplies when in an occupied territory where nobody trusts you. He demolishes the (always fishy) argument that money emerged as a way of mediating a barter system: If I catch fish and he makes shoes and I want some shoes but he doesn’t want fish right now, why not just make a deal to pay later? This is of course exactly what they did. Indeed Graeber uses the intentionally provocative word communism to describe the way that resources are typically distributed within families and small villages—because it basically is “from each according to his ability, to each according to his need”. (I would probably use the less-charged word “community”, but I have to admit that those come from the same Latin root.) He also describes something I’ve tried to explain many times to neoclassical economists to no avail: There is equally a communism of the rich, a solidarity of deal-making and collusion that undermines the competitive market that is supposed to keep the rich in check. Graeber points out that wine, women and feasting have been common parts of deals between villages throughout history—and yet are still common parts of top-level business deals in modern capitalism. Even as we claim to be atomistic rational agents we still fall back on the community norms that guided our ancestors.

Another one of my favorite lines in the book is on this very subject: “Why, if I took a free-market economic theorist out to an expensive dinner, would that economist feel somewhat diminished—uncomfortably in my debt—until he had been able to return the favor? Why, if he were feeling competitive with me, would he be inclined to take me someplace even more expensive?” That doesn’t make any sense at all under the theory of neoclassical rational agents (an infinite identical psychopath would just enjoy the dinner—free dinner!—and might never speak to you again), but it makes perfectsense under the cultural norms of community in which gifts form bonds and generosity is a measure of moral character. I also got thinking about how introducing money directly into such exchanges can change them dramatically: For instance, suppose I took my professor out to a nice dinner with drinks in order to thank him for writing me recommendation letters. This seems entirely appropriate, right? But now suppose I just paid him $30 for writing the letters. All the sudden it seems downright corrupt. But the dinner check said $30 on it! My bank account debit is the same! He might go out and buy a dinner with it! What’s the difference? I think the difference is that the dinner forms a relationship that ties the two of us together as individuals, while the cash creates a market transaction between two interchangeable economic agents. By giving my professor cash I would effectively be saying that we are infinite identical psychopaths.

While Graeber doesn’t get into it, a similar argument also applies to gift-giving on holidays and birthdays. There seriously is—I kid you not—a neoclassical economist who argues that Christmas is economically inefficient and should be abolished in favor of cash transfers. He wrote a book about it. He literally does not understand the concept of gift-giving as a way of sharing experiences and solidifying relationships. This man must be such a joy to have around! I can imagine it now: “Will you play catch with me, Daddy?” “Daddy has to work, but don’t worry dear, I hired a minor league catcher to play with you. Won’t that be much more efficient?”

This sort of thing is what makes Debt such a compelling read, and Graeber does make some good points and presents a wealth of historical information. So now it’s time to talk about what’s wrong with the book, the things Graeber gets wrong.

First of all, he’s clearly quite ignorant about the state-of-the-art in economics, and I’m not even talking about the sort of cutting-edge cognitive economics experiments I want to be doing. (When I read what Molly Crockett has been working on lately in the neuroscience of moral judgments, I began to wonder if I should apply to University College London after all.)

No, I mean Graeber is ignorant of really basic stuff, like the nature of government debt—almost nothing of what I said in that post is controversial among serious economists; the equations certainly aren’t, though some of the interpretation and application might be. (One particularly likely sticking point called “Ricardian equivalence” is something I hope to get into in a future post. You already know the refrain: Ricardian equivalence only happens if you live in a world of infinite identical psychopaths.) Graeber has internalized the Republican talking points about how this is money our grandchildren will owe to China; it’s nothing of the sort, and most of it we “owe” to ourselves. In a particularly baffling passage Graeber talks about how there are no protections for creditors of the US government, when creditors of the US government have literally never suffered a single late payment in the last 200 years. There are literally no creditors in the world who are more protected from default—and only a few others that reach the same level, such as creditors to the Bank of England.

In an equally-bizarre aside he also says in one endnote that “mainstream economists” favor the use of the gold standard and are suspicious of fiat money; exactly the opposite is the case. Mainstream economists—even the neoclassicists with whom I have my quarrels—are in almost total agreement that a fiat monetary system managed by a central bank is the only way to have a stable money supply. The gold standard is the pet project of a bunch of cranks and quacks like Peter Schiff. Like most quacks, the are quite vocal; but they are by no means supported by academic research or respected by top policymakers. (I suppose the latter could change if enough Tea Party Republicans get into office, but so far even that hasn’t happened and Janet Yellen continues to manage our fiat money supply.) In fact, it’s basically a consensus among economists that the gold standard caused the Great Depression—that in addition to some triggering event (my money is on Minsky-style debt deflation—and so is Krugman’s), the inability of the money supply to adjust was the reason why the world economy remained in such terrible shape for such a long period. The gold standard has not been a mainstream position among economists since roughly the mid-1980s—before I was born.

He makes this really bizarre argument about how because Korea, Japan, Taiwan, and West Germany are major holders of US Treasury bonds and became so under US occupation—which is indisputably true—that means that their development was really just some kind of smokescreen to sell more Treasury bonds. First of all, we’ve never had trouble selling Treasury bonds; people are literally accepting negative interest rates in order to have them right now. More importantly, Korea, Japan, Taiwan, and West Germany—those exact four countries, in that order—are the greatest economic success stories in the history of the human race. West Germany was rebuilt literally from rubble to become once again a world power. The Asian Tigers were even more impressive, raised from the most abject Third World poverty to full First World high-tech economy status in a few generations. If this is what happens when you buy Treasury bonds, we should all buy as many Treasury bonds as we possibly can. And while that seems intuitively ridiculous, I have to admit, China’s meteoric rise also came with an enormous investment in Treasury bonds. Maybe the secret to economic development isn’t physical capital or exports or institutions; nope, it’s buying Treasury bonds. (I don’t actually believe this, but the correlation is there, and it totally undermines Graeber’s argument that buying Treasury bonds makes you some kind of debt peon.)

Speaking of correlations, Graeber is absolutely terrible at econometrics; he doesn’t even seem to grasp the most basic concepts. On page 366 he shows this graph of the US defense budget and the US federal debt side by side in order to argue that the military is the primary reason for our national debt. First of all, he doesn’t even correct for inflation—so most of the exponential rise in the two curves is simply the purchasing power of the dollar declining over time. Second, he doesn’t account for GDP growth, which is most of what’s left after you account for inflation. He has two nonstationary time-series with obvious exponential trends and doesn’t even formally correlate them, let alone actually perform the proper econometrics to show that they are cointegrated. I actually think they probably are cointegrated, and that a large portion of national debt is driven by military spending, but Graeber’s graph doesn’t even begin to make that argument. You could just as well graph the number of murders and the number of cheesecakes sold, each on an annual basis; both of them would rise exponentially with population, thus proving that cheesecakes cause murder (or murders cause cheesecakes?).

And then where Graeber really loses me is when he develops his theory of how modern capitalism and the monetary and debt system that go with it are fundamentally corrupt to the core and must be abolished and replaced with something totally new. First of all, he never tells us what that new thing is supposed to be. You’d think in 400 pages he could at least give us some idea, but no; nothing. He apparently wants us to do “not capitalism”, which is an infinite space of possible systems, some of which might well be better, but none of which can actually be implemented without more specific ideas. Many have declared that Occupy has failed—I am convinced that those who say this appreciate neither how long it takes social movements to make change, nor how effective Occupy has already been at changing our discourse, so that Capital in the Twenty-First Centurycan be a bestseller and the President of the United States can mention income inequality and economic mobility in his speeches—but insofar as Occupy has failed to achieve its goals, it seems to me that this is because it was never clear just what Occupy’s goals were to begin with. Now that I’ve read Graeber’s work, I understand why: He wanted it that way. He didn’t want to go through the hard work (which is also risky: you could be wrong) of actually specifying what this new economic system would look like; instead he’d prefer to find flaws in the current system and then wait for someone else to figure out how to fix them. That has always been the easy part; any human system comes with flaws. The hard part is actually coming up with a better system—and Graeber doesn’t seem willing to even try.

I don’t know exactly how accurate Graeber’s historical account is, but it seems to check out, and even make sense of some things that were otherwise baffling about the sketchy account of the past I had previously learned. Why were African tribes so willing to sell their people into slavery? Well, because they didn’t think of it as their people—they were selling captives from other tribes taken in war, which is something they had done since time immemorial in the form of slaves for slaves rather than slaves for goods. Indeed, it appears that trade itself emerged originally as what Graeber calls a “human economy”, in which human beings are literally traded as a fungible commodity—but always humans for humans. When money was introduced, people continued selling other people, but now it was for goods—and apparently most of the people sold were young women. So much of the Bible makes more sense that way: Why would Job be all right with getting new kids after losing his old ones? Kids are fungible! Why would people sell their daughters for goats? We always sell women! How quickly do we flirt with the unconscionable, when first we say that all is fungible.

One of Graeber’s central points is that debt came long before money—you owed people apples or hours of labor long before you ever paid anybody in gold. Money only emerged when debt became impossible to enforce, usually because trade was occurring between soldiers and the villages they had just conquered, so nobody was going to trust anyone to pay anyone back. Immediate spot trades were the only way to ensure that trades were fair in the absence of trust or community. In other words, the first use of gold as money was really using it as collateral. All of this makes a good deal of sense, and I’m willing to believe that’s where money originally came from.

But then Graeber tries to use this horrific and violent origin of money—in war, rape, and slavery, literally some of the worst things human beings have ever done to one another—as an argument for why money itself is somehow corrupt and capitalism with it. This is nothing short of a genetic fallacy: I could agree completely that money had this terrible origin, and yet still say that money is a good thing and worth preserving. (Indeed, I’m rather strongly inclined to say exactly that.) The fact that it was born of violence does not mean that it is violence; we too were born of violence, literally millions of years of rape and murder. It is astronomically unlikely that any one of us does not have a murderer somewhere in our ancestry. (Supposedly I’m descended from Julius Caesar, hence my last name Julius—not sure I really believe that—but if so, there you go, a murderer and tyrant.) Are we therefore all irredeemably corrupt? No. Where you come from does not decide what you are or where you are going.

In fact, I could even turn the argument around: Perhaps money was born of violence because it is the only alternative to violence; without money we’d still be trading our daughters away because we had no other way of trading. I don’t think I believe that either; but it should show you how fragile an argument from origin really is.

This is why the whole book gives this strange feeling of non sequitur; all this history is very interesting and enlightening, but what does it have to do with our modern problems? Oh. Nothing, that’s what. The connection you saw doesn’t make any sense, so maybe there’s just no connection at all. Well all right then. This was an interesting little experience.

This is a shame, because I do think there are important things to be said about the nature of money culturally, philosophically, morally—but Graeber never gets around to saying them, seeming to think that merely pointing out money’s violent origins is a sufficient indictment. It’s worth talking about the fact that money is something we made, something we can redistribute or unmake if we choose. I had such high expectations after I read that little interchange about the IMF: Yes! Finally, someone gets it! No, you don’t have to repay debts if that means millions of people will suffer! But then he never really goes back to that. The closest he veers toward an actual policy recommendation is at the very end of the book, a short section entitled “Perhaps the world really does owe you a living” in which he very briefly suggests—doesn’t even argue for, just suggests—that perhaps people do deserve a certain basic standard of living even if they aren’t working. He could have filled 50 pages arguing the ins and outs of a basic income with graphs and charts and citations of experimental data—but no, he just spends a few paragraphs proposing the idea and then ends the book. (I guess I’ll have to write that chapter myself; I think it would go well in The End of Economics, which I hope to get back to writing in a few months—while I also hope to finally publish my already-written book The Mathematics of Tears and Joy.)

If you want to learn about the history of money and debt over the last 5000 years, this is a good book to do so—and that is, after all, what the title said it would be. But if you’re looking for advice on how to improve our current economic system for the benefit of all humanity, you’ll need to look elsewhere.

And so in the grand economic tradition of reducing complex systems into a single numeric utility value, I rate Debt: The First 5000 Years a 3 out of 5.