JDN 2457265 EDT 10:47

Last night I was having a political discussion with some friends (as I am wont to do), and it became a little heated, though never uncongenial. A key point of contention was the fact that Bernie Sanders is a socialist, and what exactly that entails.

One of my friends was arguing that this makes him far-left, and thus it is fair when the news media often likes to make a comparison between Sanders on the left and Trump on the right. Donald Trump is actually oddly liberal on some issues, but his attitudes on racial purity, nativism, military unilateralism, and virtually unlimited executive power are literally fascist. Even his “liberal” views are more like the kind of populism that fascists have often used to win support in the past: Don’t you hate being disenfranchised? Give me absolute power and I’ll fix everything for you! Don’t like how our democracy has become corrupt? Don’t worry, I’ll get rid of it! (The democracy, that is.) While he certainly doesn’t align well with the Republican Party platform, I think it’s quite fair to say that Donald Trump is a far-right candidate.

Bernie Sanders, however, is not a far-left candidate. He is a center-left candidate. His views are basically consonant with the Labour Party of the UK and the Social Democratic Party of Germany. He has spoken often about the Scandinavian model (because, well, #Scandinaviaisbetter—Denmark, Sweden, and Norway are some of the happiest places on Earth). When we talk about Bernie Sanders we aren’t talking about following Cuba and the Soviet Union; we’re talking about following Norway and Sweden. As Jon Stewart put it, he isn’t a “crazy-pants cuckoo bird” as some would have you think.

But he’s a socialist, right? Well… sort of—we have to be very clear what that means.

The word “socialism” has been used to mean many things; it has been a cover for genocidal fascism (“National Socialism”) and tyrannical Communism (“Union of Soviet Socialist Republics”). It has become a pejorative thrown at Social Security, Medicare, banking regulations—basically any policy left of Milton Friedman. So apparently it means something between Medicare and the Holocaust.

Social democracy is often classified as a form of socialism—but one can actually make a pretty compelling case that social democracy is not socialism, but in fact a form of capitalism.

If we want a simple, consistent definition of “socialism”, I think I would put it thus: Socialism is a system in which the majority of economic activity is directly controlled by the government. Most, if not all, industries are nationalized; production and distribution are handled by centrally-planned quotas instead of market supply and demand. Under this definition, the USSR, Venezuela, Cuba, and (at least until recently) China are socialist—and under this definition, socialism is a very bad idea. The best-case scenario is inefficiency; the worst-case scenario is mass murder.

Social democracy, the position that Bernie Sanders espouses (and I basically agree wit), is as follows: Social democracy is a system in which markets are taxed and regulated by a democratically-elected government to ensure that they promote general welfare, public goods are provided by the government, and transfer programs are used to reduce poverty and inequality.

Let’s also try to define “capitalism”: Capitalism is a system in which the majority of economic activity is handled by private sector markets.

Under the Scandinavian model, the majority of economic activity is handled by private sector markets, which are in turn regulated and taxed to promote the general welfare—that is, at least on these definitions, Scandinavia is both capitalist and social democratic.

In fact, so is the United States; while our taxes are lower and our regulations weaker, we still have substantial taxes and regulations. We do have transfer programs like WIC, SNAP, and Social Security that attempt to redistribute wealth and reduce poverty.

We could define “socialism” more broadly to mean any government intervention in the economy, in which case Bernie Sander is a socialist and so is… almost everyone else, including most economists.

The majority of the most eminent American economists are in favor of social democracy. I don’t intend this as an argument from authority, but rather to give a sense of the scientific consensus. The consensus in economics is by no means as strong as that in biology or physics (or climatology, ahem), but there is still broad agreement on many issues.

In a survey of 264 members of the American Economics Association [pdf link], 77% opposed government ownership of enterprise (14% mixed feelings, 8% favor) but 71% favored redistribution of wealth in some form (7% mixed feelings, 20% opposed). That’s social democracy is a nutshell. 67% favored public schools (14% mixed feelings, 17% opposed); 75% favored Keynesian monetary policy (12% mixed feelings, 12% opposed); 51% favored Keynesian fiscal policy (19% mixed feelings, 30% opposed). 58% opposed tighter immigration restrictions (16% mixed feelings, 25% opposed). 79% support anti-discrimination laws. 68% favor gun control.

The major departure from left-wing views that the majority of economists make is a near-universal opposition to protectionism, with 86.8% opposed, 7.6% with mixed feelings, and only 5.3% in favor. It seems I am not the only economist to cringe when politicians say they want to “stop sending jobs overseas”, which they do left and right. This view is quite popular; but the evidence says that it is wrong. Protectionism is not the answer; you make your trading partners poorer, they retaliate with their own protections, and you both end up worse off. We need open trade. I’ll save the details on why open trade is so important for a later post.

One issue that economists are very divided on right now is minimum wage; 47.3% favor minimum wage, 38.3% oppose it, and 14.4% have mixed feelings. This division likely reflects the ambiguity of empirical results on the employment effect of minimum wage, which have a wide margin of error but effect sizes that cluster around zero. Economists are also somewhat divided on military aid, with 36.8% in favor, 33% opposed, and 29.9% with mixed feelings. This I attribute more to the fact that military aid, like most military action, can be justified in principle but is typically unjustified in practice. And indeed perhaps “mixed feelings” is the most reasonable view to have on war and its instruments.

Since Bernie Sanders strongly supports raising minimum wage and some of his statements verge on protectionism, I do have to place him to the left of the economic consensus. A lot of economists would probably disagree on the particulars of his tax plans and such. But his core policies are entirely in line with that consensus, and being a social democrat is absolutely part of that. Compare this to the Republicans, who keep trying to out-crazy each other (apparently Scott Walker thinks we should not only build a wall against Mexico, but also against Canada?) and want policies that were abandoned decades ago by mainstream economists (like the gold standard, or a balanced-budget amendment), or simply would never be taken seriously by mainstream economists at all (the aforementioned border wall, eliminating all environmental regulation, or ending all transfer payments and social welfare programs). Even the things they supposedly agree on I’m not sure they do; when economists say they want “deregulation” Republicans seem to think that means “no rules at all” when in fact it’s supposed to mean “simple, transparent rules that can be tightly and fairly enforced”. (I think we need a new term for it, though there is a slogan I like: “Deregulate with a scalpel, not a chainsaw.”) Obama has done a very good job of deregulating in the sense that economists intend, and I think in general most economists view him positively as a leader who made the best of a bad situation.

In any case, the broad consensus of American economists (and I think most economists around the world) is that some form of capitalist social democracy is the best system we have so far. There is dispute about particular policies—how much should the tax rates be, should we tax income, consumption, real estate, capital, etc.; how large should the transfers be; what regulations should be added or removed—but the basic concept of a market economy with a government that taxes, transfers, and regulates is not in serious dispute.

Indeed, social democracy is the economic system of the free world.

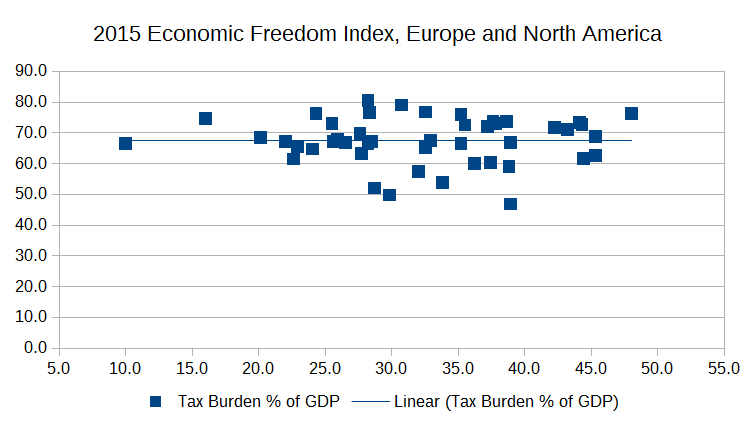

Even using the conservative Heritage Foundation’s data, the correlation between tax burden and economic freedom—that’s economic freedom—is small but positive. (I’m excluding missing data, as well as Timor-Leste because it has a “tax burden” larger than its GDP due to weird accounting of its tourism-based economy, and North Korea because they lie to us and they theoretically have “zero taxes” but that’s clearly not true; the Heritage Foundation reports them as 100% taxes, but that’s also clearly not true either.) See for yourself:

Why is this? Do taxes automatically make you more free? No, they make you less free, because you have to pay for things you didn’t choose to buy (which I admit and the Heritage Foundation includes in their index). But taxes are how you manage a free economy. You need to control monetary policy somehow, which means adding and removing money. The way that social democracies do this is by spending on public goods and transfers to add money, and taxing income, consumption, or assets to remove money. Even if you tie your money to the gold standard, you still need to pay for public goods like military and police; and with a fixed money supply that means spending must be matched by taxes.

There are other ways to do this. You could be like Zimbabwe and print as much money as you feel like. You could be like Venezuela, and have government-owned industries form the majority of your economy. Or, actually, you could not do it; you could fail to manage your country’s economy and leave it wallowing in poverty, like Ghana. All of the countries I just listed have lower tax burdens than the United States.

Within the framework of social democracy, there are higher taxes so that spending and transfers can be higher, which means that more public goods are provided and poverty is lower, which means that real equality of opportunity and thus, real economic freedom, are higher. It’s not that raising taxes automatically makes people more free; rather, the kind of policies that make people more free tend to be the kind of social-democratic policies that involve relatively high taxes.

Worldwide, US is 12th in terms of economic freedom and 62nd in terms of tax burden. We currently stand at 24%. That’s quite low for a First World country, but still relatively high by world standards. The highest tax burden is in Eritrea at 50%; the lowest is in Kuwait at an astonishing 0.7% (I don’t even know how that’s possible). Neither is a really wonderful place to live (though Kuwait is better).

Indeed, if you restrict the sample to North America and Europe, the correlation basically disappears; all the countries are fairly free, all the taxes are fairly high, and within that the two aren’t very much related. (It’s been a long time since I’ve seen a trendline that flat, actually!)

Switzerland, Canada, and Denmark all have higher economic freedom scores than the United States, as well as higher tax burdens; but on the other hand, Greece, Spain, and Austria have higher tax burdens but lower freedom scores. All of them are variations on social democracy.

Is that socialism? I’m really not sure. Why does it matter, really?

{kind=link}