JDN 2457572

Recently I read this article published by the Post Carbon Institute, “How to Shrink the Economy without Crashing It”, which has been going around environmentalist circles. (I posted on Facebook that I’d answer it in more detail, so here goes.)

This is the far left view on climate change, which is wrong, but not nearly as wrong as even the “mainstream” right-wing view that climate change is not a serious problem and we should continue with business as usual. Most of the Republicans who ran for President this year didn’t believe in using government action to fight climate change, and Donald Trump doesn’t even believe it exists.

This core message of the article is clearly correct:

We know this because Global Footprint Network, which methodically tracks the relevant data, informs us that humanity is now using 1.5 Earths’ worth of resources.

We can temporarily use resources faster than Earth regenerates them only by borrowing from the future productivity of the planet, leaving less for our descendants. But we cannot do this for long.

To be clear, “using 1.5 Earths” is not as bad as it sounds; spending is allow to exceed income at times, as long as you have reason to think that future income will exceed future spending, and this is true not just of money but also of natural resources. You can in fact “borrow from the future”, provided you do actually have a plan to pay it back. And indeed there has been some theoretical work by environmental economists suggesting that we are rightly still in the phase of net ecological dissaving, and won’t enter the phase of net ecological saving until the mid-21st century when our technology has made us two or three times as productive. This optimal path is defined by a “weak sustainability” condition where total real wealth never falls over time, so any natural wealth depleted is replaced by at least as much artificial wealth.

Of course some things can’t be paid back; while forests depleted can be replanted, if you drive species to extinction, only very advanced technology could restore them. And we are driving thousands of species to extinction every single year. Even if we should be optimally dissaving, we are almost certainly depleting natural resources too fast, and depleting natural resources that will be difficult if not impossible to later restore. In that sense, the Post Carbon Institute is right: We must change course toward ecological sustainability.

Unfortunately, their specific ideas of how to do so leave much to be desired. Beyond ecological sustainability, they really argue for two propositions: one is radical but worth discussing, but the other is totally absurd.

The absurd claim is that we should somehow force the world to de-urbanize and regress into living in small farming villages. To show this is a bananaman and not a strawman, I quote:

8. Re-localize. One of the difficulties in the transition to renewable energy is that liquid fuels are hard to substitute. Oil drives nearly all transportation currently, and it is highly unlikely that alternative fuels will enable anything like current levels of mobility (electric airliners and cargo ships are non-starters; massive production of biofuels is a mere fantasy). That means communities will be obtaining fewer provisions from far-off places. Of course trade will continue in some form: even hunter-gatherers trade. Re-localization will merely reverse the recent globalizing trade trend until most necessities are once again produced close by, so that we—like our ancestors only a century ago—are once again acquainted with the people who make our shoes and grow our food.

9. Re-ruralize. Urbanization was the dominant demographic trend of the 20th century, but it cannot be sustained. Indeed, without cheap transport and abundant energy, megacities will become increasingly dysfunctional. Meanwhile, we’ll need lots more farmers. Solution: dedicate more societal resources to towns and villages, make land available to young farmers, and work to revitalize rural culture.

First of all: Are electric cargo ships non-starters? The Ford-class aircraft carrier is electric, specifically nuclear. Nuclear-powered cargo ships would raise a number of issues in terms of practicality, safety, and regulation, but they aren’t fundamentally infeasible. Massive efficient production of biofuels is a fantasy as long as the energy to do it is provided by coal power, but not if it’s provided by nuclear. Perhaps this author’s concept of “infeasible” really just means “infeasible if I can’t get over my irrational fear of nuclear power”. Even electric airliners are not necessarily out of the question; NASA has been experimenting with electric aircraft.

The most charitable reading I can give of this (in my terminology of argument “men”, I’m trying to make a banana out of iron), is as promoting slightly deurbanizing and going back to more like say the 1950s United States, with 64% of people in cities instead of 80% today. Even then this makes less than no sense, as higher urbanization is associated with lower per-capita ecological impact, which frankly shouldn’t even be surprising because cities have such huge economies of scale. Instead of everyone needing a car to get around in the suburbs, we can all share a subway system in the city. If that subway system is powered by a grid of nuclear, solar, and wind power, it could produce essentially zero carbon emissions—which is absolutely impossible for rural or suburban transportation. Urbanization is also associated with slower population growth (or even population decline), and indeed the reason population growth is declining is that rising standard of living and greater urbanization have reduced birth rates and will continue to do so as poor countries reach higher levels of development. Far from being a solution to ecological unsustainability, deurbanization would make it worse.

And that’s not even getting into the fact that you would have to force urban white-collar workers to become farmers, because if we wanted to be farmers we already would be (the converse is not as true), and now you’re actually talking about some kind of massive forced labor-shift policy like the Great Leap Forward. Normally I’m annoyed when people accuse environmentalists of being totalitarian communists, but in this case, I think the accusation might be onto something.

Moving on, the radical but not absurd claim is that we must turn away from economic growth and even turn toward economic shrinkage:

One way or another, the economy (and here we are talking mostly about the economies of industrial nations) must shrink until it subsists on what Earth can provide long-term.

[…]

If nothing is done deliberately to reverse growth or pre-adapt to inevitable economic stagnation and contraction, the likely result will be an episodic, protracted, and chaotic process of collapse continuing for many decades or perhaps centuries, with innumerable human and non-human casualties.

I still don’t think this is right, but I understand where it’s coming from, and like I said it’s worth talking about.

The biggest mistake here lies in assuming that GDP is directly correlated to natural resource depletion, so that the only way to reduce natural resource depletion is to reduce GDP. This is not even remotely true; indeed, countries vary almost as much in their GDP-per-carbon-emission ratio as they do in their per-capita GDP. As usual, #ScandinaviaIsBetter; Norway and Sweden produce about $8,000 in GDP per ton of carbon, while the US produces only about $2,000 per ton. Both poor and rich countries can be found among both the inefficient and the efficient. Saudi Arabia is very rich and produces about $900 per ton, while Liberia is exceedingly poor and produces about $800 per ton. I already mentioned how Norway produces $8,000 per ton, and they are as rich as Saudi Arabia. Yet above them is Mali, which produces almost $11,000 per ton, and is as poor as Liberia. Other notable facts: France is head and shoulders above the UK and Germany at almost $6000 per ton instead of $4300 and $3600 respectively—because France runs almost entirely on nuclear power.

So the real conclusion to draw from this is not that we need to shrink GDP, but that we need to make GDP more like how they do it in Norway or at least how they do it in France, rather than how we do in the US, and definitely not how they do it in Saudi Arabia. Total world emissions are currently about 36 billion tons per year, producing about $108 trillion in GDP, averaging about $3,000 of GDP per ton of carbon emissions. If we could raise the entire world to the ecological efficiency of Norway, we could double world GDP and still be producing less CO2 than we currently are. Turning the entire planet into a bunch of Norways would indeed raise CO2 output, by about a factor of 2; but it would raise standard of living by a factor of 5, and indeed bring about a utopian future with neither war nor hunger. Compare this to the prospect of cutting world GDP in half, but producing it as inefficiently as in Saudi Arabia: This would actually increase global CO2 emissions, almost as much as turning every country into Norway.

But ultimately we will in fact need to slow down or even end economic growth. I ran a little model for you, which shows a reasonable trajectory for global economic growth.

This graph shows the growth rate in productivity slowly declining, along with a much more rapidly declining GDP growth:

This graph shows the growth trajectory for total real capital and GDP:

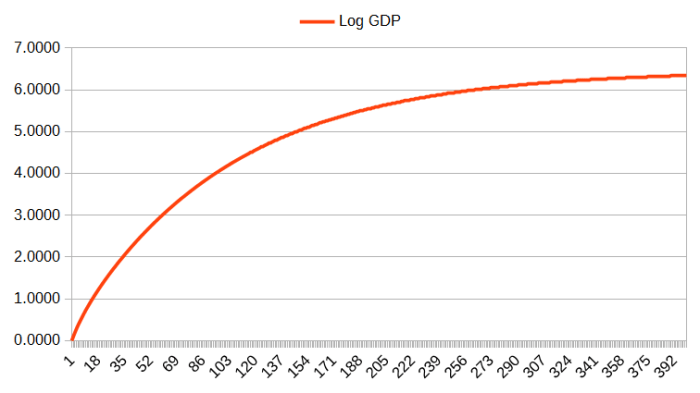

And finally, this is the long-run trend for GDP graphed on a log scale:

The units are arbitrary, though it’s not unreasonable to imagine them as being years and hundreds of dollars in per-capita GDP. If that is indeed what you imagine them to be, my model shows us the Star Trek future: In about 300 years, we rise from a per-capita GDP of $10,000 to one of $165,000—from a world much like today to a world where everyone is a millionaire.

Notice that the growth rate slows down a great deal fairly quickly; by the end of 100 years (i.e., the end of the 21st century), growth has slowed from its peak over 10% to just over 2% per year. By the end of the 300-year period, the growth rate is a crawl of only 0.1%.

Of course this model is very simplistic, but I chose it for a very specific reason: This is not a radical left-wing environmentalist model involving “limits to growth” or “degrowth”. This is the Solow-Swan model, the paradigm example of neoclassical models of economic growth. It is sometimes in fact called simply “the neoclassical growth model”, because it is that influential. I made one very small change from the usual form, which was to assume that the rate of productivity growth would decline exponentially over time. Since productivity growth is exogenous to the model, this is a very simple change to make; it amounts to saying that productivity-enhancing technology is subject to diminishing returns, which fits recent data fairly well but could be totally wrong if something like artificial intelligence or neural enhancement ever takes off.

I chose this because many environmentalists seem to think that economists have this delusional belief that we can maintain a rate of economic growth equal to today indefinitely. David Attenborough famously said “Anyone who believes in indefinite growth in anything physical, on a physically finite planet, is either mad – or an economist.”

Another physicist argued that if we increase energy consumption 2.3% per year for 400 years, we’d literally boil the Earth. Yes, we would, and no economist I know of believes that this is what will happen. Economic growth doesn’t require energy growth, and we do not think growth can or should continue indefinitely—we just think it can and should continue a little while longer. We don’t think that a world standard of living 1000 times as good as Norway is going to happen; we think that a world standard of living equal to Norway is worth fighting for.

Indeed, we are often the ones trying to explain to leaders that they need to adapt to slower growth rates—this is particularly a problem in China, where nationalism and groupthink seems to have convinced many people in China that 7% annual growth is the result of some brilliant unique feature of the great Chinese system, when it is in fact simply the expected high growth rate for an economy that is very poor and still catching up by establishing a capital base. (It’s not so much what they are doing right now, as what they were doing wrong before. Just as you feel a lot better when you stop hitting yourself in the head, countries tend to grow quite fast after they transition out of horrifically terrible economic policy—and it doesn’t get much more terrible than Mao.) Even a lot of the IMF projections are now believed to be too optimistic, because they didn’t account for how China was fudging the numbers and rapidly depleting natural resources.

Some of the specific policies recommended in the article are reasonable, while others go to far.

1. Energy: cap, reduce, and ration it. Energy is what makes the economy go, and expanded energy consumption is what makes it grow. Climate scientists advocate capping and reducing carbon emissions to prevent planetary disaster, and cutting carbon emissions inevitably entails reducing energy from fossil fuels. However, if we aim to shrink the size of the economy, we should restrain not just fossil energy, but all energy consumption. The fairest way to do that would probably be with tradable energy quotas.

I strongly support cap-and-trade on fossil fuels, but I can’t support it on energy in general, unless we get so advanced that we’re seriously concerned about significantly altering the entropy of the universe. Solar power does not have negative externalities, and therefore should not be taxed or capped.

The shift to renewable energy sources is a no-brainer, and I know of no ecologist and few economists who would disagree.

This one is rich, coming from someone who goes on to argue for nonsensical deurbanization:

However, this is a complicated process. It will not be possible merely to unplug coal power plants, plug in solar panels, and continue with business as usual: we have built our immense modern industrial infrastructure of cities, suburbs, highways, airports, and factories to take advantage of the unique qualities and characteristics of fossil fuels.

How will we make our industrial infrastructure run off a solar grid? Urbanization. When everything is in one place, you can use public transportation and plug everything into the grid. We could replace the interstate highway system with a network of maglev lines, provided that almost everyone lived in major cities that were along those lines. We can’t do that if people move out of cities and go back to being farmers.

Here’s another weird one:

Without continued economic growth, the market economy probably can’t function long. This suggests we should run the transformational process in reverse by decommodifying land, labor, and money.

“Decommodifying money”? That’s like skinning leather or dehydrating water. The whole point of money is that it is a maximally fungible commodity. I support the idea of a land tax to provide a basic income, which could go a long way to decommodifying land and labor; but you can’t decommodify money.

The next one starts off sounding ridiculous, but then gets more reasonable:

4. Get rid of debt. Decommodifying money means letting it revert to its function as an inert medium of exchange and store of value, and reducing or eliminating the expectation that money should reproduce more of itself. This ultimately means doing away with interest and the trading or manipulation of currencies. Make investing a community-mediated process of directing capital toward projects that are of unquestioned collective benefit. The first step: cancel existing debt. Then ban derivatives, and tax and tightly regulate the buying and selling of financial instruments of all kinds.

No, we’re not going to get rid of debt. But should we regulate it more? Absolutely. A ban on derivatives is strong, but shouldn’t be out of the question; it’s not clear that even the most useful derivatives (like interest rate swaps and stock options) bring more benefit than they cause harm.

The next proposal, to reform our monetary system so that it is no longer based on debt, is one I broadly agree with, though you need to be clear about how you plan to do that. Positive Money’s plan to make central banks democratically accountable, establish full-reserve banking, and print money without trying to hide it in arcane accounting mechanisms sounds pretty good to me. Going back to the gold standard or something would be a terrible idea. The article links to a couple of “alternative money theorists”, but doesn’t explain further.

Sooner or later, we absolutely will need to restructure our macroeconomic policy so that 4% or even 2% real growth is no longer the expectation in First World countries. We will need to ensure that constant growth isn’t necessary to maintain stability and full employment.

But I believe we can do that, and in any case we do not want to stop global growth just yet—far from it. We are now on the verge of ending world hunger, and if we manage to do it, it will be from economic growth above all else.

{kind=link}